Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the performance of the Toronto Real Estate Market, click the following Insights.

Changing economic conditions, slowing global economic outlooks and repatriation of foreign capital, cited as contributing to the lower investment volume.

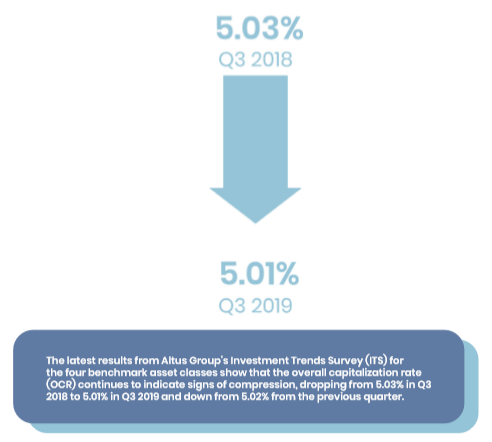

The Canadian real estate investment market is coming back after a very slow end to 2018 and a slower start to 2019.

Second quarter investment volume reached $12.5 B, a 40% increase from the first quarter but down 14.5% from the same time last year, Altus Data Solutions reports.

In terms of investment transaction volume, Toronto was the top-performing market in the second quarter, while Calgary and Ottawa showed the highest year-over-year increase, Altus stated. Moreover, Calgary and Edmonton exhibited a gain in investor preference this quarter gaining momentum from the first quarter.

Cap rates on core assets like downtown office and single-tenant industrial have plateaued as buyer pools dry up and sellers are forced to make more concessions, Jones Lang LaSalle stated in their Q2 Capital Markets Insight. Cap rates on marginally riskier assets like the suburban office in many cases are trending slightly upward, while retail cap rates continue to rise.

The end of H1 2019 has been characterized by a noticeable change in the buyer pool, according to Altus. Canada’s pension funds as well as international groups are shying away from stabilized assets. Fund managers have filled the gap, with acquisitions far outweighing dispositions.

Private investors have been the most active group of purchasers having acquired over $8 B in property.

However, at the end of the third quarter, there has been a flurry of capital movement, especially among REITs, indicating that 2019 will end on a strong note.

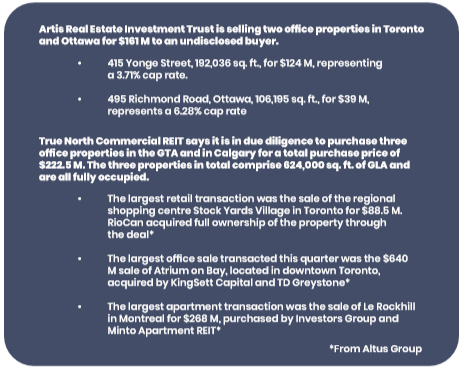

Choice Properties REIT has agreed to sell a portfolio of 30 properties (27 retail sites and three distribution centres) across Canada for $426 M. At the time of writing, the purchaser had not been revealed.

All the properties included in the sale are in secondary or smaller markets across the country. The purchaser also has the option to acquire two additional stand-alone retail properties for $29 M. If exercised, the additional properties are scheduled to close in Q4 2019.

Akelius Canada has sold 12 GTA apartment complexes to Starlight Investments for $176.8 M.

The properties include 19 buildings and 626 suites. Many of the properties were peripheral to Akelius’ core portfolio and originally acquired in conjunction with other properties, RENX reports.

Summit Industrial Income REIT has acquired 1.2 M sq. ft. of property and development land in an industrial park along the Hanlon Expressway in Guelph, just west of the GTA.

The REIT will acquire a new, single-tenant light industrial property and a second recently constructed multi-tenant light industrial property for $57 M. The two properties total 431,390 sq. ft.

In addition, Summit will acquire a 50% interest in 49 acres of development land in the same industrial park for $13.8 M, entering into a 50/50 JV with Cooper Construction Limited.

Summit Industrial Income REIT has also sold its interests in two data centres in Montreal and the GTA for $178 M.

