Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the content of the 2020 Toronto Real Estate Forum, click the following Insights.

GDP and employment continue to improve; causes a degree of optimism

As COVID-19 spread through Canada early this year, the economy came to a standstill. Businesses and schools closed overnight. Travel came to an abrupt halt. The oil demand took another hit, and unemployment rose 810 bps between February and May.

When Shelter in Place orders lifted, the economy came out of its petrified state, and an initial rebound was swift. After a few short months, recovery has lost momentum, and as we enter a second wave of the pandemic, the government is introducing new relief efforts as it phases out others.

At the end of October, Statistics Canada reported that real GDP grew by 1.2% in August, compared to a 3.1% rise in July.

Its September forecast projected 0.7% growth. Overall economic activity was still about five percent below pre-pandemic levels in February, according to Statistics Canada.

“With the number of new cases of COVID-19 climbing in many provinces, further economic recovery is expected to continue at a much more moderate pace than what has occurred from May through August,” the Conference Board of Canada reports.

The unemployment rate dropped for the fourth straight month in September when the economy added 378,000 new jobs, falling 1.2% from August to 9.0%. The gain, which was stronger than anticipated, brings the employment rate within 720,000 of pre-pandemic levels.

September figures for the Canada Emergency Response Benefit (CERB) showed almost $72.6 B in benefits paid out since its rollout in March, through to the end of August.

The Canada Emergency Commercial Rent Assistance Program (CECRA) came to an end on September 30. The program paid a portion of rent for up to six months, with the government assuming 50% of rent payments and landlords and tenants each paying 25%.

The Parliamentary Budget Office reports that as of September 28, rent assistance has helped more than 120,000 small businesses for a total exceeding $1.68 B in support, which represents about half of the $3 B total program budget. However, the program was criticized by tenants who claimed that they could not access the subsidy without their landlords agreeing to it.

At the time of writing, Ontario “hot zones” saw a resurgence of COVID-19 cases and were returned to a modified Stage 2. Many businesses will need support or will likely not make it past the next round of restrictions. On October 9, the federal government has said it will be rolling out targeted aid for businesses hit by second wave closures.

This support will include an overhauled rent relief program, which the government said will now allow businesses to apply directly for relief through the Canada Revenue Agency until June 2021.

The Liberal government promised to create more than one million jobs to rebuild from the pandemic in their September 23 throne speech.

“Climate action will be a cornerstone of our plan to support and create a million jobs across the country,” the speech specified. “This is where the world is going.”

On October 1, as part of its pandemic economic recovery strategy, the Liberal government also announced $10 B in infrastructure spending. The three-year plan is expected to create 60,000 jobs. One of the plan’s major initiatives includes $2 B for large-scale energy-efficient building retrofits.

According to RBC Economics, stimulus and relief spending has already added up to $265 B or 12.2 % of Canada’s GDP, even before adding the cost of expanded Employment Insurance benefits or paying for promises made in September’s Speech from the Throne.

Bloomberg reports that the rising debt levels have “triggered a backlash from business groups and economists, who are calling on Trudeau to commit to specific new debt targets to impose discipline on the budgeting process.”

Economist David Rosenberg wrote in the Financial Post, “The pace of the rebound may have come as a surprise, but the winding down of fiscal support (most notably, the transition away from the Canada Emergency Response Benefit to a modified Employment Insurance program providing less income), the rolling off of mortgage and loan deferrals from the major banks and the resurgence of the coronavirus all pose downside risks to the economy.”

H1 2020 Canadian investment volumes at $19.7 B is down 20%, according to Altus Group

At the end of H1 2020, Altus Group reported that Canadian investment volumes had totalled some $19.7 B, a significant 20% lower from the same time in 2019.

Investment was strong coming into 2020 as momentum from 2019 carried over in the first couple of months of the year. Large deals negotiated in the fourth quarter of 2019 made up a good portion of transactions that closed at the beginning of 2020. Also, deals that closed in Q2 were underway before the pandemic forced an economic shutdown. This was one reason that investment levels in April exceeded those in March despite most of the country being on lock-down, according to CBRE.

