Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the content of the 2020 Canadian Apartment Investment Conference, click the following Insights.

Economic impact of COVID has peaked but expect recovery to be bumpy – Bank of Canada

In its June 3 update, the Bank of Canada held its key lending rate at 0.25 percent.

In a message that was more upbeat than anticipated, the central bank said that the COVID-19 impact on the global economy appears to have peaked.

“Financial conditions have improved, and commodity prices have risen in recent weeks after falling sharply earlier this year,” the bank stated.

Canada has recorded historic job losses but avoided the worst-case scenario, the bank said, updating its projected second-quarter growth to decline between 10% and 20%, down from the 15% to 30% forecasted in April.

The BoC maintains that the economy would still likely resume growth in the third quarter.

It said it was scaling back unprecedented measures to keep financial markets functioning, but continues to buy billions of federal, provincial and corporate bonds at the same rate.

“As the BoC shift its focus from crisis management to ‘supporting the resumption of growth in output and employment,’ we think QE will be key to its stimulus efforts,” stated Josh Nye, Senior Economist at RBC.

Despite the rosy predictions of the central bank, the economic reality of many Canadians is still quite grim.

In Q1, the economy contracted by 8.2% - its most pronounced drop since the global financial crisis in 2009, according to Statistics Canada.

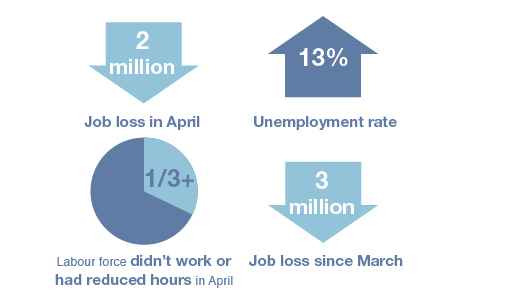

The Canadian economy lost almost two million jobs in April, causing the unemployment rate to rise to 13.0%, as reported by Statistics Canada. In all, more than one-third of the labour force didn’t work or had reduced hours in April. Since March, the economy has lost a total of 3 million jobs.

However, in May, Statistics Canada reports that the economy grew by 4.5% as business started to reopen, and a surprising 290,000 jobs were added to the economy. Unemployment rose to 13.7% - still the highest level in recent record, but significantly lower than anticipated. That said, nearly 80% of the employment gain occurred in Quebec while Ontario actually lost employment. Unemployment dropped to 12.3% in June from a record-high of 13.7% in May, with 953,000 jobs added to the Canadian Economy in June, as reported by Statistics Canada.

According to a May poll conducted by Toronto-based predictive analytics firm Riwi, 23% of Canadians reported losing most or all of their income due to the COVID-19 pandemic. This was significantly more than the 20% in the U.S. who said they’d lost most or all of their income, and the 13% in the U.K., The Logic reports.

A survey of its residents by the City of Vancouver found that 45% of households could not pay their full mortgage in May, and a quarter expects to pay less than half of their property tax bills this year.

At the end of April, mortgage deferrals with Canada’s six largest banks totalled $180 M, or 14% of the $1.24 T in residential mortgages that the nation’s chartered banks held as of March.

Deferrals have also been offered for personal loans, credit cards, and commercial mortgages, with the total (including mortgages) running upwards of $300 billion, The Financial Post reported.

Despite the BoC’s proclamation that the impact of the COVID-19 pandemic has already peaked, CMHC expects that the trend of mortgage deferrals will not be ending any time soon, and expects that 20% of Canadians with mortgages could delay their payments by September of this year.

“A team is at work within CMHC to help manage a growing debt ‘deferral cliff’ that looms in the fall, when some unemployed people will need to start paying their mortgages again,” CMHC CEO Evan Siddall said. “As much as one-fifth of all mortgages coarrears if our economy has not recovered sufficiently.”

Momentum of a historic 2019 in which Canada’s largest multi-family players acquired almost $10 B in product continued into 2020.

According to Altus Group’s National Investment Transaction Statistics for Q4 2019, total multi-family investment for 2019 represented 18% of total investment across all asset classes, and investment volume for the apartment sector was up by 8% to $9.8B. Total transactions were up 4% to 1,165.

The Ottawa market was the strongest performing market in this sector, with total investment volume up by 114% and total transactions up by 20%, followed by Toronto and Montreal.

Continuum REIT’s sale of 44 properties in Ontario to Starlight Investment for $1.7 B was the largest transaction in the country in 2019, closing last December. The portfolio contained a total of 6,271 residential units, representing an aggregate price per unit of $276,116. The projected net income for the portfolio is estimated to be $61.6 M, representing a going-in yield of 3.56%, according to Altus Group.