Pure Industrial Real Estate Trust (PIRET) has purchased an 11-property industrial portfolio in the Greater Montreal Area from Healthcare of Ontario Pension Plan (HOOPP) for $249 M. Most of the buildings are located on the island of Montreal and were built during the early 2000s.

The 1.5 M sq. ft. acquisition, which is expected to be one of the biggest industrial real estate transactions in Canada this year, includes warehouses, distribution centres and logistics buildings. It is also believed to be one of the largest industrial transactions in Montreal’s history, if not the largest, according to RENX.

Unrelenting demand for office space, which is led primarily by a red-hot tech sector and coworking providers, will keep availability at near rock bottom, according to Cushman & Wakefield.

The national unemployment rate reported in August was 30 bps higher than May’s, which at 5.4% was the lowest it has been since 1976. Employment has grown in the Tech, FIRE and self-employment categories, which is helping to fuel the demand for office space across the country.

The national vacancy rate dropped to 10.1% in Q2 2019 from 11.6% in Q2 2018 and 10.4% in the previous quarter. The availability rate also fell in most major markets, signaling a robust leasing market, according to Altus Group.

Downtown Toronto vacancy crept up slightly to 3.5% in Q2 from 3.4% in Q1, reported Altus Group. The increase will have little impact on market dynamics during the remainder of 2019. The unrelenting demand, it states, which is led primarily by a red-hot tech sector and coworking providers, will keep availability at near rock bottom.

Nationally, approximately 21 M sq. ft. of inventory is currently under construction in the third quarter, of which 13 M sq. ft. has already been leased. Just under 11.4 M sq. ft. of the space under construction is in the GTA market.

The downtown average net asking rent has been on a steep upward trajectory, appreciating by close to 40% during this 3-year period. It now stands at $44.77 per sq. ft.

TD Bank Financial Group leased 903,000 sq. ft. at 160 Front Street West, a Cadillac Fairview development that is now fully leased. Construction of the 47 storey tower commenced this quarter and is scheduled for completion by 2022.

In Q2, King Portland Centre, located at 602–620 King Street West, was completed. The joint venture between Allied Properties / RioCan brought 255,565 sq. ft. of new inventory to the Downtown West submarket. This project is 100% leased by Shopify and Indigo.

CBRE states that coworking activity is helping to fuel the relentless office demand in Toronto’s downtown market. In addition to the 105,000 sq. ft. at The Shift, Spaces is planning on opening a 50,000 sq. ft. location at the Royal Bank Plaza and 40,000 sq. ft. at 1655 Dupont Street.

Canada’s flex office market has grown from about 1.5 M sq. ft. in 2014 to over 6.05 M sq. ft. in 2019, according to CBRE.

As this category grows, its model is shifting to take into account more innovative lease structures possibly affecting building valuation.

CBRE predicts in its September report on Flexible office space. There will be fewer traditional leases between landlords and operators with more onus on landlords to accept and manage risk.

As flex office space becomes more mainstream, lenders and investors are starting to see the benefits of moderate exposure as part of a well-diversified tenant roster, according to Alex Colpaert, Head of Offices Research at JLL EMEA. Buildings with a high percentage of flexible space are increasingly seen as viable investment propositions, he writes.

In its 2019 Commercial Real Estate Outlook, Deloitte stated that these newer opportunities may be more ideal for investors— “Investors seem to realize that their investments should be tied to the changing nature of work and tenant preferences. As such, the new capital commitment is unlikely to flow entirely into traditional CRE.”

Deloitte found that over half of investors surveyed have plans to invest or increase investments in properties with flexible leases, and 44% plan to do so for flexible spaces. In general, survey respondents specializing in mixed-use and nontraditional properties plan to increase their capital commitment by a higher percentage than those focused on traditional properties.

The 30.4 M sq. ft. of industrial space under construction at the end of the third quarter may do little to alleviate supply shortage.

The national vacancy rate at the end of the second quarter of was 2.0%, according to numbers from Altus Group. This rate is down slightly from 2.2% in the first quarter and remains very tight.

The industrial vacancy rate is down across most major markets, except for Calgary compared to the same quarter last year. Toronto and Vancouver continue to have the tightest vacancy rates.

Furthermore, the third quarter of 2019 was another record-breaking quarter for the GTA industrial markets.