According to Altus Group, the office sector experienced the largest dip in volume compared to other asset classes and recorded only 100 transactions in the second quarter, dropping 73% from Q2 2019, and 52% from the first half of 2019. With the surge in remote work and as tenants re-consider their use of office spaces, Downtown Class “AA” Office cap rates rose slightly to 5.53%, up from 5.36% in the same quarter last year, and 5.30% in Q1 2020.

The number of deals greater than $100 M in value has dropped significantly. Averaging 8 to 10 transactions per quarter, CBRE calculates just one transaction in Q2 in this range, excluding M&A activity: the Landing Office complex in Vancouver acquired by Allied REIT for $225 M.

The next largest transactions were 245 Lena Crescent, a multifamily property in Kitchener-Waterloo, acquired by QuadReal for $98.9 M and 395 Terminal Avenue, an office asset in Ottawa, bought by BentallGreenOak for $97.5 M.

The largest sale transaction in Canada to occur during the pandemic this year was BentallGreenOak’s acquisition of 50% interest in Toronto’s Waterfront Innovation Centre from Menkes for $250 M, or $526 PSF. The 475,000 SF office and retail development adjacent to Sugar Beach is currently under construction and is scheduled for occupancy in 2021. In Q3, InterRent REIT acquired five multifamily properties in southwestern Ontario consisting of a total of 723 units for $170.7 M.

On the first day of Q4, US-based Equinix REIT’s acquisition of Bell Canada’s Brampton Data Centre closed. Located at 30 Bramtree Court and 1895 Williams Parkway, this was one of 13 Bell Data Centres that Equinix bought for a total of $1.041 B.

Industrial investment volumes, however, have outpaced H1 2019. The Vancouver, Montreal, the GTA /Greater Golden Horseshoe markets all saw growth in the industrial sector during this time period Altus Group reports. Single and multi-tenant industrial remain the top-two preferred asset classes in their Q2 Investment Trends Survey.

Retail investment volumes have fallen sharply and totalled only $1.5 B in the first half of the year, the lowest two-quarter performance in almost a decade. Most retail landlords have turned their attention to managing their assets and working out rent deferral agreements with tenants, and they are postponing any new acquisitions or developments to preserve capital, JLL noted.

Greater Toronto investment volumes in Q2 2020 totalled $3.8 B, down by 37% compared to Q2 2019, and Altus Group reports that this was the first time quarterly totals fell below $4 B since Q1 2016.

On inspection, a good chunk of Q2 investment was the result of two transactions:

- Ontario Power Generation’s $1.3 B acquisition of two GTA power plants from TransCanada - the Halton Hills Generating Station for $750 M and the Portlands Energy Centre for $578 M.

- The nine-property, 509-unit portfolio that Timbercreek Asset Management bought from Flagship Property Ventures for $143.4 M.

Deal volume dropped by 29% in Q2 compared to the same time period in 2019. “Impacts from the pandemic were reflected in the market most significantly in May – registering only 106 transactions and an investment total of $471 M, which was a drop of 68% from May 2019,” Altus Group reported.

Nationally, the most active purchasers in Q2 2020 were private Canadian Investors. This group accounted for almost 60% of acquisitions, CBRE stated. Over the last decade, participation by this investor group had never exceeded 46.7%, “illustrating how nimble and opportunistic well-funded private investors can be during times of crises,” the company observed.

Of the investment environment, JLL noted, “Buyers and sellers have been far apart on pricing. Most sellers are well-capitalized and unwilling to sell in a downturn or to offer a ‘COVID discount.’ The very logistics of touring assets has been a challenge and contributed to friction in the marketplace. The resulting lack of comparables makes it even more difficult for groups to assess and agree upon value.”

Commercial mortgage spread increases as lenders price in elevated risk associated with certain asset classes

Last March, many commercial lenders put a hold on lending activity while dealing with the volume of deferral requests and waited for the markets to normalize.

Market liquidity deteriorated as lenders assessed the uncertainty around borrowers’ ability to service debt, CMLS Capital observed.

Requests for loan deferrals slowed going into Q3, JLL reported. “Some lenders provided deferrals across the board while others were more bespoke. However, a disproportionate number of requests were made for retail and hotel assets. Deferrals are generally granted on the condition that they are repaid over the remaining term of the loan,” the company stated.