Starlight acquired approximately $2.8 B in multi-family product in 2019, representing a total of 10,085 units. Most of the units were located in Ontario, with 434 units located in the Greater Vancouver Area.

In Q4 2019, Minto Apartment REIT acquired two properties from QuadReal in for $281.8 M. The buildings, Le 4300 and Haddon Hall, contain a total of 528 units, representing an aggregate price per unit of $532,386.

In Q2 2019, Minto Apartment REIT and Investors Group acquired Le Rockhill from Ivanhoé Cambridge for $268 M, an apartment complex containing six buildings on about 7.6 acres with 1,004 units.

Minto Apartment REIT participated in the acquisition of over $600 M in multi-family product in 2019. Over a half a billion dollars was invested into the Montreal market, and just under $100 M was allocated to the Calgary market.

Homestead picked up a portfolio of five buildings in the Guelph / Cambridge area from Balnar Management at the end of Q4 2019. The portfolio was purchased for $255.4 M and contained a total of 1,064 residential units.

At the end of 2019, Realstar purchased 2333 Taunton Road in Oakville for $164 M. The 286-unit newly constructed complex was built by Branthaven Homes. In Q2 2019, Realstar was active in the Greater Montreal Market, picking up $211 M of product.

The momentum from a historic 2019 carried into Q1 of this year. According to Altus Group, the apartment sectors recorded over $2 billion in Q1 2020 nationally; in GTA, the apartment sector saw the biggest gain with a 164% increase in comparison to the same period last year. Q1 was one of the most active first quarters of the last decade in GTA with transactional volume reaching $614 M and the total number of units sold equalling 2,550. Average cap rates remained steady at approximately 3.5% from the end of 2019, Colliers reports. In Q2 2020, QuadReal purchased three properties in southern Ontario for $300 M from Starlight Investments.The properties located in Hamilton, Cambridge and Kitchener contained a total of 750 units.

EQ8 Phases 3 & 4 in Montreal was purchased by Manulife in January for $105 M. The newly built 300-unit complex contains ground-floor retail and was fully leased at the time of sale.

In Edmonton, $372 M worth of buildings were transacted in January alone, the bulk of which occurred in two transactions where Centurian Apartment REIT acted as the purchaser. This included:

• a three-building, high-rise apartment portfolio with a total of 832 rental suites, plus 39,000 SF of commercial space, which sold for $205 M.

• The Mayfair, a mixed-use multifamily complex on Jasper Avenue with 24,901 SF of ground floor retail, acquired for $100 M.

In Vancouver, Larco Investment acquired 5455 Balsam Street in February. The 87-unit high rise apartment was purchased for $70 M.

At the end of Q3 2019, CMHC reported nearly 72,000 rental units under construction in Canada. This is the highest rate in more than 30 years.

Across the country, new rental buildings are being constructed at a level not seen in decades.

The Senakw Development is an 11.7-acre Squamish Nation-owned site at the foot of Burrard Bridge near Vanier Park in Vancouver. The project will feature about 6,000 units of mostly rentals in 11 towers. Squamish Nation has partnered with developer Westbank, and construction for phase one could start in 2021. The Senakw development will be on federal reserve land, which means that the nation does not need permission from the city to go ahead. It also is not restricted by density or height limits. The tallest tower planned is 56 storeys.

The Globe & Mail reports that it would be one of the largest private First Nations investment projects in the country, expected by the Squamish to be in the billions of dollars, and turn the First Nation into a significant developer in Vancouver’s lucrative housing market.

In Edmonton, three new rental projects consisting of a total of 369 units were launched during the second quarter of last year, and seven new rental projects totalling 782 units were launched in Q3 2019, JLL reports.

The Augustana located at 9901–107 Street NW in downtown Edmonton is scheduled for completion in 2020. The Pangman Development Corporation’s mixed-use development consists of a 30-storey apartment building, with 240 apartment units for rent ranging from studios to 3 bedrooms. The building also incorporates 6,400 SF of commercial space on the ground floor.

Also under construction is Southpark on Whyte, an apartment development by ONE Properties and Wheaton Properties located at 82 Avenue NW in Edmonton. The project features retail space on the ground floor, and a total of 660 residential units. Phase 1 will be completed Fall 2020 with 98 residential units.