Due to strong demand and severe supply shortages, industrial availability in the GTA fell to a historic low of 1.4%. Tight conditions continued to exert upward pressure on the asking rental rate, which reached $9.59 per sq. ft. in GTA— a 21.9% year-over-year increase, Altus Group stated. With a record 19.5 M sq. ft. under construction in the third quarter, developers are moving as fast as possible to meet demand.

Absorption reached 905,070 sq. ft. in the second quarter of 2019, pushing the year-to-date total to 1.5 M sq. ft. in the GTA. Of the new supply under construction, speculative builds make up 45%, and build-to-suit accounts for 55%. At the end of the quarter, 57.4% of the speculative product was already preleased, according to Cushman & Wakefield.

E-commerce and food warehousing and distribution continue to drive demand for space in the GTA. Small-parcel delivery services are in high demand, driven by e-commerce. Purolator recently announced plans for a 430,000 sq. ft. automated package-processing facility in Etobicoke, valued at $330 M. This facility will be part of a larger $1 B investment by Purolator to form a national “super hub” for e-commerce order processing.

“The voracious demand for industrial space has put upward pressure on all kinds of costs— occupancy costs, land costs, construction labour and materials costs, and development charges. Steel tariffs linked to the ongoing North American free trade discussions have also increased the cost of industrial construction,” said Bill Argeropoulos, principal and practice leader for research in Canada for Avison Young.

As older office and industrial products begin to show their age, and with many becoming near obsolete, demand is rapidly rising for more modern facilities with newer amenities or with clear ceiling heights above 32 feet, among other features. Developers are recognizing the ability to obtain significantly more rent by investing in properties and bringing them up to date, Altus Group stated.

In the coming quarters, vacancy is expected to remain stable at historic lows while rents are expected to continue to grow rapidly, JLL reports. “Rents will likely begin to level off in 2020 as the wave of new construction hits the market. Buildings under construction are expected to ramp up through 2019 as developers try to get product ready for 2020 delivery”.

At Upper Canada Mall in Newmarket, work-sharing startup Lauft recently set up shop at a site next to a former Target outlet. Lauft is now talking to other landlords about moving into their shopping centres. Oxford Properties Group is piloting various office-sharing initiatives at its sites while expanding its indoor amusement parks, food halls, lounges and restaurants.

Susan McGibbon, co-founder of retail consultancy Three Sixty Collective, predicted malls and other mixed-use developments will keep adding more co-working spaces.

Altus Group reports that investors continue to focus on transforming older retail properties into mixed-use communities, catering to changing demographics and customer demands by combining features of retail, entertainment, office and residential uses into a single location. Many of these properties are in well-located areas near major road networks and transit nodes, making them ideal properties for successful intensification.

An example of this transformation trend is QuadReal Property Group’s recently announced redevelopment plans for Cloverdale Mall in Etobicoke.

QuadReal plans are to include a variety of uses including retail, residential, parks and open spaces on the 32-acre site.

Cloverdale will be the third major mall redevelopment undertaken by QuadReal in Canada. Their other projects include Oakridge Centre in Vancouver and Bayview Village Shopping Centre in Toronto.

Ninety percent of worldwide retail sales are still done in physical stores, according to a Bloomberg Intelligence report. In addition, 43% of consumers are likely to spend more money shopping at a store that offers a meaningful experience, according to a 2019 Storefront retail trends report.

JLL found people who dine at malls generate about 12% more in sales while Canada-based Cadillac Fairview’s upgraded food courts have yielded a 20% increase in sales per square foot.

As consumer spending shifts, entertainment is now the primary driver to brick and mortar locations (61%), followed by dining (53%), according to the new ICSC Mix of Uses Survey.

Despite growth in supply pipeline, new construction is not keeping up with rising demand for rental housing.

With national apartment vacancy last pegged at 2.4% by CMHC, rent growth has accelerated. Over the last two years, average rents for purpose-built rental units have grown by 4.4% annually at the national level, by 5.0% in Toronto and by 7.1% in Vancouver.