The Canada Emergency Commercial Rent Assistance (CECRA) program has helped maintain some confidence in the market and “cushion” the impact of the pandemic on the commercial lending space, Michel Durand, CEO of Mortgage Alliance Commercial stated.

However, some industry experts believe that measures like the Canadian Emergency Relief Benefit (CERB) have flowed through to landlords far more effectively than Canadian Emergency Commercial Rent Assistance (CECRA) for the office and retail sectors.

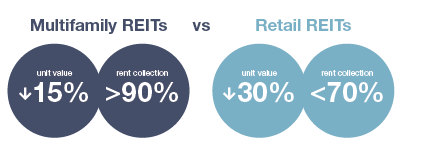

That’s reflected both in a lower level of rent default and a higher level of confidence from public markets and lenders, REMI Network reports. “Industrial and multifamily REITs have experienced the least erosion in unit value during the crisis, with multifamily REITs down about 15% versus nearly 30% for office and retail REITs. Multifamily REITs also report upwards of 90% or more in rent collection versus less than 70% for retail REITs.”

Lending activity increased by the end of June but in a more cautious fashion.

“Debt liquidity is now being dictated by asset class outlooks and the ability of sponsorship to operate under current economic conditions,” writes CBRE’s Carmen Di Fiore, Executive Vice President, Debt & Structured Finance.

“While credit spreads have come in during the last quarter, the range in cost of debt between best- and worst-in-class has widened materially,” Di Fiore stated.

Multifamily, industrial and grocery-anchored retail is viewed more favourably, while lenders are reluctant to finance hotel and non-core retail, JLL has observed.

As of Q3 2020, the spread between cap rates and bond yields were at their widest on record at 510 bps, according to CBRE Research.

According to Craig Solomon, CEO of Square Mile Capital, one of the challenges for real estate debt fund managers is knowing what spreads are necessary to compensate for market risk while pricing their debt in order to be competitive. Trying to do that in an environment of constrained transaction volume is rather difficult.

In their mid-year Canadian Investment Outlook, JLL reports that “underwriting has been a challenge and therefore lending has been conservative; loan sizes and loan-to-value ratios have largely been reduced since March. Acquisition lending activity has slowed commensurate with a slowdown in overall investment activity. However, this has been offset by an increase in refinancing activity by borrowers looking to take advantage of lower mortgage loan rates.”

“Ten-year commercial mortgage spreads for Class A properties jumped from 170-180 basis points end of 2019 to 250-275 basis points at the end of June 2020, offsetting some of the drop in the GoCs during this period. Conversely, banks pushed the cost of funds higher in Q2 due to fear of liquidity insufficiency but keeping spreads stable. Debt funds remained steady with their overall interest rates,” reported JLL.

Preqin reports that over 1,000 institutions currently allocate to private real estate debt, and as of December 2019, the industry stood at US $190 B in aggregate assets under management – doubling in size since 2014. Debt funds also had about US $61 B in dry powder at the end of last year.

However, as of October 2020, Preqin reports that just three Canadian-based closed-end private real estate funds closed with an aggregate value of $600 M. This is down significantly from seven in 2019, which had an aggregate value of $15.9 B.

While lenders remain concerned about the actual economic impact of COVID-19, in general, the market is recovering from the lending freeze that occurred at the end of March, JLL observed.

Cities have the opportunity to rethink space in order to become more equitable and more resilient

“Every major calamity – from the 19th-century cholera outbreaks to the 2013 floods in Calgary – has provided valuable lessons in better city-building,” said John Brown, President of the Royal Architectural Institute of Canada.

COVID-19 gives us the opportunity to rethink how space is used, and to transform spaces that will help make the city more resilient to future upheaval – whether it be climate change or another pandemic down the line.

The possibility of pandemics will continue to exist, writes Oliver Schaper, Design Principal at Gensler. He sees that building stronger, more resilient communities is necessary to withstand future disruptions, creating spaces that can adapt to quarantine and surge-demand conditions. According to Schaper, changes will be required in areas that were already in need of attention, and new opportunities will emerge along the way.

In an interview with CTVNews.ca, Jason Thorne, Hamilton’s General Manager of Planning and Economic Development, said that COVID-19 had brought more dining and retail outdoors because of capacity limits.