One Properties is currently constructing the Curtis Block in the Beltline neighbourhood, just outside of Calgary’s downtown core. The first phase of development for the 1,030-unit complex consists of 650 rental suites in two towers of 34 and 37 storeys, with 16,500 SF of retail space on the ground floor. There are also three levels of underground parking.

Cidex Developments has submitted a development permit application for a three-building complex on a 3.3-acre site located just west of Stampede Park in Calgary. The residential towers will range in height from 44 to 55 storeys and will be built on top of a nine-level podium that will contain restaurant and retail spaces on the ground level, as well as 1,180 vehicle parking stalls.

The first building would be 55 storeys and is expected to create 465 one bedroom and two bedroom rental units, including 22 affordable units.

The development will be located near the Victoria Park/Stampede LRT Station and once complete, will contain 1,252 units. If approved, the development will be one of the largest in Calgary in terms of the number of homes within a multi-residential project.

Devimco Immobilier has unveiled a 1.2 MSF mixed-use project that will include a complete overhaul of the Longueuil – Université-de- Sherbrooke Metro station. The $500 M development will contain 1,200 rental and condo units, including two rental towers and two condo towers, each of which will have 22 storeys. The project will be built over a six-year period starting in the latter half of 2021 and will begin with the demolition of the current Metro station.

GWL Realty Advisors has several new purpose-built rental developments in the pipeline aimed at accommodating family renters by offering a wide range of amenities, unit types and sizes.

Announced in February, Enfield Place will be a 35-storey, 365-apartment building in Mississauga’s Square One District. The new 366-unit building will have 59% of units designed for singles and couples as one bedroom, and 41% two bedroom and larger.

At the end of 2019, a total of 57,197 new purpose-built rentals were proposed for development but had not yet started construction, rising from 44,086 units at the end of 2018 and reaching the highest level tracked by Urbanation over the last five years.

In Ottawa, Trinity Development Group has more than 2,300 rental units under construction or planned, mostly near stations on the new Confederation light-rail line and the Trillium Line. One ofthe largest projects is 900 Albert St., a three-building 1,300-unit development located at Bayview Station. The complex will be built atop a large multi-level podium that will contain an estimated 85,000 SF of retail space and 500,000 SF of office space.

At the end of 2019, Trinity, along with its partner Timbercreek, broke ground on Rideau and Chapel, a two-tower development containing a total of 633 rental units and 9,500 SF of ground floor commercial space and 477 parking spaces. The first tower contains 315 units and is scheduled to begin occupancy in 2022.

In Quebec City, Kevlar, Constrobourg and Groupe Patrimoine have announced the development of Quartier Mosaïque, a $750 M development on a 900,000 SF parcel of land in Lebourgneuf that was purchased from the city.

The project will have 2,200 housing units in 11 towers divided between condos, rental apartments and seniors housing. Towers will range between eight and 14 storeys and contain 555 seniors’ units, 485 condo units and 1,150 rental apartments.

Demand for rental housing expected to drop slightly as immigration stalls and economic pressures mount.

The national vacancy rate for rental apartment units declined in 2019 for a third consecutive year to 2.2%, its lowest level since 2002. Vancouver, Toronto, Montreal and Ottawa all had vacancy rates of less than 2% in 2019, according to data from CMHC.

Prior to the pandemic, apartment buildings were near full occupancy in markets from coast to coast, and rent growth was accelerating quickly. Over the last year, average rents for purpose-built rental units have grown by 3.9% annually at the national level.

The average annual rent for a rental apartment in Canada rose by 5.7% to $1,530 in 2019 compared to the year before.

Asking rents for all property types in Toronto, Vancouver and Montreal increased annually by 9%, 11% and 25% respectively in 2019.

In December 2019, the average one bedroom rent for all property types in Toronto was $2,299, while two bedroom was $2,914, according to the rental listing website Rentals.ca.

CMHC forecasted that the vacancy rate in Toronto would fall to 1.2% in 2020, a slight decrease from 2019’s 1.5%. However, these estimates predated the pandemic. Fast forward a couple of months and the national apartment rental situation looks vastly different.

In April, the average asking price for apartments nationwide fell to$1,491. Condos rental rates fell 8.8% from $2,488 at the end of 2019 to $2,268 in 2020.

Industry watchers expect vacancy and rental rates to fall further.

Closed borders have affected tourism, immigration, and temporary residents, as well as weakening job prospects, which have all contributed to a negative demand for rental housing.

With vacation travel at a standstill, owners of Airbnb rental units are putting their properties on the apartment rental market, which is resulting in a rise in new rental listings, especially in certain neighbourhoods.

