Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the performance of Land and Developement Conference, click the following Insights.

Tight supply, capital availability & low unemployment will underpin continued demand for real estate.

Conference Board of Canada projects that the Canadian economy will grow by 2% in 2019 but fall below 2% beginning in 2020.

The economy has been driven by robust household spending in recent years. This has been spurred in part by high home prices and a large increase in consumer debt.

The outlook for housing demand in 2019 remains positive across the country with elevated immigration levels, continued demand from first-time home buyers, and a tight rental market, asserts Altus Group.

CMHC numbers show that five of Canada’s ten largest cities (Vancouver, Toronto, Ottawa, Montréal and Halifax) have overall apartment vacancy rates below 2.0%.

Housing demand is expected to remain rob ust in 2019, CMHC concurs. Although both consumers and developers will continue to be impacted by rising interest rates and increasing construction costs.

The key pressures that we see continuing to impact the new home market in 2019 are higher interest rates and housing affordability constraints, rising construction costs and development charges impacting developers, and weaker economic growth potential in certain regions constraining demand, Altus reports in its New Home Outlook - 2019.

The commercial markets are expected to stay strong, with low vacancies and rising rents supporting new development, although higher interest rates and slowing economic growth – both in Canada and globally – could impact demand and new development activity, CMHC continues.

Hotel occupancy reached 66.0% nationally in 2018, setting a new Canadian record.

Commercial real estate investment almost reached $55.0 Billion in 2018 with residential land, apartments, and industrial marked as the top three asset classes, Altus Group reported.

Strong demand, record low vacancy rates and changing tenant needs are spurring a wave of new construction across the country.

Currently, as of Q1 2019 about 19.2 M sq. ft. of office and 25.2 M sq. ft. of industrial product is under construction— primarily concentrated in the tight Toronto and Vancouver markets, Altus Group notes.

“We continue to feel very positive about opportunities in the real estate environment for the year ahead,” said Avison Young’s Chief Executive Officer, Mark Rose, in a report at the beginning of the year. “More capital is available to move into real estate debt and equity than at any other time. The next wave of investment is not a matter of if or when— it’s just a matter of price.”

New construction technology is addressing the productivity lag in the sector.

Tech investment in construction has grown rapidly in the past decade. In 2008, global investment totalled $4.5 M across two deals, according to data from CB Insights. The industry saw $882.3 M in investment in 2017 across 103 deals and by midway through 2018, $1.38 B had been invested across 61 deals.

From 2011 through 2016, construction-technology players received the greatest amount of investment (from venture capital and other sources) for document-management use cases ($1.7 B), followed by equipment management ($1.4 B) and enterprise-resource-planning systems. McKinsey found that new start-ups focused on performance management and field productivity, with 29% of companies developing tools for one or both areas.

According to a report by McKinsey, global labour-productivity growth in construction has averaged about 1% annually over the past two decades, compared with 3% to 4% across other sectors. By closing this gap with new tools and solution, the industry’s output would increase by $1.6 T per year.

In January 2018, the startup Katerra brought in $865 M from Softbank, RiverPark Ventures, and Four Score Capital in a Series D round— more than the whole sector raised in 2013 and 2017 combined. The startup optimizes “every aspect of building development, design, and construction.” It has raised $1.1 B since its inception in 2015.

San Francisco-based Rhumbix has raised more than $20 M to develop its mobile platform designed for the construction workforce. It brought in $7.4 M in a Series A round last September.

Rhumbix has developed a tool for digitizing field data on project sites. It tracks timekeeping, production, and T&M tags via a smartphone app that eliminates the need to use paper and spreadsheets in the field. Foremen save 2.5 to 3 hours per week on paperwork when using the Rhumbix system, the company estimates, according to feedback received from customers.

San Francisco-based PlanGrid markets a cloud-based productivity software that aims to help owners, general contractors, and subcontractors collaborate on blueprints and building documents from any device. It raised a $50 M Series B round last September and has brought in $69 M in total since it was founded in 2011.

WiredScore, a New York-based real estate tech firm that certifies office buildings for internet connectivity, has raised $9 million in Series A funding.

