Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the content of the 2020 Vancouver Real Estate Forum, click the following Insights.

Almost half of the jobs that were lost have been recouped, but the economy is expected to contract by 5.4%.

On March 18, 2020, British Columbia declared a provincial state of emergency under the Emergency Program Act, which has been in place until at least August 18, 2020.

On March 23, BC announced a $5 B COVID-19 Action Plan that dedicates $2.8 B to help people and fund the services they need to weather the crisis, and $2.2 B to provide relief to businesses and help them recover after the outbreak.

Specifics of the plan include:

• A one-time $1000 Emergency Benefit for Workers

• A six-month freeze on student loan payments

• Postponed tax increases that were scheduled for April 1

• Postponed tax deadlines for businesses

• An increase in the BC Climate Action Tax Credit for July 2020

The COVID-19 Action Plan includes $1.5 B that earmarked for an economic recovery plan on which the government is consulting the public.

The tourism industry is asking for almost half of this amount. Tourism has nearly disappeared from Vancouver, and the industry may lose as many as 72,000 jobs, warns Ted Lee, acting CEO of Tourism Vancouver. The Tourism Industry Association of BC is asking the province for $680 M of the recovery fund to help them remain afloat.

Dayna Miller, Director of global partnerships for Tourism Vancouver, said that last year, Metro Vancouver alone had 11 million visitors who brought in an estimated $9.8 B in total spending.

This year, Tourism Vancouver is forecasting four million visitors and a 68% decline in total visitor spending.

A ban on large cruise ships until October 31 has essentially cancelled the cruise ship season. An estimated 1.3 million cruise ship passengers on 310 ships were scheduled to port in Vancouver in 2020. Each ship translates into $3 M in tourism spending.

In the first week of July, Vancouver hotels were at 22% capacity compared to 89% in 2019, as calculated by the BC Hotel Association. About 20 hotels remained closed as of the beginning of July, representing 30% of the total number of hotels in the city.

Prior to the pandemic, the Conference Board of Canada projected that BC’s GDP would grow by 3% in 2020. In a June update by the province, these numbers were adjusted to reflect a harsh, new reality — GDP is now forecasted to contract by 5.4% this year.

Nearly 400,000 jobs in March and April were lost across BC. The province gained back 233,000 of those jobs, and the unemployment rate has now fallen from 13.4% in May, the highest it has been since 1987, to 11.1% in July, according to Statistics Canada.

A drop in revenue due to reductions in retail sales, corporate profits and tax revenues combined with $5 B in emergency relief measures means that the province could face a $12.5 B deficit this fiscal period. These numbers are a drastic change from the $227 M surplus that was projected back in February when BC unveiled their budget.

Occupiers are re-assessing their space requirements in light of tighter cash flows and work from home policies.

The Metro Vancouver market experienced 30,850 SF of negative net absorption in Q2 2020, primarily driven by Downtown sublets, which grew from 195,021 SF in Q1 to 594,751 SF in Q2, JLL reports.

According to Altus Group, Vancouver Market Area vacancy increased by 10 bps QoQ to 4.7% at the end of Q2. Downtown Vancouver vacancy increased for the third consecutive quarter since Q4 2015, from 3.1% in Q1 2020 to 3.7% in the second quarter of the year. It remains the second tightest market in Canada, following Toronto.

Average rents have continued to climb, both in downtown and the suburbs. JLL notes that the spread is widening between what the tenant is willing to pay and what a landlord is offering, which is causing a stall in deal activity.

Two significant downtown transactions in the second quarter were Lululemon’s lease extension of 88,362 SF, and 82,000 SF of office space that SNC-Lavalin vacated at 745 Thurlow Street as they move part of their offices to 3777 Kingsway, CBRE reported.

The suburbs performed comparatively well with Burnaby, Surrey and New Westminster all showing positive absorption this quarter, according to Collier’s numbers. In Burnaby, there were several large deals initiated before COVID-19, including Chemetics Inc. lease extension of 55,000 SF in Broadway Tech Centre and South Coast BC Transportation Authority leasing 23,000 SF in 4555 Kingsway.

Q2 2020 saw 44,784 SF of new supply in office space that is fully leased at 1575 West Georgia Street in Downtown Vancouver, Altus Group reports. There is 3.8 M SF office space under construction and is 70% preleased.

Only minor construction delays have been reported.