“Some investors are likely scrambling to find long-term tenants for their short-term rentals,” said RBC Economist Robert Hogue. “This could add some much-needed supply to tight rental markets,” he added.

“Because of COVID-19, Canada will have less immigration (and) fewer international students and, with the border closed, not nearly as many seasonal and part-time workers. All typically are renters,” wrote Ben Meyers, President of Bullpen Research, an affiliate of Rental.ca.

Stephen Brown, a Senior Economist with Capital Economics, wrote that net immigration to the country has fallen from 30,000 monthly arrivals to close to zero. Vancouver and Toronto are the destinations for the highest number of immigrants to the country, most of whom rent upon their arrival.

A CMHC Analyst, Andrew Scott, has found that non-permanent residents have accounted for 46% of the growth in Metro Vancouver of people between the ages of 18 and 44, the group most likely to rent. “There were at least 100,000 international students living and working in Metro Vancouver – many of whom returned home,” Douglas Todd wrote in The Province.

CMHC, Moody’s and other analysts are predicting declines in double-digit house prices over the next year or two. People who had intended to sell their homes may be trying to wait out the downturn by renting them instead. This has also increased the supply of rental accommodations.

“Rents in the major cities seem to be falling fast,” Brown wrote in a recent client note. He projected that “rents seem likely to declineby at least 5% to 10% in Toronto and Vancouver.”

Shift in consumer behaviour due to social distancing policies has motivated companies to adopt new technologies at a rapid pace.

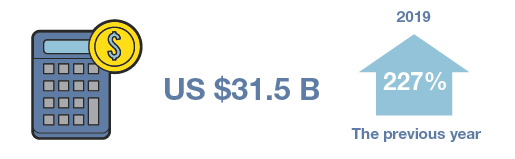

The PropTech industry had experienced a flood of venture capital investment in 2019. Global VC investment in real estate tech companies reached a record high of US $31.5 B, a 227% increase from the previous year, according to a CREtech year-end report.

Current social distancing policies are forcing real estate companies to adopt new technologies and are accelerating the adoption of PropTech solutions, especially services that facilitate streamlined real estate transactions.

There has been a rise in virtual touring, self-touring and more automated apartment search processes, Forbes reports.

VirtualAPT, a four-year-old startup that uses robots to create virtual walkthrough tours of residential and commercial properties, has seen demand rise by more than 500% over the last month, founder and CEO Bryan Colin said.

Truss, an online leasing platform that offers virtual tours of buildings, received more than 500 requests for virtual tours in the first two weeks of April, a tenfold increase from the prior month, Co-Founder Bobby Goodman told Bisnow.

Steve Boyack, CEO of global real estate investment and management company CA Management Services states that behaviours have been slow to change: “These are not new technologies but have been slow to adapt due to consumer behaviour.”

An article from management consulting firm McKinsey & Company entitled The COVID-19 recovery will be digital: A plan for the first 90 days states: “We have vaulted five years forward in consumer and business digital adoption in a matter of around eight weeks.”

“There is no entirely digitized end-to-end solution that allows a prospect to go from lead to tour to lease,” business strategist Khushbu Sikaria writes in Hive. “There are many point solutions that exist to solve a piece of the leasing process, but operators are often forced to patch together five or more technologies to create a fully automated funnel, which is anything but efficient,” she writes.

The company that is closest to developing an end-to-end solution is MeetElise. Last fall, the company raised US $1.9 M series seed financing led by Golden Seeds and backed by AvalonBay Communities and Equity Residential.

MeetElise’s AI leasing assistant named Elise answers questions and schedules apartment tours 24/7 via email and text messaging. Prospective renters receive real-time assistance and allow leasing agents to focus on in-person interactions rather than answering emails and returning phone calls. Elise converts 65% more leads to residents than a leasing team alone the company reports.

The pandemic has made it necessary for building management to be performed remotely, in order to minimize staff exposure to the virus. Enertiv provides remote building management capabilities. The company’s software-first solutions help building owners access building systems remotely, take over work vendors formerly performed and document all their processes.

Pre-pandemic, parcel storage has challenged many property managers. In the last few months, online shopping has accelerated, and package deliveries have increased by 40% in the US. Canada Post has reported a 30% increase.

RENX reports that parcel locker companies such as Snaile and LocKourier have seen increased demand for their products since COVID-19.

“We are seeing an increase in condominium inquiries looking for a low-contact solution for parcels, instead of having to rely on face-to-face interactions or their concierge,” said Snaile CEO Patrick Armstrong.