The funding was secured from Bessemer Venture Partners, Los Angelesbased Fifth Wall, Sterling and commercial real estate investors including Legal & General, KingSett Capital, U+I, Town Centre Securities, Momeni Digital Ventures and Savitt Partners.

“WiredScore’s engineers have developed these guidelines as a free resource that will bring technology to the forefront of the design process,” said WiredScore Founder and CEO Arie Barendrecht. “Technology has never been more important to office tenants than it is today, and by providing invaluable insights into how to optimally design for reliable connectivity, mobile enhancement planning, electrical resiliency and flexibility to adopt new building technologies, we are helping Canadian developers design future-proofed office assets.”

75 office assets developed by Fourteen Canadian property owners and developers have either become Wired Certified or are undergoing the certification process in Toronto, Montreal and Vancouver. Notable developments include Ivanhoé Cambridge and Manulife’s Maison Manuvie and Broccolini’s 700 Saint-Jacques St. in Montréal; Menkes Development’s One York St. and Caterra’s 65 King East in Toronto; and GWL Realty Advisors’ Vancouver Centre II in Vancouver

An estimated 1.6 M Canadian households are considered in “core housing need,” meaning that people live in places that are too expensive or unsuitable.

In November 2017, the federal government unveiled its 10-year, $40 B National Housing Strategy (NHS) which is being administered by CMHC.

In addition to the NHS, CMHC has made it a priority to provide every Canadian with affordable housing that meets their needs by 2030.

To achieve this goal, CHMC plans to give out $2.4 B in loans and funding as part of the strategy to build 8,300 units, including 3,800 rental units, and repair 15,000 more over the next year.

Municipalities across Canada have begun to unveil their latest initiatives aimed at boosting local affordable housing supplies.

In Toronto, Mayor John Tory’s “Housing Now” plan is already underway with support from the federal and provincial governments. Eleven surplus city-owned land sites near transit stations are about to be transformed into affordable housing developments. The goal is to add 40,000 affordable units in the next 12 years and realize 3,300 or more affordable units per year, beginning in 2020.

As part of its Housing Vancouver strategy, the city has implemented the Moderate Income Rental Pilot Program as well as Rental 100 strategies to help it reach its goal of creating 20,000 new units of market rental housing by 2027.

The Moderate Income Rental Housing Pilot Program encourages development proposals for new buildings where:

- 100% of the residential floor area is secured rental housing

- At least 20% of the residential floor area is made available to moderateincome households earning $30,000 to $80,000 per year

The pilot program will select up to 20 proposals for submission of rezoning applications between January 1, 2018 and July 1, 2019. Developer incentives include increased density, development charge waivers and expedited processing.

Rental 100 encourages projects where 100% of the residential rental housing units are secured for 60 years or life of the building, whichever is greater. Similar incentives are provided and also include the relaxation of unit size to 320 sq. ft. (provided the design and location meet the City’s liveability criteria).

The theory is that more market rental housing gives higher-earning residents more options to choose from, lowering the pressure on demand for lower priced rental units.

In Coquitlam alone, three new non-market rental projects are about to break ground, with help from provincial funds and money from the City’s affordable housing reserve and incentives, such as reduced parking and higher density.

- The Concert Properties will get $10 M in provincial funding for their 551 Emerson Street development. The rental project will see the construction of 100 affordable units in a 200-unit tower, with rents tied to income for seniors, families and people with disabilities. The remaining units will be rented at market rates.

- At 2905 Glen Dr., the Community Land Trust, the real estate arm of the Co-operative Housing Federation of B.C., will receive $13.1 M to build 131 units for families at the site of the Hoy Creek Housing Co-op.

- At 3100 Ozada Ave., the Affordable Housing Societies has received $7 M to build 70 units of affordable housing in an apartment building on the side of the site, which has a number of rental townhomes on the property.

Coquitlam has 4,000 purpose-built rental units in the works, approximately a quarter of which are earmarked as non-market rental.

Action Ottawa is the City’s primary program for increasing the supply of low-income affordable housing in Ottawa. Action Ottawa combines City incentives with funding from all three levels of government to help private and non-profit developers build new affordable rental housing for moderate and low-income households.