Westbank’s 75,000 SF space at the Vancouver House development is complete and leased to Global University Systems, who will take occupancy in the fourth quarter.

Oxford Properties’ nine-storey, 150,000 SF building at 402 Dunsmuir St. was completed in Q2. It was fully preleased by Amazon.

Statistics Canada reported that 4.7 million Canadians started working from home in March. Many surveys have shown that people like the flexibility and not having to commute to the office. Companies have realized that productivity has not been hindered, and this will undoubtedly lead to a change in work practices.

Magnus Meyer, Managing Director of WSP Nordics & Continental Europe, stated that “The typical tenant will start thinking that maybe they don’t need space for 100% of their employees, maybe only 75% or 60%. Or they might not expand because of the crisis, but just work with the space they have.”

There is a consensus that the type of work done at the office will change.

“People won’t go back to sit in the office and just work. They can do that at home. They will want more when they come back. They will want to learn and collaborate and connect in the office,” says Didhiti Bhoumik , Chief Administrative Officer at Borden Ladner Gervais.

Pi Labs Founder Faisal Butt puts it, “remote working won’t spell the end of the office, given that 87 percent of global corporations view real estate as a key strategic asset rather than just a place for people to go do their jobs. Not all jobs can be done remotely, and many firms will still favour the social and collaborative benefits that can be fostered through in-person working relationships.”

Vancouver continues to attract major tech firms and is 12th in CBRE’s 2020 North American Tech Talent Ranking.

There are over 100,000 technology professionals across BC, with almost 85,000 working in Metro Vancouver. In addition, there are more than 10,000 tech companies across BC, the Information and Communications Technology Council reports.

The industry generates more than $23 B in revenue and adds $15 B to the GDP in Vancouver, and is growing by 6% per year, accordingto the Economic Commission.

Before the pandemic struck, CBRE stated that Vancouver’s office sector was “becoming increasingly crunched for space, as technology giants expand their footprint in the Pacific Coast city, lured by a strong labour pool, friendly immigration policies and proximity to US West Coast company headquarters.”

At the beginning of the year, Shopify leased 70,000 SF in Bentall Centre. The company says it will be hiring 1,000 workers in the city for its new research and development centre. The office is set to open in late 2020.

However, in May, Shopify told its employees that it would permanently allow them to work from home. It spent US $37.1 M in Q2 reconfiguring office space and closing down “secondary offices in major cities.” Chief Operating Officer Harley Finkelstein declined to say which cities closures would occur in, but mentioned that “we are committed to retaining a physical presence in each major city that we currently have spaces in, which includes Ottawa, Toronto, Waterloo, [Ont.], Montreal, Vancouver and several international locations.”

In the first half of 2020, Israeli FinTech company, Tipalti, opened its third location with its Vancouver office. The company was founded in 2010 by CEO Chen Amit and Chairman Oren Zeev. Tipalti has offices in Kibbutz Galil Yam (Israel), California, and now Vancouver, with over $75 M in funds raised to increase the team to 400 employees.

Grammarly, which has developed an AI-powered digital writing tool, opened a new office in Gastown, which is the San Francisco-based tech company’s fourth global office location. According to a release issued last September, the company chose Vancouver “because of its strong and growing talent pool that supports and attracts both startups and established companies.”

Mastercard Inc. announced that it was investing $510 M to launch a new cybersecurity centre in the city and will hire approximately 300 workers.

In CBRE’s 2020 North American Tech Talent ranking, Vancouver remained at No. 12. Vancouver has benefited from tech-centric post-secondary schools such as the BC Institute of Technology and the University of British Columbia. Almost 12,000 tech degrees were added from 2014 to 2018.

CBRE has found that tech “submarkets” outperformed overall office markets within cities that are most popular amongst tech talent. One of the top-performing submarkets included Vancouver’s Broadway Corridor. However, vacancy rates in this area have ticked up in the last couple of quarters to 4.5%.

“Along the Broadway Corridor, neighbourhoods such as Mount Pleasant and False Creek Flats have evolved from industrial service submarkets to hubs for tech, animation, and creative industry firms,” the report also noted.

The number of tech jobs has grown by 47.9% in Vancouver between 2015 and 2019. So far, Amazon has accounted for 2,000 of those jobs, but it appears that number will go well beyond the 5,000 jobs that the company has said it intends to locate in Vancouver.