“I think we could see investors and entrepreneurs really consider opportunities for outdoor space when making decisions going forward. That adaptability of space will be important so that we’re not boxing ourselves in so we can only use space in one way,” he said.

Many cities have reported a drop in public transit use during the pandemic. Ahsan Habib, Director of the School of Planning at Dalhousie University, says that it’s likely to remain lower than usual in the short term.

Toronto Transit Commission CEO Rick Leary stated that 25% of lost TTC ridership might not return post-pandemic. In September, ridership was at 18% compared with the year before.

Former transit users could resort to personal vehicles such as scooters and e-bikes, which had already been trending before the pandemic. With the eventual adoption of personal autonomous vehicles, space will be needed to accommodate these alternative modes of travel.

Many major cities worldwide have closed roads in order to facilitate the movement of people in a socially distanced manner, especially since many have opted out of public transit.

To accommodate more cyclists and pedestrians, Vancouver closed down part of Stanley Park to cars last April. The ActiveTO program, which was developed by Toronto Public Health and the transportation department, saw Lake Shore Boulevard and Bayview Avenue closed to cars on the weekends.

“Parks and open spaces really prove their value in this current environment,” said Rachel MacCleery, Senior Vice President at the Urban Land Institute. They form a “natural network” with streets and can be used to create alternative ways for people to move within a city, she observed.

In the last few months, people have become more reliant on their immediate neighbourhoods to bring them the goods and services they require.

“The 15 Minute City” is an idea that was developed by Professor Carlos Moreno at the Sorbonne in Paris. The definition of it is that everything that you need on a daily basis – your home, work, shops, schools, healthcare – is located within a 15-minute walk or bike ride. It is a concept that is being embraced in cities such as Paris, Edmonton, Portland, Detroit, Dallas and Chicago.

It is also gaining traction during COVID-19 as a way to promote the health and well-being of city inhabitants.

In fact, the C40 Cities Climate Leadership Group pledged in May “to build a better, more sustainable and fairer society out of the recovery from the COVID-19 recovery.” The cornerstone of the group’s policy agenda is the transformation of the world’s megacities into “15-minute cities.” C40 is a network of the world’s megacities committed to addressing climate change and has 97 member cities, including Montreal, Toronto and Vancouver.

According to the C40, following such a model will promote equitable access to jobs and government services and rebuild areas economically hard-hit by the pandemic among global cities.

A central theme of the Mayor’s Agenda for a Green and Just Recovery, released in July by C40 Cities, is that cities are the “engines of the recovery,” and investing in their resilience is the best way to avoid economic disaster.

In line with the national average, sublet space represents approximately 36% of vacant space in Toronto, as occupiers reassess their space requirements in the evolving economy

Office vacancy rates have continued to rise as work from home is projected to last through to 2021. According to Altus Group, the national vacancy rate increased to 10.1% in Q3 2020 from 9.6% in the previous quarter and 9.9% in Q3 2019.

Nationally, sublet availability jumped from 15.7% in the previous quarter to 17.2% in Q3 2020, with 12 MSF of sublet space on the market. Toronto has 4.4 MSF sublet space available, which is the highest among major markets, Altus Group reports.

Rents, however, have ticked slightly higher from the previous quarter. According to CBRE, Class A office net rents rose in Toronto to $35.90PSF, up from $34.77 PSF one year ago, while on a national level, rents are up to $22.25 PSF from $21.93 PSFin the previous quarter.

Q3 2020 Downtown Toronto office vacancy rate rose by 2% to 5.1% quarter-over-quarter and increased from 3.4% in the same quarter last year, Altus Group reports. Colliers noted that it is primarily the tech industry that is giving back space. This is an indication that the sector is reassessing their space requirements as many companies pivot towards a remote workforce as a permanent element of their culture.

However, despite companies such as Twitter, Slack, Shopify, Infosys and Zillow enabling at least a portion of their workforce to permanently work remotely, Amazon announced in September that they will be expanding their office footprint and will be hiring another 3,500 employees. The company revealed that 3,000 of the jobs would be done out of the Post, their newly constructed office building in Vancouver, where Amazon will take over an extra 678,126 SF of office space. The Canadian Press reports that by 2023 it will be operating across 18 floors in the building’s north tower and 17 in its south tower.