Performance drivers, including a growing population, rising home ownership costs and lack of rental supply, are becoming entrenched in many markets across the country, which means the appeal of multifamily assets is likely to increase.

Canada’s population grew by 1.1% per year from 2009 to 2018 and is expected to continue expanding at a rate of 0.9% over the next four years, outpacing all other G7 nations by a considerable margin, CBRE states. As the population has grown, so too has demand for housing, particularly for purpose-built rental units.

Recent reports have shown that when comparing affordability across global cities, Canadian markets consistently rank as some of the least affordable in the world.

Rental inventories in major Canadian markets are limited compared to their global peers. The largest rental market in Canada is Montreal with just under 600,000 units, a formidable total. Toronto follows with 313,000 units, slightly over half of Montreal’s total, and then comes Vancouver with only 109,000 units. CBRE notes that adding secondary market rental units, privately owned condominium rentals, to these totals closes the gap in certain cases, but it’s clear that renters in most markets across the country remain underserved.

Investment volumes in the multifamily sector reached about $3.9 B in the first half of the year, recorded by Altus Group. It is unlikely that the sector matches its record pace of 2018, but this looks poised to be its second-highest year on record, JLL states.

High investment volumes continue to be driven not only by low vacancy but the perception among many investors that multifamily has the capacity to maintain its strong fundamentals even in an economic downturn.

The Ontario government recently unveiled its Housing Supply Action Plan, which focuses on incentivizing the supply side of the housing market and reducing impediments to the development process so that more units are brought to market. Developers have responded: more purpose-built units will be delivered between 2019-2021 than were delivered between 2012-2018.

A variety of government programs are beginning to shift the tides. The share of rental units as a percentage of the total high-rise units under construction has been increasing steadily over the last five years. While still not fully balanced, rental’s share of the new construction pipeline is now 35.9% based on the most recent data. Despite this slow shift towards more rental construction, new supply is not likely to meet the demand for the foreseeable future, CBRE predicts.

In the quest for yield, investors are turning to alternative asset classes.

Demand is shifting toward historically less-trodden areas of the property market that offer superior returns, something that has become increasingly important to property investors facing record-low yields around the world, JLL reports.

These alternative sectors include properties like data centres, student housing, self-storage, education and senior housing.

“For many years, non-traditional real estate was not fully appreciated,” says Tyler Blue, Vice President of the Advisory and Consulting arm of research firm Green Street Advisors. “Once the broader real estate investment community caught on, more capital flowed in, particularly as the more traditional real estate sectors became fully valued. So, the more progressive investors benefited and the institutions have followed their lead,” Blue says.

In September, TD Asset Management Inc. (TDAM) launched the TD Greystone Real Asset Pooled Fund Trust, a fund focused on Canadian and global real estate and infrastructure investments as well as publicly traded securities.

Rob Vanderhooft, Chief Investment Officer, TDAM said that, “we believe that alternative asset classes, such as real estate, mortgages and infrastructure, can be a source of accretive returns with the potential to enhance portfolio diversification, particularly in environments where inflationary pressures start to pick up.”

Data Centres

“The global demand for data storage and processing has grown exponentially over the past few years, driven by trends like the increase in mobile devices, the internet of things, cloud services and the rise of digital photography and social media,” Peter Russell of Urbacon says.

The imminent rollout of the 5G mobile communications network and the significant increase in data that will need to be processed, stored and distributed will only increase the demand for data centres.

With the onset of 5G, a massive boom in edge computing is expected to take place, transforming the way enterprises manage their networks. According to experts, the edge data center market is expected to exceed US $16 B by 2024, growing at a compound annual growth rate CAGR of more than 20% in the next five years.

Edge computing is defined as data processing power at the edge of a network instead of in a cloud or a central data warehouse. Edge computing enables data processing as close to the source as possible and allows for faster processing of data and enhanced customer experiences.

Cologix announced the opening of a new 18,000 sq. ft. data center in downtown Toronto. The new data center, known as TOR3, is located on the same campus as TOR2 at 905 King Street West. It is their third data centre in Toronto. The company has 10 data centres in Montreal and three in Vancouver.