Snaile operates lockers in almost 200 locations in 23 Canadian cities for building owners that include Oxford Properties, Starlight Investments, Hollyburn Properties, Akelius, Minto, Cogir Real Estate, KingSett Capital, Westbank, Townline, Canderel, Shiplake and Strategic Group. The company also provides both refrigerated and freezer smart lockers.

Closed borders, travel restrictions and shelter in place orders have dried up the short-term rental market almost overnight.

At the beginning of April, Ontario joined Quebec and several jurisdictions in the US by banning Airbnb and short-term vacation rentals. Under Ontario’s Emergency Management and Civil Protection Act, Airbnb rentals are only allowed for those in need of housing.

Data from research site AirDNA revealed in early April that bookings in some cities were down by 96% as travel came to a halt, and governments around the world issued shelter in place orders.

Airbnb’s original intent was to give people the opportunity to make some extra money by renting out a spare room or an unused vacation home. Many hosts, however, have built short term rental empires.

AirDNA data shows that of the 1.1 M Airbnb listings in the US, about 600,000 are from hosts that have at least two other listings. McGill University Assistant Professor of Urban Planning, David Wachsmuth, found that almost half of all Airbnb revenue last year was generated by commercial operators who manage multiple listings.

This business model has led to a rental arbitrage boom, especially in cities that are popular tourist destinations, Wired UK reports. People have rented properties on a long-term basis and then have re-rented them on short-term rental platforms. With tourism at a standstill, no rent is being collected, leaving these hosts in a precarious financial situation.

Airbnb created a US $250 M Host Relief Fund and an additional US $10 M “Superhost” relief fund at the end of March to ease the financial pressure on hosts following the mass cancellation of bookings due to the pandemic.

Airbnb stated it would pay out 25% of what hosts would normally receive for a cancelled booking, based on their individual cancellation policies for check-ins that were scheduled between March 14 and May 31, 2020.

In a letter to Chrystia Freeland, Airbnb has asked the Canadian government to provide support for hosts who have lost income from cancelled bookings in the form of tax breaks. Nearly a third of Canada’s Airbnb hosts need the income to avoid eviction or foreclosure, the letter said. It also requested that the government fund a tourist promotion program to help the sector recover. The request was not met with very much enthusiasm.

To mitigate the loss of income, many short-term rental units have returned to the long-term rental market.

“In cities across the world, long-term rental websites have been flooded with identikit one and two bedroom apartments, replete with bedrooms adorned with neatly-folded towels and prominently-displayed Nespresso coffee machines” Wired UK reports.

McGill’s David Wachsmuth calculates that Airbnb has likely taken about 31,000 units from Canada’s long-term rental market. Advocacy group Fairbnb Canada, estimates that the COVID-19 crisis could put up to 7,500 homes back on the long-term market.

John Pasalis, President of Realosophy Realty, told CBC that there has been a 25% increase in the number of condos being listed for rent in Toronto. He says a surge in listings has pushed the condo rental inventory from one-and-a-half months of inventory (MOI) at the end of March to nearly 4 MOI at the end of April.

Even before the onslaught of COVID-19, Airbnb was facing some challenges with some cities clamping down on short term rental regulations.

Last summer, Montreal implemented new regulations for short term property rentals to ensure that every time properties get rented through online platforms, the required 3.5% accommodation tax is being paid to the provincial government.

In November 2019, a new Toronto by-law came into effect, forbidding homeowners from renting out any properties on Airbnb except for their primary residence or rooms in a primary residence.

As a result of these more stringent rules, furnished long-term rentals experienced a 29% year-over-year increase in listings during Q1 2020 to 1,382 units, Urbanation reported.

Vancouver Councillor Pete Fry is proposing city staff tighten the regulations on short term rentals. In his motion, he cites issues such as units rented longer than the permitted 30 days, lack of strata permission to run an Airbnb, as well as no appropriate oversight of safety standards in the context of COVID-19.

Once travel resumes, governments will likely continue to place tighter regulations around short term rentals. New cleaning standards will make it more costly for some operators, while some guests will prefer to stay in corporate hotel chains where cleaning protocols are more closely monitored.

In April, Airbnb raised US $2 B in debt financing and in May, the company cut 25% of its staff. The company is forecasting that revenue will be less than half of last year’s US $4.8 B.

Across the country, COVID-19 is highlighting the urgent need for affordable housing.

At the end of 2019, there were about 1.7 M Canadian households who are living in ‘core housing need,’ meaning they live in a home that is too small or too costly. This number is likely to skyrocket as the pandemic takes its toll on the economy.