Ottawa Community Housing acquired 933 Gladstone Avenue along the O-Train corridor. The 7.3-acre vacant site was bought from the Canada Lands Corp. for $7 M in May 2017. The OCH is planning a mixed-income community for the “Gladstone Village” made up of subsidized housing and market-value housing. The City of Ottawa Zoning By-Law classifies the property as a Mixed-Use Centre Zone (MC), which regulates the use of land and buildings through height and density, parking and loading spaces, and setbacks form the street.

Edmonton is tackling the affordability issue by launching a ‘missing middle’ infill design competition.

The term ‘missing middle’ refers to multi-unit housing that falls between single detached homes and tall apartment buildings. It includes row housing, triplexes/fourplexes, courtyard housing and walk-up apartments.

The City states that encouraging this type of housing is essential for welcoming new people and homes into older neighbourhoods and creating complete communities with a variety of housing options for people at every stage of life and income level.

The City is soliciting proposals to design a multi-unit, medium-density, or ‘missing middle’, housing development on five City of Edmonton owned parcels of land at the northeast corner of 112 Avenue and 106 Street in the Spruce Avenue neighbourhood. The winning team will be given the opportunity to purchase the site and build their winning design. To

Cities, communities and buildings need to build the infrastructure to enable them to adapt to changing environments.

As technology changes the way people live and work, cities are undergoing an unprecedented transformation. Those that have the infrastructure and strategy to manage this rapid technological shift are set to become the most competitive.

Key elements of future-proofing include: the ability to drive and manage technological change; infrastructure that contributes to a high quality of life; a long-term city vision; and attracting and retaining talent, JLL Research Director Jeremy Kelly writes.

In total, cities around the world are expected to spend around $41 trillion on smart-city upgrades over the next 20 years, according to EY.

A smart city is defined as one that uses data and technology to enhance operational efficiency and deliver sustainable solutions to enable economic growth and enhance the quality of life for its community.

Lack of infrastructure is one of the barriers that prevent cities from becoming smarter.

According to the Globe and Mail, Sidewalk Labs is shopping around for investment partners to help finance next-generation infrastructure to underpin their Quayside development.

Toronto-based architectural firm, Quadrangle, states that there are four main ways to future proof buildings:

- Understand local climate change risks and adaptability strategies;

- Demand that passive design solutions to reduce thermal demand, mitigate flood and anticipate power outages be prioritized;

- Request the use of climate future scenarios during the design process for new building design and test future weather scenarios in existing assets;

- Prioritize designs that support social connection and ambitious change.

On the topic of future proofing new developments, Jay Wyper, SVP at the Hines Conceptual Construction Group, said that in his experience working in Europe and North America, suburban developments are increasingly urban in nature, with densification and a mix of uses providing places where people can work, live, and play.

He added that housing is also often now aimed at multiple generations. Also, there has been a move away from concentrating simply on buildings’ environmental sustainability to the role they play in promoting wellness.

Affordable housing is crucial to future-proofing our communities. Worldwide, the McKinsey Global Institute has estimated that some 330 million urban households currently live in substandard housing or stretch to pay housing costs that exceed 30% of their incomes.

Lack of affordable housing constitutes a significant risk for cities and needs to be addressed to make them more resilient to increasing migration flows. Income polarization can be exacerbated if lower-income households cannot find a decent place to live.

McKinsey estimates that autonomous vehicles could reduce the need for parking space in the U.S. by more than 61 B sq. ft. This would have a significant impact on commercial real estate by supplying development opportunities on the sites of existing parking lots and garages and also by reducing the costs associated with incorporating parking in a new development.

“AVs remove commuters’ demands for street and lot parking,” KPMG said in its autonomous vehicles report. Driverless cars could potentially pick people up from their homes, drop them off at the office or the mall and then leave to park in a less prime area— or, like taxis, won’t even need to park, but will just move on to the next customer and the next trip.

In addition, automated cars could directly affect the design of homes. According to Robert Dietz, chief economist and senior vice president for Economics and Housing Policy for the National Association of Homebuilders, it would mean additional interior space within homes and less space dedicated to car storage.