Amazon, which holds more than 600,000 SF of office space in downtown Vancouver has preleased 1.07 M SF of space being built at the Post project on West Georgia Street – the largest office leasing deal in Vancouver’s history. The company intends to allow its employees to work remotely until January of next year.

With major tech firms permitting their employees to work from home, there could be a shift in demand for office space by this sector. Facebook, for example, has said that half of its 50,000-person workforce will be working from home by 2030.

However, Facebook has said that it has no plans to close any offices as it allows employees to work remotely. Its Vice-President of Human Resources, Lori Goler, said in a statement that “offices will continue to play an important role in the future of work,” but that its shift to more remote work “is about supplementing offices, not replacing them.”

Vacancy rises only 30 bps in Q2 despite 2.1 M SF of new product as supply cannot keep up with demand.

Vancouver’s industrial vacancy remains one of the tightest in North America, with the vacancy rate rising slightly to 1.7% in Q2 2020, Altus Group reports. The averaging asking rents dropped by 2.5% to $14.29 PSF.

Q2 2020 saw 1.9 M SF of new industrial product coming to the market, with 72.4% preleased and another 1.9 M SF under construction.

A quarter of the new supply was Beedie’s 530,000 SF distribution centre that was completed on behalf of Sobey’s in Campbell Heights in South Surrey.

Campbell Heights is emerging as the most active development node in GVA’s supply-constrained market.Campbell Heights is expected to grow to about 25 M SF when the 2,000-acre zone reaches its potential. It is where Walmart is building its 300,000 SF, $175 M warehouse and distribution centre. The facility is expected to open in early 2022 and will provide fresh and frozen food to 60 stores in British Columbia with a focus on sustainability and no waste.

“Vancouver’s robust industrial pipeline is unlikely to have asignificant impact on vacancy, with the majority of space being build-to-suit or preleased,” JLL stated.

Just over 2.5 M SF of the 4.1 M SF currently under construction is expected to be delivered by the end of 2020, of which 64.1% has been pre-committed.

Even before the pandemic, Vancouver’s industrial demand was being driven in large part by last-mile logistics. Online retailers like Amazon, Ikea, and Walmart bought or built about 2.4 M SF of industrial warehouse space across Metro Vancouver in 2019, according to Avison Young.

Growth in e-commerce has skyrocketed since the start of the pandemic. Statistics Canada says e-commerce sales hit a record of $3.9 B in May, a 2.3% increase over April and 99.3% increase over February. Compared to May 2019, e-commerce sales more than doubled, increasing by 110.8%.

“Across all the logistics markets, it’s pedal to the metal in response to the momentous increase in online demand to delivering products to an at-home workforce,” Craig Meyer, President of Industrial Brokerage for JLL Americas says. “By the end of the year, there will be significant demand for leasing in the large e-commerce category of industrial buildings.”

“The intensification of e-commerce and logistics services will continue to spur demand for industrial space even further. Consumer expectations for same-day or next-day goods are likely to keep growing, and the lack of well-positioned industrial space is placing a significant strain on various retailers and e-commerce giants that depend on a network of distribution centres.” – Altus Group.

Pandemic-induced uncertainty has slowed investment activity in the GVA.

The second quarter of 2020 has offered the first bit of insight into the effects of the COVID-19 global pandemic on the Vancouver commercial real estate market. Facing the brunt of the pandemic, the first half of 2020 recorded a total investment volume of $3.7 billion, marking a nearly 30% decrease from the first half of 2019. Share sales, totalling only $500 million, accounted for the majority of the decline from the first half of 2019, falling 71% while asset sales of $3.2 billion fell by just 7% from H1 2019, Altus Group reports.

Morguard Investments sold the Viking Way Business Centre in Richmond to PC Urban and KingSett Capital for $49.2 M. The multi-tenant industrial building is approximately 160,000 SF.

KingSett Capital sold a 279,900 SF trucking terminal located in Burnaby for $51 M to a private investor.

The Jim Pattison Group acquired 997 and 1001 Coutts Way in Abbotsford for $17.2 M. Altus Group reports that the sale excluded one of the strata units at 997 Coutts Way.

Beedie Group bought 3195 Production Way for $15 M. The Burnaby industrial building was 17,090 SF situated on 2.37 acres of land.