Jones Lang LaSalle suggests that municipalities and appraisers are struggling with how to properly assess the value of an asset whose main attribute is not its physical footprint but rather its connectivity.

Student Housing

The student housing sector has been attracting more interest and more capital. Over 1.5 M students are enrolled in Canadian post-secondary institutions and generate a huge demand for housing.

Growth in student population throughout Ontario has generated significant interest for purpose-built student housing accommodation, JLL stated in their H1 2019 Capital Markets report. Kitchener-Waterloo currently accounts for about 50% of all student housing in Ontario, suggesting room for growth in other college towns like Kingston, London, Hamilton, and others throughout the GTA. Alignvest Student Housing REIT was formed in 2018. Since then, the private REIT has acquired seven purpose-built student residences in Ontario with looks to expand into Halifax and across the country.

“Currently, only about 3% of Canadian university students live in off-campus purpose-built student accommodation compared to 10% in the US and 12% in the UK,” said Sanjil Shah, ASH REIT Managing Partner. “We are 10 to 15 years behind those markets, even though our student population is growing at a much higher rate fuelled by both domestic enrolment and our increasing share of international students.”

Toronto-based developer IN8 Developments Inc., a pioneer in the student-condo niche with its Sage brand, now has 13 buildings in Waterloo. Two more are in the construction phase in Waterloo and Kingston, Ontario.

Toronto-based Centurion Asset Management Inc. oversees a private REIT that also owns student housing. The $1.7 B Centurion Apartment REIT is 17% invested in off-campus accommodation, in addition to apartment buildings and mortgages.

This REIT, which was launched in 2009, has more than 2,700 beds in nine student properties in Waterloo, Montreal and London, Ontario.

It has been suggested that Brexit’s impact on the UK’s post-secondary tuition costs could also have some flow-through implications for Canadian universities and student housing providers. A significant hit to the affordability of UK education could potentially divert students elsewhere if/when they are confronted with fees double to triple the rate that holders of EU passports have traditionally enjoyed.

Infrastructure

Preqin reports that infrastructure fundraising has been smashing records every year for the past four years, with US $90 B secured by funds closed in 2018, with no signs of slowing down.

50% of infrastructure investors plan to increase their allocation to the asset class over the longer term. The largest proportion (73%) of investors allocate to infrastructure for diversification. Other key attractions include the offer of a reliable income stream (44%), infrastructure’s low correlation to other asset classes (42%) and its ability to act as an inflation hedge (40%) according to Preqin’s Investor Outlook: Alternative Assets H1 2019.

Infrastructure, particularly for pension funds and other structurally long-term investors, has appeal as a natural hedge against inflation, RBC notes.

According to the Pension Investment Association of Canada (PIAC), investment in infrastructure among PIAC members has grown from 3.59% in 2008 to 8.17% in 2018.

In addition, there is an expanding universe of P3 investments in infrastructure, encouraged both by the current government’s focus on accelerating infrastructure development and the creation of Canada’s new Infrastructure Bank.

The Canada Infrastructure Bank, part of the government’s Investing in Canada infrastructure plan, is investing $35 B of federal capital into infrastructure projects. This initial funding is designed to attract private sector and institutional investment to new revenue-generating infrastructure projects that are considered to be in the public interest, such as public transport, social and green infrastructure.

In their brief, Can P3 Fill The Infrastructure Gap, AON reports that there is an increasing level of institutional awareness of infrastructure as an asset class around the world. This parallels the increasing need for renewing and upgrading infrastructure in many major developed economies as well as the unfulfilled requirements of economies everywhere.

In September, Canada Pension Plan Investment Board (CPPIB) announced that it had made its first infrastructure investment in Indonesia with the acquisition of a 45% interest in the Cipali Toll Road.

CPPIB has a diversified, global portfolio of infrastructure assets and makes direct investments through many of its nine offices worldwide. CPPIB’s Infrastructure group is focused on investing in quality, large-scale core opportunities with dependable, like-minded partners. On June 30, 2019, CPPIB had $33.1 B invested in infrastructure assets globally.

Across the country, development and urban revitalization occurring on a scale not seen in a generation, propels new trends and technologies.

Adaptive Reuse is a concept that is trending across the globe.