Tariffs and labour shortages among trades are putting upward pressure on construction costs.

Real estate projects across Canada totalled $210 B in construction costs last year, led by $87 B in 1,550 residential projects. Approximately 210,000 new homes are expected for 2019, with an additional $85 B in residential renovations projects in the pipeline.

Construction cost increases are projected to average 6% to 8% in 2019, according to BTY Group’s annual Market Intelligence Report.

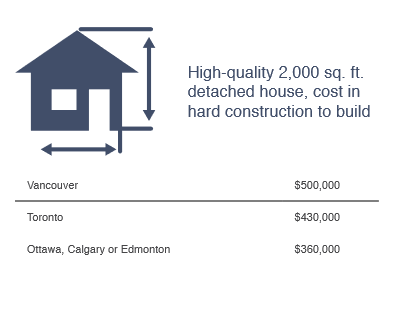

A high-quality 2,000 sq. ft. detached house would cost up to $500,000 in hard construction costs to build in Vancouver. In Toronto, this house would cost $430,000 and in Ottawa, Calgary or Edmonton, the cost would run around $360,000, according to the Altus Group’s Canadian Construction Cost Guide 2019.

According to Altus, commercial costs are also highest in Vancouver. The hard construction cost for a Class A, 5 to 30 storey office building in Vancouver ranges from $240 to $305 per sq. ft. This compares with $215 to $285 per sq. ft. in Calgary and $215 to $295 per sq. ft. in Edmonton. The price for such an office building in Toronto ranges from $220 to $290 per sq. ft.

Construction costs have jumped 23.6% since 2004 in the U.S., according to “What’s Up With Construction Costs?”, a report by BuildZoom economist Issi Romem. The housing cost spike that started in the mid-2000s at the tail end of the pre-recession building boom was initially caused by increases in material costs; the continued rise is now mostly a factor of rising labour costs.

Romem notes that the key drivers of construction costs are still “lots and local regulations,” the combination of high land prices and restrictive landuse policy. However, in especially expensive metros, labour costs have also vastly accelerated the cost of construction.

A skilled labour shortage in Ontario in the past three years has slowed the growth of construction companies, prompting some to turn down work and others to decline to bid on projects, according to the 2019 Contractor Survey by the Ontario Construction Secretariat. The shortages led to significant increases in project costs for 59% of respondents.

Labour shortages are expected to worsen. In the next 10 years, about 91,000 construction workers are expected to retire, 40,000 of whom are in the GTA, says Katherine Jacobs, director of research at the Secretariat.

The tariffs imposed by Trump and the countermeasures they have triggered around the world are pushing up material costs for the Canadian construction industry, said Sal Guatieri, senior economist at BMO Capital Markets.

Canada is a net importer of rebar— the steel used to reinforce concrete in condo towers— which is subject to the counter-tariffs, said David Schoonjans, senior director of cost consulting and project management at Altus Group. He estimates that rebar makes up around 4% of the cost of a condo tower, meaning a 25% import duty would add up to 1% in construction costs.

In Ontario, the increased cost of steel could add between $10,000 and $12,000 to the cost of an average condominium unit and boost the price of new condos in Vancouver by up to $10,000 per unit, according to the Residential Construction Council of Ontario.

The country’s geography deters West Coast buyers from purchasing steel from central Canada. It costs more than four times extra to ship a tonne of steel to Vancouver from Ontario than it does from China or Korea, said Richard Lyall, president of the Residential Construction Council of Ontario.

CREA reports that the Canadian housing market is headed for the weakest year in a decade.

CREA expects home sales in Canada to decrease by 1.6% to 450,400 in 2019, a change that would mark the weakest annual sales since 2010. The association expected British Columbia and Alberta to account for much of that projected decrease.

The national average price for homes sold in February was $468,350, down 5.2% from the same month in 2018. If you factor out the GVA and GTA markets, the national average price was just under $371,000.

CMHC forecasts that housing starts will slow down gradually into 2020, coming down from the 10-year high recorded in 2017 to levels more in line with a moderate economic outlook.