Beedie Group also acquired a Surrey industrial building from Greiner Pacaud Management for $23.8 M. The 66,328 SF building sits on 11.7 acres of land.

In Q1, Larco Investments acquired a 250,000 SF industrial complex for $146 M. The multi-tenant building is located in Burnaby on Lougheed Highway.

Also in the first quarter, Larco Investments bought the Fontainebleau Apartments for $70 M. The Vancouver high-rise apartment on Balsam Street has 87 units. The site has an additional 100,000 SF of additional building space, according to Altus Group.

Mayfair Properties bought 1230 Nelson Street, a 107-unit high rise apartment building for $51 M.

Starlight Investments bought 1371 Harwood Street, a downtown high rise apartment building with 35 units for $16.4 M.

In April, Allied Properties REIT acquired The Landing, a 175,000 SF office building at 375 Water Street for $225 M. The 115-year- old building located in Gastown was bought from the owner of the Whitecaps FC, who had once proposed to build a soccer stadium on the site.

GWL sold Crestwood Corporate Centre and Commerce Court III and IV to a local private investor. GWL also sold a Class A office building in south Burnaby fully occupied by Ritchie BrosAuctioneers on a long-term lease for $75 M and a yield over 6 %, Colliers reports.

The St. Paul’s Hospital site on Burrard Street was sold to Concord Pacific Group for about $1 B. The deal closed at the end of July. A mixed commercial-residential development is being proposed for the 6.6-acre site.

Altus Group’s Q2 2020 Investment Trends Survey reveals that overall cap rates have gone up from Q1 to 5.15%. The company reports that Vancouver had one of the highest increases among the major Canadian markets.

Cap rates for industrial product increased by about 10 bps in Q2 from the previous quarter, and asset pricing fell by 5 to 10% PSF, JLL reports. Retail cap rates were up across the board, however, grocery-anchored assets remain in high demand among investors, according to the company.

On a national level, CBRE reports that defensive asset classes have exhibited lower levels of cash flow volatility than initially anticipated and suggested that ‘cautious optimism’ had returned to the market in Q2.

High unemployment and slow population growth will hamper demand for housing.

The Real Estate Board of Greater Vancouver (REBGV) reports that sales of detached, attached and apartment homes reached 3,128 in July 2020, a 22.3% increase from the 2,557 sales recorded in July 2019, and a 28% increase from the 2,443 homes sold in June 2020.

“We’re seeing the results today of pent up activity, from both home buyers and sellers, that had been accumulating in our market throughout the year. Low interest rates and limited overall supply are also increasing competition across our market,” Colette Gerber, REBGV Chair said.

In addition to the GVA, increased resales activity was evident across the province in July.

“The strong recovery in sales activity continued in July,” said BCREA Chief Economist Brendon Ogmundson. “Increased demand for more living space combined with an undersupplied market is producing significant upward pressure on home prices, particularly in the market for single-family homes.”

However, Altus Group reports that new condo sales were down 15% from 2019 in the first half of 2020, even with strong sales at the start of the year and a spike in activity in June. The company reports that new condo prices have dropped by 3%.

In 2019, the GVA recorded a record-breaking 28,141 housing unit starts according to CMHC. This number surpassed the previous record of 27,914 in 2016.

CMHC expects that in 2020, starts will drop significantly in Canada’s major centres. Central 1 estimates that the number of starts in BC will drop by 33%. Lower condo presales in the past year added to the shock of the pandemic, two of the main causes of the decline.

In their most recent Market Rental Report, CMHC reported that vacancy rates in Vancouver remained at 1.1% for purpose-built apartments and were 0.3% for condominium rentals. At $1771, the average asking rent for vacant units was 20.8% higher than the average rent paid for occupied units, at $1,466 in October 2019.

Demand for rental housing was primarily driven by employment growth and migration, but the pandemic has put the brakes on these drivers.

A study by Finder revealed that 1.5 million Canadians had moved back in with their parents since the COVID-19 pandemic began.

At the end of 2019, there were 144,675 study permit holders in the province, and the rate of growth was 8% per year over the past decade. International students may choose to delay entry or return to Canada, especially given the shift to online learning at colleges and universities this fall, Central 1 states.

This will have an important effect on the demand for rental housing.