Toronto city Councillor Joe Cressy writes, “COVID-19 has exposed the negative health effects of poverty for our entire society. We need to invest in affordable and supportive housing while also exploring new ideas such as modular housing and changes to zoning to increase density. Public investment in housing works as an economic stimulus, not only by creating jobs in construction and development but also by providing people with a place to live and better health outcomes.”

Toronto Mayor John Tory announced that the city is moving forward with building between 1,455 and 1,710 new residential units as part of Phase 2 of the city’s Housing Now initiative.

“We know that COVID-19 has had great impacts on Toronto and its economy, but we also know that the city will rebound and recover from the pandemic. And when that happens... we will be ready to push ahead on still more affordable housing.”

The recommended locations for the new residential units are 158 Borough Drive, 2444 Eglinton Ave. E., 1627 and 1675 Danforth Avenue, 1631 Queen Street East, 405 Sherbourne Street, and 150 Queens Wharf Road.

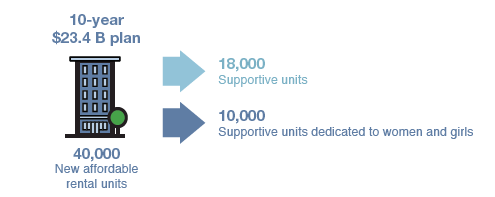

Last December, Toronto’s city council approved its HousingTO strategy. This 10-year $23.4 B plan includes building 40,000 affordable rental units, such as 18,000 supportive units and aminimum of 10,000 affordable and supportive units dedicated to women and girls.

The Housing Now initiative, which the city has described as a “key component” to the HousingTO plan, offers developers surplus city land and other incentives such as tax relief and development charge exemptions, in exchange for ensuring that a portion of the units they construct are affordable units.

Last November, Habitat for Humanity GTA has announced the launch of a $17 M land trust, which will enable the creation of 180 new affordable housing units. The trust is the result of a collaboration between Capital Developments, Metropia, the City ofToronto, Habitat for Humanity GTA, St. Clare’s Multifaith homes, and community group Build a Better Bloor Dufferin.

Via the CMHC, the federal government is investing $357 M into a three-building 836-unit condo project, west of the Distillery District. According to a Waterfront Toronto draft plan, 36% of the project will be affordable housing.

The developers of the site are Dream Unlimited Corp., Dream Hard Asset Alternatives Trust, Kilmer Van Nostrand Co. Limited, and Tricon Capital Group Inc.

At the end of April, Vancouver planning staff presented a plan to the city that advocates a three-stage approach that would seek to stimulate the city’s economy while meeting urgent housing needs.

The first phase of the plan was its COVID-19 emergency response, which provided shelter to people who were homeless or at risk.

The second phase, which would last to the end of the year, would prioritize high-impact affordable housing projects currently in the pipeline, including ‘shovel ready’ affordable and market rental projects expected to initiate construction in the coming months. According to the planning department, there are 15,000 housing units in the application or inquiry stage.

In its most recent budget, the Alberta government is cutting $53 M over three years to affordable housing funding maintenance. Shortly after the cut was announced, the Calgary Housing Company said it is expecting to close 100 units this year because of insufficient funding, and more closures are expected in 2021.

Calgary currently needs 15,000 more units of affordable housing just to reach the national average.

To address this shortfall, the city is selling land that it owns in Saddle Ridge, Highland Park, Banff Trail, Capitol Hill and Seton to affordable housing non-profits, which will build and manage the new housing. Mayor Naheed Nenshi said the sales are expected to create as many as 200 new affordable housing units.

Recently the federal government has announced an investment of $24.5 M toward the construction of a 96-unit rental housing complex in Calgary that is being developed by Truman Homes. The five-storey Mulberry building will offer one and two bedroom homes in the residential district of West Springs.

At least 31 of either the one bedroom or two bedroom units will be available for rent at an annual rate that will be less than 30% of Calgary’s median household income. The rent cap will remain in place for at least the next 21 years.

Financing for the project is coming through the Rental Construction Financing initiative, a National Housing Strategy program delivered by Canada Mortgage and Housing Corporation.

The City of Edmonton is proposing a new framework calling for 16% affordable housing in every Edmonton community. This is an increase from the previous goal of 10%.

Housing starts are expected to fall by at least half until they pick up again in H2 2021 — CMHC.

Prior to the pandemic, Canada’s major cities had rental vacancy rates of sub-2%.