Single-detached housing starts are anticipated to decrease over the forecast horizon due to limited lot availability in some of Canada’s major CMAs, and higher borrowing costs across the nation.

Multi-unit housing starts are expected to trend down despite inventory levels that are at their lowest levels since Q2 2008.

“While new condominium apartments continue to provide a more affordable alternative to new single-family homes, the gap in prices between new single-family homes and new condominium apartments has narrowed significantly since early 2017, removing some of this advantage,” according to Altus Group’s GTA Flash Report 2019.

“With available inventory low in relation to the pace of sales, the average asking price for a new condominium apartment in the GTA rose by 57% in the past two years with the benchmark price reaching an all-time high at just under $800,000 by the end of 2018,” Altus Group reports.

Homebuilders sold 25,161 new homes across the GTA last year, down 40% from 2017 levels.

The majority of sales remained in the condo market, with 21,330 according to the report. About two-thirds of those sales were within the City of Toronto.

Single-family homes decreased from over 20,000 units in 2015 to 3,831 in 2018.

In December the benchmark price of single-family homes, including detached, linked and semi-detached homes as well as townhouses, was $1,143,505, down 7% from a year ago and 13% off the July 2017 peak.

Canada’s mortgage stress test which requires borrowers to prove they can handle a 2% increase on their approved interest rate, has been blamed by realtors, developers and investors for driving down sales.

According to a new report from The Canadian Home Builders’ Association (CHBA), nine out of 10 builders say customers had a harder time qualifying for a mortgage last year than in 2017.

The report also notes that 84% of builders had home purchase agreements fall through as a result of financing issues last year. As a result of the financing issues, CHBA found a 33% drop in sales to first-time homebuyers.

TREB estimates that the stress test requires homebuyers to prove they can handle an additional $700 in monthly mortgage payments requiring buyers to move to more affordable housing options.

In the Greater Vancouver area, the total number of homes sold last year fell to 24,619, marking the lowest total since 2000— down 31.6% from nearly 36,000 in 2017 and 25% below the region’s 10-year average.

The average price for a home in the GVA, which includes detached properties, townhomes and condominiums, dropped 2.7% from December 2017 to finish the year at $1,032,400.

REBGV president Phil Moore attributed the declines in B.C. to the same factors impacting home sales in the GTA. “High home prices, rising interest rates and new mortgage requirements and taxes all contributed to the market conditions we saw in 2018,’’ he said.

As home prices and borrowing costs increase, the demand for mid-rise housing is increasing.

According to Shaun Hildebrand, president of Urbanation, “the market is substantially undersupplied in mid-rise.” He reports that mid-rise projects in the GTA were just 31 of 2017’s new launches, accounting for 3,833 units or 12% of the total. The number of units per mid-rise launch has been growing too, from 80 a launch in the second half of 2016 to 145 a launch in the first half of 2018.

“At an average selling price of about $500,000, units in these types of projects are in extremely high demand, given that the cost to rent in today’s market would be just as high as the ownership carrying costs,” Mr. Hildebrand said.

Total net absorption nationwide totalled 2.7 M sq. ft. in Q4 2018, which was more than double the amount of new space delivered across the country according to CBRE.

According to CBRE, positive net absorption was recorded in nine of the 10 Canadian office markets.

Altus Group also reports a drop in vacancy in all major markets— with the exception of Manitoba— and on a national level is at its lowest point since the 2008 global financial crisis.

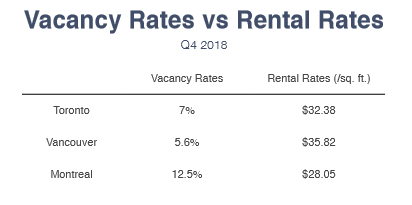

In Toronto, vacancy rates dropped to 7.0% in Q4 2018 while rents have increased to $32.38 per sq. ft. in the same period.

Vancouver’s rental rates were $35.82 per sq. ft., where the vacancy rate was 5.6%.

In Montreal, rental rates were $28.05 per sq. ft. and the vacancy rate was 12.5%.