The company will also hire new workers in Toronto, where it will lease 129,000 SF at 18 York Street. The intent is for workers to be in the building by next summer.

Across the road, Cadillac Fairview completed construction of 16 York Street. The development was 86% pre-leased and added 879,000 SF to the Downtown South submarket. This represented most of the almost 1.2 MSF of new space that was brought on the market in Q3. Other office completions included the 161,000 SF 500 Lakeshore Blvd W and 133,000 SF 99 Atlantic, both fully pre- leased, according to CBRE.

As of Q3, there is almost 9 MSF under construction in downtown Toronto – accounting for two-thirds of all inner-city office space under construction in Canada’s major cities. It is estimated that all this new supply will increase vacancy to top 8% by H2 2023.

Average rental prices are declining as small investors and professional landlords try to attract clients from a diminished pool of potential renters, according to Statistics Canada

Month after month, demand repeatedly outpaced supply in Toronto and in Canada’s other key housing markets. This trend came to an abrupt halt in mid-March 2020.

When COVID-19 hit Canada, the demand for rental housing decelerated swiftly. The drivers of this demand – economic growth, immigration, employment, tourism – declined virtually overnight.

Urbanation’s survey of purpose-built rental apartment projects that have been completed in the GTA since 2005 reported a vacancy rate of 2.4% in Q3 2020, which was three times higher than in Q3 2019 (0.8%) and the first time vacancy rates surpassed 2% in the GTA in 10 years.

Not only has demand decreased, but supply also has. Added to the fact that former Airbnb units have now added space to the rental stock, there has been a surge in new unit completions.

Urbanation reports that 988 new units will have been completed by the end of 2020.

More units are on the way down the road.As of Q3, 13,663 purpose-built rental units were under construction. Some 5,276 of these are scheduled for completion in 2021 – the highest level in more than 25 years, the company reports.

The combination of decreased demand and an increase in supplyhas produced lower rents in the GTA.

According to the latest data from Rentals.ca, rents in September were down 9.5% overall, with rents in downtown Toronto for a one-bedroom unit dropping below the $2,000 mark for the seventh straight month.

Urbanation found that the reported decline in rents was in addition to incentives landlords have started to offer new tenants.

Out of 50 purpose-built apartment complexes in the city they track, 29 offered incentives during the third quarter. The types of incentives include free parking, one or two months of free rent, and move-in bonuses of up to $1,500.

The eCentral in midtown Toronto and The Selby located south of Bloor East are offering one month of free rent for select units. 18 Erskine at Yonge & Eglinton was offering two months free and a $1,500 bonus. These are all newly built rental buildings.

For landlords, there are further headwinds. The Ontario government announced in August that it would be freezing residential rents in 2021. Rents were on track to rise by 1.5%, as set out by previous rent-control guidelines.

Still, a vacancy rate of 2.4% is extremely low. Observers feel strongly that demand will return to the GTA post-pandemic, eventually pushing rents back up. Incentives will not likely be around for long.

Low interest rates have made homes more affordable, and the WFH trend means that people are not as concerned about being located close to the core

COVID-19 has accelerated interest in the suburbs, but this trend predates the pandemic. This interest has been fueled by millennials who have reached prime home-buying ages.

“Millennials are driving much of the market now,” Diana Petramala, a Senior Researcher with the Centre for Urban Research and Land Development at Ryerson University, told Toronto Storeys. “We have underestimated the impact of millennials on housing markets and overestimated the impact of boomers.”

Affordability and space are the biggest considerations for those moving to the suburbs and even exurbs, says Petramala.

“The move to towns and secondary municipalities — called exurbs — that are beyond reasonable commuting distances from large urban centres have nevertheless gained popularity,” says Phil Soper, CEO of Royal LePage.

Eight of the ten fastest appreciating Canadian exurbs are in Ontario, led by areas surrounding Windsor, London, Kitchener-Waterloo- Cambridge, Kingston, Niagara/St. Catharines, Hamilton, Belleville/Trenton and Guelph, Soper said.

According to brokerage Zoocasa, areas in the GTA that set new home price records in August were farthest from the city centre: Ajax, Burlington, Brampton, Clarington, Essa, Halton Hills, Innisfil, Mississauga, New Tecumseth, Oshawa and Scugog and Whitby.