To keep up with the demand, Royal Bank of Canada estimated that the GTA would need to add an average of 26,800 units a year to bring the vacancy rate up to a healthy 3%.

It was estimated that Metro Vancouver needed to build at least 30,000 new rental units over the next two years to balance supply with demand, according to 2019 data from GWL Realty Advisors.

Demand for rental apartment units has been underpinned by strong employment numbers, historically high immigration numbers and lifestyle preferences by both the millennial and baby boomer cohorts.

The employment and immigration demand drivers have since collapsed.

In the last three months, Canada has lost millions of jobs, causing the unemployment rate in May to skyrocket to 13.7%, according to Statistics Canada.

And just before the borders shut down, the Federal government released its three-year immigration plan. It called for record-high numbers of 341,000 permanent residents in 2020, 351,000 in 2021 and 361,000 in 2022. Now monthly immigration numbers have dropped to near zero.

CMHC predicts that housing starts will decline by 51% from pre-COVID levels to 75% in 2020 before starting to recover by the second half of 2021.

“Stymied economic activity, together with recent provincial measures to contain the virus, has slowed residential construction activity in many provinces, particularly in Quebec and Ontario,” CMHC states. “These trends will drive a decline in national housing starts in 2020, leaving the level of housing starts at historic lows in the second and third quarters of 2020. Housing starts are expected to begin to recover in the first half of 2021 as economic conditions improve.”

May housing starts appear to support these predictions. Canadian housing starts, excluding the province of Quebec, fell 20.4% in May compared to April. CMHC left Quebec out of the April survey after construction in the province was disrupted by measures to combat the coronavirus pandemic.

Multi-family starts in urban areas decreased by 27.2%.

In the first five months of 2020, CMHC reports that housing starts were actually up by 18% from the previous year in Toronto, and up by 40% in Ottawa, while they were down by 37% in Vancouver.

Vancouver brokerage firm Goodman Commercial Real Estate reported in June that only 372 rental apartments have started in the City of Vancouver so far in 2020, down from 954 at the same time last year.

“Reduced demand, and higher supply due to the conversion of short-term rental units to long-term rental units, will more than offset the reduced supply resulting from a lower completion rate (of new housing)… and weaker investment activity,” CIBC Economists Benjamin Tal and Katherine Judge wrote in a report on May 1st.

In the longer term, the demand for multi-family housing will resume.

Greg Romundt of Centurion Asset Management writes: “Apartments will be seen as one of the safest sectors not just of real estate, but of the economy in general, as a basic needs industry once COVID-19 is in the rear-view mirror. I expect that long-term flows to apartments will increase relative to other sectors.”

“Multi-family real estate has historically been the most resilient asset class and we think that continues today,” said Anna Kennedy, Chief Operating Officer of KingSett Capital, during an April 30 Real Estate Forums webinar moderated by Stephen Sender.

In this new age of social distancing, multi-family design is shifting away from certain shared-space amenities.

In the last few years, the multi-family and condo developers have been embroiled in an amenities war, with projects offering better and more luxurious add-ons in order to attract residents and to differentiate their buildings from others. Buildings have been tricked out with meditation rooms and outdoor fire pits and everything in between.

Recently, however, building managers have either closed or limited the use of building amenities in order to prevent the spread of COVID-19.

Condo corporations in Ontario, at the time of writing, have been required to keep common element areas closed, as stated in a provincial order issued by the Emergency Management and Civil Protection Act. Once they are lifted, there will be strict municipal regulations to be followed.

“The first line of defense will be to encourage or mandate social distancing around certain share-space amenities, such as a property’s pool and in the gym,” John W. Gray, President of LMC Investments said during a recent webinar by Marcus & Millichap’s Institutional Property Advisors. “Staff will have to watch residents to make sure the amenities will remain safe,” he said.

In this new COVID-19 environment, industry watchers are seeing a shift in amenity trends as a result of the need for social distancing.

Gray also believes that there will continue to be demand for shared-space amenities, but that the coronavirus’ after-effects will be seen in more subtle ways. “Employers may be willing to allow employees to work from home more often, and residential buildings will accommodate this by offering more communal work-from-home space,” he said. This will make upgraded, premium internet access throughout the entire building, imperative.

At the end of March, two-thirds of knowledge-based workers in the US were working from home, according to an estimate from software company Netskope. A similarly timed Colliers survey found that 82% of employees hope to work from home at least once a week after the pandemic.

Crescent Communities Managing Director Ben Kras now thinks that they’ll continue to see the expansion of coworking spaces within multi-family projects.