Toronto had 11.3 M sq. ft. under construction in Q4 2018, while Vancouver had 3.72 M sq. ft. and Montreal had 2.76 M sq. ft. under construction, Altus Group reports.

Tech firms are experiencing unprecedented growth, and small, medium and even large tenants are demanding more flexible lease terms from landlords to manage the unpredictability of their requirements.

Tech companies continue to drive the leasing market across major Canadian markets and are reported to build out more amenities than other tenants, in order to attract and retain the best talent.

CBRE says the technology sector is a major contributor to increased rates of leasing for downtown office space in Toronto, accounting for 20% of pre-leased space out of the 9.1 M sq. ft. in new planned development.

In Vancouver, of the 3.72 M sq. ft. under construction downtown, 1.6 M sq. ft. has already been pre-leased. Large tech tenants expanding in Metro Vancouver have earmarked the majority of the preleased space, according to JLL, and Colliers reports that technology companies represent 34.4% of the leasing activity in the city.

The Montreal, Ottawa and Kitchener-Waterloo markets are also attracting tech companies as rental rates climb in the Toronto office market.

Shared workspaces have grown at an incredible rate of 200% over the past five years. In global cities like London, New York, and Chicago, they are expanding at an annual rate of 20%, making coworking an institutional part of the market despite many dismissing this trend as a fad.

Shared space accounted for 12.4% of the overall downtown office absorption in Toronto and Vancouver from 2015 to 2018. That demand is accelerating as occupier needs transform.

According to a 2017 study by Freelancers Union and Upwork, freelancers are expected to become the majority of the workforce by 2027. Five percent of Canada’s workforce will be “on demand” or “freelancing” by 2020 StatsCan forecasts.

Although the growth of freelancing or the gig economy fuels the demand for coworking space, more than 30% of WeWork’s members now work at companies with 1,000 or more employees, Bloomberg reports.

These factors together will enable continued growth for co-working. Spaces and Regus owner IWG announced it will open at least nine new locations across Canada in 2019. Combined, they will encompass about 375,000 sq. ft.

CBRE recently announced the 2019 launch of Hana, a new service offering designed to help institutional property owners meet the rapidly growing demand for flexible office space solutions.

Hana’s core offering is called Hana Team, combines the benefits of flexible space with the amenities, technology, thoughtful space design and control over branding and culture that corporations require.

CBRE will launch its first Hana unit at PwC Tower at Park District in Dallas, a new development project by MetLife Investment Management and Trammell Crow Company. The unit, called Hana PwC Tower at Park District, is expected to open in mid-2019.

Demand will exceed supply for the next few years as Canadian industrial markets are forecasted to have over 30 M sq. ft. of net absorption between 2019-2020 according to C&W.

Consumers research and learn all there is to know about the product before going into a physical location— if they ever do. One of the outcomes is that square footage demand for retail space has decreased due to shifts in consumer behaviour and buying patterns, efficiencies of the physical store and online channels, according to Forbes.

“...Increasingly, retail stores are being used as vehicles for product discovery, not pickup. At the same time, digital native retailers are moving into showroom-style spaces,” CBRE’s Paul Morassutti asserts.

Tesla might be the best example, Morassutti continues. “You do not drive off from a Tesla showroom with a Model 3, but you do leave with a deeply implanted memory and strong brand association.”

Global online sales were less than $1 T in 2011. By 2020, according to estimates from e-Marketer and Prologis Research, total sales could double again to $4 T, at which point they’ll account for nearly 15% of total sales. In Canada, it is estimated that retail e-commerce sales will total C$55.78 B by 2020.

Warehousing and distribution markets have experienced an increasing demand due to the yearly growth in online purchases.

Canada’s industrial availability rate remained stable in Q1 2019 from the previous quarter at 2.9%, the lowest rate ever recorded by Altus Group. Toronto, Vancouver and Montreal are seeing the lion’s share of demand, with availability rates of 1.5%, 1.9% and 4.3% respectively, Altus Group reports.

Toronto is now the tightest industrial market in North America, alongside Greater Los Angeles with Vancouver ranking third tightest market in North America.