Adaptive reuse is the transformation of a building from one use to another and is breathing new life and vitality into cities all around the world.

“Obsolescent buildings might be wrong for their current use, but might also be adaptable to something more suitable,” says JLL Head of Asia Pacific Research, Dr. Megan Walters. “Investors prepared to think creatively can acquire such buildings at discounted prices."

In Shanghai, Pamfleet has converted the former Starway Parkview South Station Hotel into a co-living facility. Pamfleet and its partners converted the 56-room hotel into 67 apartments including studio, one- and two-bedroom units, a gym with a pool and tennis courts, and more 10,000 sq. ft. of retail.

In Irondequoit, upstate New York, developer Pathstone Corporation has announced plans to adapt part of the redundant Skyview on the Ridge shopping mall into a 157-unit senior care facility. Another part of the mall will be converted into a community centre.

In Calgary, Minto Apartments has converted the aging International Hotel into premium long- and short-term rental apartments now known as The International. The newly renovated building is a 35-storey tower with 252 units featuring a rooftop terrace, lobby bar, full-service fitness centre, party room, media room and modernized indoor pool. The building has direct access to the city’s downtown Plus 15 indoor pedestrian walkway systems and suites range in rent from $1,499 to $2,279 per month for one-bedroom and two-bedroom units.

Developers of self-storage facilities are buying vacant retail properties and redeveloping them into the new use. The locations are often very strong, and the low cost of redevelopment helps make these deals work. Of the new self-storage properties that have opened since 2015, 7% were converted from former retail buildings and 65% were constructed from the ground up, according to research firm CoStar Group. 23% were converted from industrial buildings.

Modular construction is a process in which a building is constructed off-site in a factory-styled manufacturing facility and has experienced significant growth in recent years.

The potential to adopt modular in construction is great, according to a McKinsey & Co. report released in June. The report found that the market value for modular in new real estate construction could reach US $130 B in Europe and the US by 2030. It found that some modular projects have accelerated project timelines by 20% to 50%, and some developers have saved 20% in construction costs.

At a time when many cities are facing housing shortages, modular construction provides a new affordable way of building homes.

Google recently spent upwards of US $30 M on 300 modular housing units built by the Bay Area–based Factory OS for its Silicon Valley employees. Microsoft is spending half a billion dollars on new housing in the Seattle area. There is a growing list of modular startups — such as Blokable in Seattle and RAD Urban in Oakland set to disrupt the construction industry.

Up to 80% of modular-construction processes can occur off-site using leaner workforces of moderately skilled, less-expensive labour. Work once done on-site by specialized labour can now be done at a fraction of the cost. Those in the building trades are still in demand, but now there is a larger pool of labour. Labourers work in a climate-controlled factory so there are no delays because of inclement weather.

In a JV with Netherlands-based hospitality company citizenM, BLVD Hospitality is developing a ground-up, 11-storey, 315 room modular hotel in downtown Los Angeles. The JV broke ground on the Gensler-designed hotel in June.

Thus far, developers have used modular for the construction of student housing projects, hotels, residential housing, healthcare offices and multifamily buildings.

Marriott is a big proponent of modular construction, opening several modular-built hotels in recent years and soon to open the tallest modular hotel in the world in New York this fall, Bisnow reports.

One of the major benefits of VR is the ability to showcase a property during all stages of development - including the pre-construction phase. Brokers are able to showcase the property down to every last detail, including amenities and location.

BIM is a way to visualize, manage and coordinate data about a building or other kind of construction project. It is like having a scale model of a building, but with the ability to identify every component, every material and every foot of wiring.

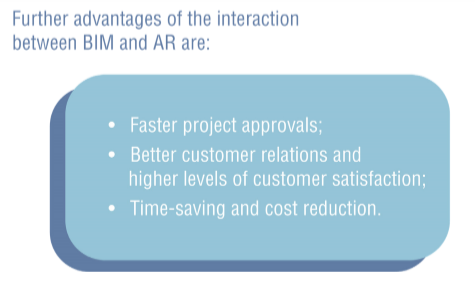

Building Information Modelling (BIM) becomes a particularly powerful tool when it is used with AR. AR’s ability to present the data in a clear and straightforward manner makes for an ideal visualization platform for BIM.