The average price in Durham Region reached $734,136, a 19.5% increase compared to last year. The area reported over 1,500 residential transactions in August, a significant 45% jump from the same time last year.

Vaughan is another suburban city that is booming. During the first quarter of 2020, 656 residential and commercial building permits were issued with a value of more than $128 M, according to Mayor Maurizio Bevilacqua.

Companies such as KPMG and Harley Davidson Canada have opened offices there, and PwC Canada opened an office in Vaughan in November 2019. Frank Magliocco, the company’s national real estate leader, said 300 employees work there, 100 of whom relocated from the downtown Toronto office.

“I think in the past, these bedroom communities didn’t have any vibrancy, but what we’ve seen is that some of these communities have nightlife, restaurant scenes, entertainment scenes and I think people are enjoying that aspect of it,” Magliocco said.

Avoiding public transit makes working in the suburbs more attractive relative to the urban core. Accordingly, occupiers are looking at hub- and-spoke model options, Cushman & Wakefield reports.

“Many corporate occupiers are saying let’s have a downtown hub, and suburban west, east and north spokes so that people can have their office close to their home if and when they want to go to the office,” says Sheila Botting, President for the Americas at Avison Young.

Suburban office markets have performed well over the past few years. Historically, vacancy has been higher in the suburbs. However, Cushman and Wakefield states that in the US, the gap between the CBD and the suburbs has shrunk from a high of 406 bps in 2008 to 35 bps as of Q1 2020.

To facilitate travel through the GTA, significant extensions to the 400 series highways are in various development stages.

The extension of Highway 407 to Highway 35/115 has been complete for almost a year, cutting the time it takes to get to Peterborough to around an hour.

In January, the 10 kilometre Highway 418 opened. The north-south road connects the 407 with Highway 401 between Courtice and Bowmanville.

The $616 M widening and expansion of Highway 427 is progressing despite the challenges presented by COVID-19. Four kilometres of the existing highway from Finch Avenue and Highway 7 is being widened, and the roadway is also being extended 6.6 kilometres from Highway 7 to Major Mackenzie Drive.

The province is moving ahead with the GTA West Corridor (known as Highway 413) and plans to have an Environmental Assessment completed by the end of 2022. The route will cut across Halton, Peel and York regions, starting at Highway 407/401 interchange in the west, and connecting to

Highway 400 just south of King Road. The proposed route will also connect to the expanded Highway 427. Highway 400 is undergoing expansion from six to eight lanes along the 11 kilometre stretch between Major Mackenzie and King Road. Bridge widening that is taking place in Barrie will accommodate future widening of Highway 400 from six to 10 lanes.

Statistics from the Barrie and District Association of Realtors show 1,021 homes were sold within the city during Q3 2020, a 54.9% increase compared to the same period last year. Home prices also rose 16.8% to $574,023 compared to 2019.

In greater Simcoe County, excluding Barrie, 2,323 units were sold. This is an increase of 55.5% compared to the third quarter of last year. Homes in this area also had an average sales price of $634,586, up 24.7% from the same period in 2019.

5.3 MSF of new product delivered in Q3, but vacancy in the GTA remains at rock-bottom

National industrial absorption reached 6.6 MSF in the third quarter of this year, according to CBRE numbers, outperforming initial expectations for 2020.

According to Altus Group, the national vacancy rate at the end of the third quarter was 2.2%. This rate is up slightly from 2.1% in the previous quarter but remains very tight.

Vacancy rates are up across most major markets compared to the same quarter last year, except for Ottawa, Vancouver and Montreal. Toronto, Montreal, and Vancouver now have the tightest vacancy rates.

Rent escalations in key labour and logistics corridors including Mississauga ON, Delta BC and Laval QC helped the national net rental rate remain near its all-time high of $9.17 PSF, which was set in Q2 2020, CBRE reported.

Demand continues to be largely driven by an acceleration in e-commerce activity as a result of the pandemic.