Canada-wide average rates increased by 10.1% in 2018, the largest single-year increase in history while rental rates in the GTA grew by 17.6%. Vacancy

Access to the ”last mile” of delivery in urban locations has become one of the most critical factors in site selection and urban logistics is a fastgrowing industry that is anticipated to spend nearly $6 T by 2020.

In Chicago for example, the average city resident generates approximately 0.1 deliveries per day. With a population of 2.7 M, that equals 270,000 daily deliveries and the number of deliveries is only expected to grow and so will the need for staging areas close by to deliver goods.

Buildings and structures are being repurposed in response to the demand for fulfillment space. A portion of the Millennium Parking Garage in Chicago was transformed into a shipping/warehouse location. The garage’s 3.8 M sq. ft. over two floors had been under-utilized, so the owner worked with developers to repurpose some of it into an urban fulfillment center as well as self-storage.

Retailers and the 3PL firms that service them will continue to covet facilities within five to seven miles of major urban markets. In addition, C&W notes that demand will continue to increase for a variety of building types, including urban depots, sortation hubs and cold storage facilities.

Across the country, average rents for a 2-bedroom unit grew by 3.5% to an average of $1,025 while vacancy fell for the second year in a row to 2.4% in 2018.

CMHC reported that high levels of international migration, growth in youth employment and the aging of the Canadian population led to an increase in the number of occupied apartment units on the primary rental market.

Vacancy rates decreased in Quebec, Alberta and the Atlantic region and while still remaining very tight, they increased slightly in Ontario and British Columbia.

In Quebec, the rental market tightened considerably, as the vacancy rate dropped from 3.4% in 2017 to 2.3% in 2018. While significant, the increase in the supply of purpose-built rental apartments was offset by the strong rise in rental housing demand. This demand was supported in part by Quebec’s vigorous economy.

The vacancy rates also declined in Alberta (from 7.5% in 2017 to 5.5% in 2018) and in Saskatchewan (from 9.3% in 2017 to 8.7% in 2018).

In Ontario, the rental apartment vacancy rate stayed close to the all-time low recorded in 2017 of 1.6%, despite posting a modest increase in 2018, to 1.8%, on account of the greater number of purpose-built rental housing unit completions.

In British Columbia, the vacancy rate also remained low, although it did rise slightly, reaching 1.4% (versus 1.3% in 2017). Rental housing demand stayed robust this year, thanks to a growing preference for rental housing and sustained international migration, CMHC reported.

GWL has just broken ground on a 21-storey market rental tower at 1500 Robson Street in Vancouver. A third of the building will be made up of 2 and 3-bedroom units suitable for families. High-level indoor and outdoor amenities such as fitness, yoga and lounge rooms as well as a rooftop patio has been incorporated into the building’s design. The entire penthouse floor of the tower has been set aside as a common area for all tenants. The building will also be pet and cyclist friendly and is expected to be finished in early 2021.

Killam Apartment REIT is in the process of completing three apartment developments:

- Spring Park in Gloucester — when complete will total four residential towers containing up to 840 units. The first phase of the development will include a 217,000 sq. ft., 23-storey tower containing approximately 222 units.

- SilverSpear Phase II in Mississauga — the 128-unit building will feature 980 sq. ft. common amenity room and 1,430 sq. ft. fitness room and have a geothermal heating and cooling system.

- CarletonTerrace in Halifax — the 104-unit 18-storey building’s proposed features with include a large common amenity room and a two-level fitness room.

Devimco Immobilier, the Fonds immobilier de solidarité FTQ and Fiera Properties have partnered on a $700 M mixed-used development on the former site of the Le Spectrum de Montréal. MAESTRIA, the largest mixeduse real estate project in Montréal’s Quartier des spectacles, will consist of two towers of 51 and 53 storeys. One-third of the 1,500 units will be designated rental. Construction is set to begin at the end of 2019.