In fact, asking rental rates in Vancouver have been falling for the last few months. Padmapper is reporting that rental rates dropped 0.5% to $2,060 in July, while two-bedrooms dropped 2.4% to $2,800. On a year-over-year basis, one and two-bedroom prices have fallen 6.4% and 9.4%, respectively.

The ban on evictions will be lifted beginning in September 2020, and tenants will have until July 2021 to pay back any missed rent from March through July 2020. A study by Landlord BC found that 85% of renters are making full payments, 12% are making partial payments, and only 3% have stopped making payments altogether.

The status quo will stunt supply and lead to further affordability problems, developers assert.

Developers at an Urban Development Institute event at the beginning of the year warned that demand-side policies as well as lack of collaboration between governments and the development industry would negatively affect growth, supply and affordability.

Brian Porter, CEO of Scotiabank, similarly said in January: “The federal, municipal and provincial levels of government need to be more coordinated in their approach.”

A report by Central 1 states that home sales dropped 40% between 2018 and midway through 2019 as stricter policies deter potential buyers while sellers wait for prices to come back.

“We’ve had the foreign buyer tax expanded geographically and made even stricter, we have the speculation tax, we’ve also had the mansion tax,” Tom Davidoff, an Assistant Professor at the University of British Columbia’s Sauder School of Business, said. This is in addition to the mortgage stress test and stepped up school taxes.

Other industry experts say that the combination of all of these taxes has impacted home sales and, ultimately, housing supply. Lower presale numbers affect construction financing. Financing will fall through if a project doesn’t get enough presales and the development becomes jeopardized.

“Unless [developers are] in a position to self-finance a project, where they don’t need the banks, they’re giving long, hard thought to how they proceed,” Coquitlam City Councillor Dennis Marsden said.

In Burke Mountain, located in northeast Coquitlam, the city started selling off serviced, pre-zoned sites through public tender to developers. For developers, the streamlined process of acquiring pre-zoned enabled them to begin construction within a year.

“So, developers can come in with their development application, and sometimes they are under construction within a year or so. It moves quickly,” says Curtis Scott, Manager, Land Development, City of Coquitlam.

Changes to rent control were made in September 2018 by the BC government. Rent increases cannot exceed the rate of inflation, rather than the previous calculation of inflation plus two percent.

Joshua Gottlieb, Associate Professor at the Vancouver School of Economics, UBC, predicts that the province’s new limitation of allowable rent increases to the cost of inflation “will do the opposite: discourage construction, which reduces competition. Renters will suffer – via low quality instead of prices.”

In June 2019, the City of Vancouver approved several amendments to the Tenant Relocation and Protection Policy. The most significant of the changes is the increased compensation levels for renters forced to relocate due to renovations.

The existing right of first refusal at 20% below new market rents for tenants returning to redeveloped sites will be maintained. Substantial financial challenges exist for housing providers and developers if this rate is any lower.

The new rules require landlords to provide more help for displaced tenants looking for new homes at a manageable price and increase the level of communication between tenants and the redevelopment team.

Landlord CB CEO David Hutniak warns not to discourage landlords from investing in the ageing rental stock and increasing the numberof units through redevelopment.

CMHC announced changes to the eligibility rules for mortgage insurance, which came into effect on July 1. The new rules will reduce the amount of debt an applicant for an insured mortgage can carry, set a higher credit score of 680 to qualify for CMHC insurance, and will require a homebuyer to use their own, not borrowed, funds for down payments.

The changes made in response to the pandemic are designed to “protect future home buyers and reduce risk.” CMHC is predicting a drop in average housing prices of between 9% and 18% over the next 12 months.

CMHC provided 100,000 insured mortgages in 2019, about half as many compared to 2017. Borrowers are increasingly seeking private funding, which is not subject to the same borrowing restrictions.

Brad Jones, Vice-president of Development at Wesgroup, has said that they have been able to take advantage of government incentives, including CMHC’s Rental Construction Financing Initiative, to build rental in their master-planned River District. However, he tells RENX that “there is still a quagmire of bureaucracy involving conflicting policies between different government departments. It’s part of the reason a massive project like River District takes so long.”

Altus Group reported that at the end of 2019, almost 75% of Vancouver rental development applications submitted in 2017 were still under review by the city.

Despite a fundamental shift away from traditional retail uses, Vancouver has one of the lowest vacancy rates of Canada’s major cities.