“I think we’ll see the size of coworking spaces likely increase within projects, and the design will be catered more to, as I call it, the digital nomads, or people who are able to work remotely digitally and are not bound by any specific location,” he said.

Michael Fazio, Chief Creative Officer of New York-based experiential concierge company LIVunLtda, said his team is trying to foster a sense of community in stressful times by curating virtual events that residents can tune into together from their living rooms. Building personalized experiences right now has become increasingly important while communal physical spaces are closed.

Broadstone Arden, a new 335-unit luxury multi-family building in California, closed its gym, pool and club room but launched a virtual dance party with DJ Karma, of Las Vegas, for its residents.

Designers say that post-pandemic outdoor amenities will likely become more important. Pool design, however, will need to be reconsidered, said Patrick Winters, Principal of architectural firm Nadel Inc.

Many of the modifications to make apartment living safer from infectious diseases are already happening, with the promotion and adoption of Passive House, WELL Building and other greenbuilding standards, Architect Michael Liu said.

Amid COVID-19, regular communication with tenants has been central to property management efforts.

Industry sources say that regular communication has been central to management efforts, with technology playing a critical role in how day-to-day business has been maintained.

“Property managers will continue to play an increasingly integral role amid the COVID-19 pandemic,” Stacy Holden, Industry Principal and Director at AppFolio, a property management technology company, tells GlobeSt.com.

Holden states that, “communication and engagement is the key to navigating this event and to curating policies to mitigate rent loss.”

Educating tenants about financial resources available has been a way to support tenants and also to reduce rent loss.

In a survey conducted by Colliers, landlords who took a more proactive approach with their tenants had a higher rate of rent collection. Some of these initiatives included educating tenants on government programs such as EI and CERB as well as percentage rent deferral for tenants unable to make the full rental payment.

A surge in online shopping requires property managers to handle a larger volume of packages safely and efficiently, NREI reports.

“During these initial months of dealing with the pandemic, we have focused on the safety of our team members and residents by implementing a no-touch delivery process,” says Tim Kramer, Vice President and Director of Operations of Draper and Kramer, a Chicago property and financial services company. “This simply means that, for example, when a resident is picking up their delivery, they let us know they are coming, and we place it in an area where they can pick it up without coming into direct contact with anyone else. At our sites with package lockers, we have implemented a much more robust cleaning schedule for the lockers, so they’re wiped down much more frequently.”

Aside from managing monthly income loss, some of the bigger struggles impacting rental-housing providers come from not being able to maintain service quality or make building repairs due to physical distancing requirements. With health and safety being the top priority at all professionally-run buildings, some key operational tasks have been temporarily sidelined, Erin Ruddy writes in Canadian Apartment Magazine.

Virtual showings have replaced in-person tours. Postponement of non-essential work has also impacted operations. This includes things like annual suite inspections, the planting of flowers, pool repairs, changing HVAC filters, cosmetic work for suite turnovers and common areas, and other spring maintenance, Erin Ruddy writes.

Companies have had to implement new work-around procedures essentially on the fly—from how to conduct annual fire alarms in tenant suites, to establishing PPE protocols and implementing hyper-vigilant cleaning practices using hospital-grade disinfectant.

Mark Goodman of Goodman Commercial Real Estate said most owners and property managers are expending considerable resources to stay in contact with and assist their tenants. They are also facing much higher costs for things such as cleaning.

In addition to cleaning its buildings three times a day, Greenwin Property Management has contracted a company to apply antimicrobial bonding treatment to all high-traffic areas and heavily touched surfaces, which is effective for up to six months, says Robert Weiman, Vice President, Quality Assurance and Compliance, Greenwin Corp.

Weiman said that the use of more products as a result of cleaning more often comes at a cost, “but it’s worth it to keep our residents safe. We’ll definitely be following the guidance of Canadian and local health authorities.”

Greenrock Real Estate Advisors has also implemented specific measures. The company is using the GermGuard Treat and Protect Program, which kills up to 99% of germs on contact.

With more residents spending more time at home, electricity and water expenses have gone up. Owners who pay these expenses are facing higher utility bills by about 15%, according to Dan Argiros, the CEO of Q Management, during a Real Estate Forums webinar.

Ultimately, the goal of property management teams, particularly those managing apartments, hasn’t changed. “Many property management companies are primarily focused on their residents and property management teams right now,” says Holden of AppFolio. “They want to ensure the safety of everyone in their properties and provide assurance to all that they are taking preventative measures and following local and national guidance around social distancing.”

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.