Evidence highlights that combining BIM and AR will drive the digital transformation of this sector. One of the biggest advantages of using this tech combo is minimizing design errors before moving to project implementation.

As Peter Marchese of Microdesk stated to Forbes, “I do believe that as [augmented reality] becomes more available, it will shape how the BIM data and information is used and consumed, especially on the construction and manufacturing side of things. I feel the real power of AR will be a boost to facilities and construction, especially when connected to real-time data from a connected IoT. It has the capability to make jobs safer, more efficient and productive, and the pilots that have used AR in manufacturing have proved these claims.”

The improved connectivity that will result from 5G will supercharge IoT and is likely to have significant impacts on the real estate industry.

Seoul became the first city in the world to offer 5G in April when it was launched by SK Telecom, KT (Korean Telecom) and LG Uplus. Other countries are close on its heels. US network operators have said they’ll start operating 5G this year. Canada will likely roll out 5G in 2020 while Japan is pledging to have a fully-functioning 5G network by 2022.

5G, or the fifth generation of wireless technology, is a standard designed to deliver data speeds greater than 1 gigabit per second and low latency of less than 1 millisecond. This means much faster data speeds (100 times the speed of 4G LTE) and less delay between the request for a data transfer and the start of the data transfer in a cellular environment.

5G is poised to be a very big deal, a far bigger transformation in mobile technology than any previous generational shift, says the Harvard Business Review. Its speed, capacity, and dramatically reduced power consumption and communications response times, or “latency,” will make possible an astonishing range of innovative new products and services.

Uber, with support from 5G technology, is planning to test its Uber Air flying taxi in 2020 with the aim of launching the service commercially in 2023 in Dallas-Fort Worth and Frisco, Texas and Los Angeles.

According to Qualcomm, the 5G mobile value chain alone could generate up to US $3.5 T in revenue by 2035.

5G’s higher speed and bandwidth will create fully wireless workplaces and impact everything from printers to elevators. Greater bandwidth would also allow artificial intelligence programs to analyze more data in real-time, allowing smart buildings to engage and interact with employees and landlords according to NAIOP.

It will also enable more efficient building maintenance in both commercial and industrial buildings, allowing technicians to address issues virtually and reducing downtime, equipment failure, and costly on-site visits.

5G networks will require many more base stations, which are physically smaller than a current cellular tower. They will also need to be placed much more closely together. 5G base stations could be placed every 250 meters, rather than the every 1 to 5 km needed for 4G.

In a commercial real estate scenario, the need to propagate signals will be challenged by a number of factors including the age of the building, the materials used in construction, the needs of a potentially diverse tenant base, and physical location just to name a few.

Real estate owners could see new opportunities to generate revenue as telecom companies seek to rent more space on rooftops and inside buildings for the additional electronic infrastructure they will need, said Len Forkas, President of Milestone Communications.

“Landlords need to recognize that 5G and improved connectivity will benefit them by increasing the overall value of their property assets,” said John Gravett, Cluttons Head of Real Estate Management . “The commercial value of a well-connected property thanks to increased rental revenues, minimizing voids and having happy tenants due to higher staff retention and the ability to work more efficiently, should not be underestimated.”

Millennials looking for affordable housing options are heading to ‘purpose-built’.

As more millennials become parents of school-age kids, and home prices in urban areas become out of reach for more families, there’s been a slow but steady push toward the suburbs.

This is a reversal from the past decade, during which some companies attempted to increase their attractiveness to talent by relocating to central business districts (CBDs) explicitly to be near a younger labour pool.

In Emerging Trends in Real Estate® 2020, the Urban Land Institute and PwC in September identified the migration of millennials to the suburbs as a theme for 2020.

In what the report dubs “the rise of Hipsturbia,” the hot locations outside of big cities are evolving: In addition to being more diverse, they’re also becoming more walkable, with developments that favour density, retail, recreation, and transit access.

Many of these new hot spots that located on the US East Coast are linked by old commuter rail stops. They have seen a renaissance with new apartments, eateries, and office space.