Population growth, tourism and job growth, all factors that propel retail spending, evaporated in March. Not surprisingly, vacancy has increased over the last two quarters. Cushman & Wakefield has reported an increase in vacancy to 4.1% in Q2 2020 from 3.4% in Q4 2019.

Fewer restaurants and shops have closed than the company had initially projected, and it is anticipated that many of the restaurant spaces that did become vacant will be reabsorbed quickly. In early July, it 78% of consumers reported that COVID made them more aware of the importance of small businesses in their communities and will likely support them more in the future.

As many as 25,000 stores are expected to close in the US in 2020, mostly in shopping malls, Coresight Research predicted in June.

For Canada, that could theoretically mean 2,500 stores, said Craig Patterson, of Retail-Insider.com.

Market intelligence company, Trendex, says that total retail apparel sales will decrease by 28% to 32% in 2020, while luxury apparel sales should drop 16.8%. It expects 10 to 15 major apparel chains will either close or drastically reduce their retail footprint.

Vancouver based chains Lululemon and Aritzia are continuing to perform well, but other chains such as Frank and Oak and Sail are filing for bankruptcy protection. Roots did not pay its April rents and expects its retail footprint to decrease over time.

Throughout the pandemic, grocery-anchored assets have performed well and continued to be the most sought-after assets among retail investors.

At the beginning of the year, nearly four million square feet of new retail development is being built or planned in Metro Vancouver, including a 150,000 SF addition to the McArthurGlen Designer Outlet mall in Richmond and an 80,000 SF shopping mall being under the Vancouver House condo tower at the north end of the Granville Street bridge.

With property tax assessments based on Highest and Best Use, many retail property owners are tearing down existing structures and planning to redevelop under higher density allowances. JLL reported that demolitions peaked in 2019, and more landlords are including demolition clauses in leasing agreements.

Altus states that “investors continue to focus on transforming older retail properties into mixed-use communities, catering to changing demographics and customer demands by combining features of retail, entertainment, office and residential uses into a single location. Many of these properties are in well-located areas near major road networks and transit nodes, making them ideal properties for successful intensification.”

An example of this transformation trend is QuadReal and Westbank’s redevelopment of the 30-acre Oakridge Centre. When complete, the centre will include 2,548 homes, including 1,968 market housing units, 290 social housing units, and 290 rental housing units. In addition to one million SF of flexible retail space, there will be a 100,000 SF community centre, a library, daycare and senior facilities.

Statistic Canada numbers published in mid-July indicate that retail sales recovered to $41.8 B in May—a $6.6 B increase over April’s level (a rise of 18.6 percent).

In addition, preliminary estimates suggest that retail sales rose by 24.5% in June. If this increase holds, retail sales would be almost completely recovered in June when compared to February.

Conference Board analysis concludes that the Canada Emergency Response Benefit (CERB) has been an income boost to many households and is likely a big reason why retail sales have recovered ahead of other parts of the economy. Government programs have propped up much of the spending power in the economy.

“Retail sales are strongly rebounding, boosted by pent-up demand and as government income support measures provide a lift to household spending,” Bank of Montreal Economist Benjamin Reitzes said. “While it looks as though retail activity returned close to pre-COVID levels in June, expect the broader economy to experience a longer, more drawn-out recovery as the pandemic continues to weigh on many sectors.”

The pandemic is forcing the real estate industry to fast track its digital transformation.

Global investment in the PropTech sector has hit staggering levels totalling US $31.6 B in 2019, according to CREtech – a 227% increase from 2018.

The pandemic has caused deals to slow and investors to become more cautious.

A new survey from venture capital firm MetaProp, which received responses from more than 2,500 PropTech executives and investors, found a significant drop in their confidence in the market. However, 33% of investors are expected to make more investments into PropTech over the next 12 months compared to the previous 12 month period.

MetaProp’s survey found that 84% of PropTech start-up founders believe the coronavirus is accelerating the adoption of technology in the real estate industry.

As workers return to their offices, landlords are implementing technology to enable touchless solutions, monitor common area occupancy and air control and to better communicate with their tenants.

A new report by independent European venture capital (VC) fund PropTech1 Ventures found that agile start-ups and those that address rapidly changing requirements and expectations induced by COVID-19 will prosper, emphasizing start-ups with technical solutions that reduce the risk of infection in office and retail space.