Statistics Canada reports that online shopping by Canadians has doubled during COVID-19, and now constitutes 10% of all shopping by Canadians. In the US, Moody’s Analytics estimates that the share of e-commerce spending relative to total retail sales increased from 11.4% at the end of 2019 to a historic 16.4% in March and April alone. This has fuelled an increase in demand for warehouse and distribution space across North America.

“As e-commerce gains traction and an increase in storage and distribution facilities are needed, the industrial asset class is expected to see growth in a tight market, requiring the construction of new facilities,” CBRE stated in a recent report.

Supply chain disruptions experienced by some companies during the pandemic have also prompted them to keep more inventory on hand, leading to an increased need for storage space.

Evidence of this demand has been seen with numerous large- scale development lease transactions, as well as a surge in new construction in the GTA.

Notable leases in the third quarter were design-builds with expected delivery dates through 2024 and included Amazon’s 1.1 MSF in Ajax, Avison Young reports. Walmart leased 550,000 SF at 11110 Jane Street in Vaughan for a new distribution centre, and Brewers Retail signed a deal for 437,500 SF at HOOPP’s iPort development in Caledon.

The Canadian government completed a deal for over 350,000 SF at 2675 Steeles Avenue West. This facility will act as a stockpile for personal protective equipment and is a direct example of how the ongoing pandemic has increased the need for industrial real estate for some users, JLL observes.

Seventeen buildings reached completion during the Q3 in the GTA, most of which was pre-leased, Avison Young reports. Of the 3.2 MSF that was brought to market, 92% was already absorbed. Included in this total is Amazon’s million-square-foot fulfillment centre in Scarborough.

According to Altus Group, the GTA saw 52 buildings under construction, totalling 13.5 MSF in Q3 2020, with 8.7 MSF already pre-leased. There are 144 buildings currently pre-leasing, with 46.6 MSF potentially coming to the market, a significant increase from 2019.

“Commerce is being raised from the dead, online, offline, and everywhere in between.” – Nick Winkler

Retail sales rose by 0.4% in August 2020, with year-to-date growth remaining positive at 1.7%, according to Statistics Canada. Their preliminary estimates suggest no change for September.

On a category basis, figures remain down in three of nine core categories. Clothing & Accessories posted a decline of 30.6% compared to the same period last year while food & beverage sales rose 10.1% as Canadians stocked up and dined at home, CBRE reports.

These numbers underscore the bifurcation within the retail sector. While enclosed malls have been hit much harder by the pandemic, grocery-anchored retail continues to outperform.

An essential service during the pandemic, grocery stores have developed a series of measures designed to protect their employees and customers and therefore maintain higher levels of in-store shopping.

While these protocols aren’t standardized, they have included reducing the number of entrances into the store; limiting the number of customers inside at any given time; marking a safe distance between shoppers; and in some cases, introducing one-way aisles.

It’s not just grocery stores that have implemented these kinds of measures.

Best Buy Senior Vice President Mat Povse told Retail-Insider that the company has “re-engineered and re-floored” to redirect the movement of customers.

“We’re very clear on how customers walk into our stores. If you come in to pick up a product versus coming in to walk around and shop the store, we acknowledge that before you enter the store, and we manage the lineups that way as well,” he said.

National retail vacancy rose 100 bps to 4.1%, according to CBRE’s mid-year survey of select retail REIT portfolios. This was one of the largest half-yearly increases on record. All retail formats have been impacted with regional shopping centre vacancy increasing by 190 bps to 7.7%, the company reports.

JLL writes: “Real estate investment trusts Morguard, H&R, and SmartCentres reported that, while April’s rent collection averaged around 80% for open-air and 45% for enclosed, July’s rent collection rose to 85% for open-air and 60% for enclosed retail assets.

Between March and the end of September, over 40 brands have announced the intention to shutter some or all their stores in Canada. These announcements amount to more than 1,100 stores that will close in the next year, with many experts speculating that there are more closures to come.

Retail-Insider reports that bankruptcies and store closures are expected to peak in early 2021 after the holiday retail season has ended.

With more vacancies anticipated to come to market, there will be many new opportunities for both existing and new concepts that are in a good financial position to take over high-profile locations not available to them in years past.

One new concept retailer is Mad Radish. Developed by David Segal of DAVIDs Tea, there are now six locations – three in Ottawa and three in Toronto – with more on the way. Segal has launched two new brands, Luisa’s Burritos & Bowls and Revival Pizza, which will be sold at this higher quality fast-food chain, a dining category that Segal believes is lacking in Canada.