Edmonton-based Saroukian Group is developing Central Parc Laval, a sixtower transit-oriented development that will contain 1,400 high-end residential rental units, a luxury hotel and retail space. The first building, currently under construction, will contain 22 storeys with 198 units and is slated for delivery next July. Construction of the final building is scheduled to wrap up in 2023. Amenities will include an infinity pool, floor-to-ceiling windows, high ceilings, high-end stainless appliances and a concierge service.

Sifton Properties announced it had broken ground on Helio, a 10-storey, 115-unit mixed-use apartment tower in London, Ontario. When complete in April of 2020, Helio is slated to be the most energy-efficient residential high-rise in Ontario.

The student housing sector has been attracting more interest and capital. Over 1.5 M students are enrolled in Canadian post-secondary institutions and generate a huge demand for housing.

A recent report in the Economist revealed that student housing attracted US$16 B worldwide investment in 2016, as sovereign wealth funds increasingly target the sector.

ASH REIT, which focuses on student housing, launched last July. Since then, the private REIT has acquired seven properties across Ontario containing more than 3,300 beds. Its first acquisition was 181 Lester Street in Waterloo, 500 meters from both the University of Waterloo and Wilfrid Laurier University. The 18-storey building has 455 beds in fully-furnished suites, and offers high-end student-oriented amenities.

“Currently, only about 3% of Canadian university students live in offcampus purpose-built student accommodation compared to 10% in the U.S. and 12% in the U.K.,” said Sanjil Shah, ASH REIT Managing Partner. “We are 10 to 15 years behind those markets, even though our student population is growing at a much higher rate fuelled by both domestic enrolment and our increasing share of international students.”

Significant amount of capital is flowing into the land sector in the GTA but is easing on the West Coast.

Despite a reported moderation of the Greater Toronto Area’s single-family housing market, there has been no corresponding decrease in either demand or price of residential land, CBRE reports. “A powerful combination of constrained supply and population growth continues to support recordsetting land investment and, unfortunately for homebuyers, increasingly steep competition for residential land.”

In 2018, Metro Vancouver’s residential land sales hit $627 M, lower than in 2016 and 2017 when sales sailed past the $1.1 B mark for the first time.

The downward shift began in the last half of 2018, as an avalanche of government policies, interest rate hikes and a subsequent 40 percent plunge in housing sales hammered developer and consumer confidence, noted Casey Weeks, SVP at Colliers.

Here are some of the major transactions of the past few months.

Ten years after reports first surfaced that Celestica was looking to sell its 60.5-acre campus at Don Mills and Eglinton in Toronto, the deal has finally closed. Aspen Ridge Homes purchased the site which is on the Eglinton LRT for $347 M.

Celestica’s head office will move into about 100,000 sq. ft. in a new office tower to be built on the corner of Eglinton and Don Mills, according to CBRE’s Mike Czestochowski who brokered the deal. He said the tower will be approximately 200,000 sq. ft. and that at least one more office tower, along with ancillary retail, mixed-density housing and a community centre, will be built on the Celestica site

In October, Saputo Dairy sold its 18.7-acre facility in Burnaby to Peterson Investment Group for $209 M.

In Downtown Vancouver, Harlow Holdings bought 0.993 acres for $164,750,000. The land was improved with an eight-storey residential strata building and a three-storey commercial building. The apartment component was part of a strata windup.

In November, Phantom Development bought 225 Mutual Street in Toronto, a 0.799-acre site, for $82.1 M.

In January 2019, 9255 Airport Road West in Hamilton sold for $44 M. The 78.2 Acre site was bought by Cachet Developments.

In June 2018, Qualico acquired 316.4 acres in Chestermere just outside of Calgary for $42.2 M.

Qualico also picked up 353.5 acres in Edmonton on Meridian Street N.E. for $41.1 M from Walton Group of Companies.

In Brantford, Lindvest bought 58.2 acres on Shellard Lane from the City for $30 M.

Developer Mondev bought 0.896 acres in Ville-Marie for $26.9 M in January.

Altus Group forecasts that land sales are expected to improve from 2018 levels. Some uncertainty has been introduced to this sector, with the Province of Ontario’s proposed changes to the Growth Plan for the Greater Golden Horseshoe and the introduction of the Local Planning Appeal Tribunal (LPAT), it says.

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.