German start-up Thing Technologies (Thing-it), for example, has developed a new digital solution called Virus Guard that helps reduce the risk of infection by using sensors to control the flow of people in a store or building.

Toronto-based PropTech firm Lane has just raised an additional $10 M in a funding round led by Round13 Capital, with further participation from Alate and Panache.

Lane offers a platform that streamlines office and retail space communications between landlords, property managers, companies, retailers, and vendors.

The platform enables contactless elevator and building access control using QR codes that can be scanned from more than two metres away.

Lane can also help retailers manage the flow of shoppers into their stores by allowing users to book specific time windows.

The startup closed out 2019 with over 300 M SF contracted through its platform, representing a 320% year over year increase. Lane’s clients include Colliers, Brookfield Properties, Hullmark, Menkes, Dream and Kipling.

The company also stated that on average, landlords report a 20-fold increase in engagement and usage of building services and amenities since using Lane’s platform.

Since the onset of the pandemic, Lane’s CEO and Co-founder Clinton Robinson believes there will be even greater demand for a technology solution that can “help property owners and operators orchestrate a safe and secure return to work, effectively manage building communications and operations, and make the workplace a seamless and engaging place to be.”

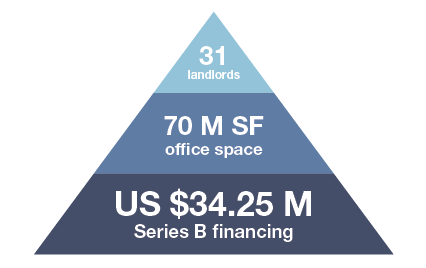

HqO, a Boston-based tenant experience (TeX) platform for commercial real estate, has just raised US $34.25 M in Series B financing led by Insight Partners. It’s currently working with 31 landlords, including Blackstone’s EQ Office, and manages 70 M SF of office space. It has seen demand for its platform accelerate in May and June.

HqO’s software gives office landlords a way to unify all of an office building’s tenant-facing technology and amenities into a single SaaS platform. The platform also features content and events, and provides landlords with data aimed at helping them increase tenant retention.

In response to the pandemic, HqO announced a new partnership with LiveSafe, a risk intelligence and safety communication platform.

“Now more than ever, the use of technology to ensure safety and communication in the workplace is paramount,” HqO Co-founder and CEO Chase Garbarino said in a release.

Millions of square feet are either planned or under construction in the GVA.

Despite the pandemic, high land costs and government policies that are often an impediment to development, 6 M SF of office space is under construction, as well as 4.4 MSF of industrial space and thousands of new homes are in the pipeline for Vancouver.

UK property investor Grosvenor has stepped up development efforts in GVA. It has just acquired the final piece for its Burnaby land assembly in Brentwood, where it plans to create a mixed-use development that could have over 2,000 residential units, including condominiums and rental housing, with approximately 500,000 SF of commercial space.

Cadillac Fairview has just submitted revised plans for The Crystal at Waterfront Square at 555 West Cordova in Gastown. The new plans call for a 26-storey office building of about 500,000 SF. The building will be constructed targeting WELL and LEED Platinum certifications.

Squamish Nation development is an 11.7-acre Squamish Nation-owned site at the foot of Burrard Bridge near Vanier Park. The project will feature about 6,000 units of mostly rentals in 11 towers. Squamish Nation has partnered with developer Westbank, and construction for phase one could start in 2021.

Henson Development is proposing a 60-storey residential tower in the city’s west end, Nelson Street Tower, which is being built to passive house standards. It will feature a total of 485 units, including 113 social housing units, 49 market rentals and 323 market condo units.

Construction on the first phase of Onni Group’s Gilmore Place in Burnaby has begun. The first phase of the development will be home to three towers, the largest measuring 64 storeys – taller than any other residential tower west of Ontario.

The remaining two towers are 43 and 51 storeys, totalling 1,550 units across all three buildings. A podium on the sixth floor will connect the three towers, which will contain 500,000 SF of retail space and 1 M SF of office space.

Future phases of the Gilmore Place project, which is situated on a 12-acre site surrounding Gilmore SkyTrain station, will eventually see a total of ten towers.

Canadian Metropolitan Properties’ plans to redevelop the North East False Creek Plaza of Nations site at 750 Pacific Boulevard, which was heading to the development permit board at the time of writing. The project includes terraced buildings up to 30 storeys with commercial space on the lower floors.

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.