On the restaurant front, a new survey done by the Canadian Chamber of Commerce finds that 60% of restaurant owners say that they cannot operate with social distancing measures in place and may have to close.

Global chicken chain Nando’s has already closed 21 of its Canadian locations since the beginning of the pandemic.

The ghost kitchen concept gives the restaurant industry a new way to evolve and possibly keep afloat. A concept that started cropping up a couple of years ago, ghost kitchens contain all the equipment needed for the preparation of meals, but has no dining area. Restaurants may use a ghost kitchen and have a different physical location for customers, or they may be open for delivery only, facilitated by apps like Uber Eats and DoorDash. Some ghost kitchens host several different brands. Some restaurants have expanded into these kinds of virtual kitchens. Some have launched virtual brands – food concepts that are available only by delivery.

The growth of food delivery services has enabled the rise of ghost kitchens. Food delivery sales reached $4.1 B in Canada in 2019, up 85% from just three years earlier, according to Ipsos Canada –also influenced by the pandemic which has forced the shut down of restaurants and led to the avoidance of dining among strangers.

Despite the challenges faced by this sector of the past few years, 1.3 MSF of new supply was completed in H1 2020, as reported by CBRE. “Several project timelines were pushed out to yearend and if they remain on schedule, could see a further 3.2 MSF delivered in H2 2020, a half-year high not matched since H2 2016,” the company states, adding that mixed-use projects account for 69.8% of under construction nationally – the highest level on record.

Adoption of new technologies is making businesses nimbler and resilient to future disruption

From ‘nice to have’ to ‘need to have,’ the industry has had Proptech adoption thrust upon it. Companies have had to innovate quickly to order to ensure some form of business continuity.

Proptech solutions that aid in the movement of people and those that support safety and wellness efforts have become essential for commercial real estate.

Contactless building access, such as keycards, smartphone access or smart locks, is one that has been gaining a lot of traction, especially as people return to work. This trend was already emerging before the pandemic, but interest is now accelerating as people try to avoid touching surfaces.

Technology is being developed to help companies comply with social distancing protocols by managing the number of people in the workplace.

Global design and architecture firm Gensler has developed a physical distancing tool called ReRun. Using algorithms, ReRun can quickly generate many scenarios and identify the most optimized plan for a variety of physical distancing conditions, regardless of the size of the organization.

As workplaces begin to phase in more employees, ReRun can continue to generate scenarios that increase in density to help inform organizational return planning strategies, Gensler says.

German startup Thing Technologies (Thing-it) has developed a new digital solution called Virus Guard that helps reduce the risk of infection. Virus Guard provides an easy-to-operate solution to control the in and outflow/presence of people in a building using sensors.

Destination dispatch systems are being designed to optimize elevator efficiency and reduce elevator trips combatting the backlog at the elevator banks. The system determines which passengers need to go to which floors and assigns cars based on that need. “In comparison to conventional elevators, destination dispatch increases efficiency and speed by over thirty percent,” Susan Brown writes in Propmodo.

Elevator company Schindler Group has created a suite of clean and touchless services as well as “passenger space solutions.”

Microshare is a tech company that specializes in sensor-based data products, including predictive cleaning, asset tracking, contact tracing, and occupancy monitoring.

IoT technology provides space usage data, which can be used to assess allocation for new cleaning demands. Cleaning supervisors and staff can respond to clean the used spaces and not waste resources where they are not required.

Also notable is that property owners have begun to use software systems to monitor a tenant’s default risk.

Bison.box from the German software company control.IT has put out a product that does just this. Another is US-based Till, which tracks the income and expense patterns of multifamily tenants to create custom rent payment schedules, thereby reducing late payments and preventing evictions. It also gives landlords a real-time picture of the health of their rent rolls, according to Zak Schwarzman, General Partner at VC firm MetaProp.

The 2021 PWC Emerging Trends report forecasts that the same business continuity solutions – videoconferencing, cloud technologies, etc. – that have kept real estate companies operating, are expected to generate continued demand next year, as are those that support safe re-openings of office and retail properties.

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.