The live/work/play formula is what developers used to revive downtowns two decades ago, and they’re plugging it into the suburbs with good success, says Byron Carlock, PwC Real Estate Leader.

Cushman & Wakefield confirms this trend. “As millennials age, their priorities are changing, and they want more space. However, they don’t want to sacrifice city culture, energy and walkability that traditional suburbs typically lack. The cost of living in the world’s top-tier cities is growing much faster than incomes, and these high costs are bleeding further and further out of the urban core. Rents and the cost of living have also been rising in emerging alternative locations.”

The trend of population shift away from city centers in the US has prompted stakeholders in city development and urban planning, including government authorities and developers, to focus on the holistic development of suburbs. Further, given the emphasis on attracting and retaining talent, companies have become increasingly sensitized to this shift. Massive pressure on cities to accommodate growing populations created the need to develop cost-effective and self-sufficient areas to live, Cushman & Wakefield reported in The Edge Magazine Vol. 2.

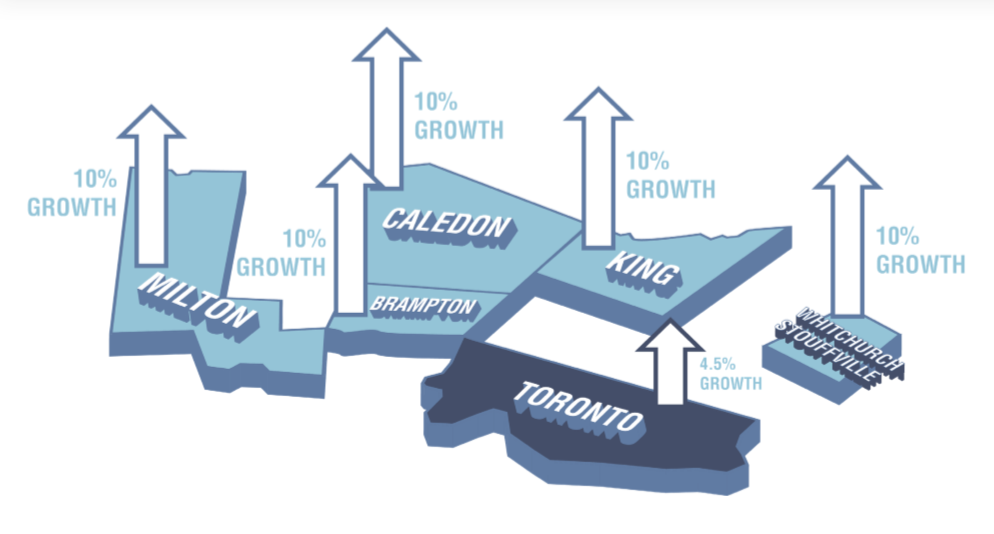

The growth of the suburbs has been apparent in Toronto as well. The latest census numbers highlight a number of spots in the Toronto census metropolitan experiencing significant growth. While Mississauga grew only slightly, areas further away like Milton, King, WhitchurchStouffville, Brampton and Caledon experienced upwards of 10% growth over the 2011 to 2016 period— more than double the 4.5% growth rate of the actual City of Toronto during that time, CBC reported.

With space at a premium and rising rents in core markets, tenants are seeking available products elsewhere, Altus Group reported in their Q2 market update. Smaller, yet growing secondary markets situated along major transportation routes may be their next best bet, as they offer direct access to both urban and suburban markets and, in many cases, more sustainable rents. In the Toronto suburban market, JLL reported that there was 714,771 sq. ft. of office space under construction in Q2 2019.

The suburban office vacancy rate is 11.7%. It has been on a downward trend since 2016 and the JLL states that this is expected to continue as a number of large tenants will take occupancy of their new spaces in the next six to 12 months.

Smart buildings improve tenant experience and promote energy and financial savings.

“Smart technology can significantly help to create an attractive, customized workplace environment, as well as enhance the efficiency of building operations,” says Tomasz Mizera, CRE Technology Delivery Director, JLL. “It has huge potential for helping tenants get the most from their space, save on operational costs and meet their sustainability goals.”

As more companies embrace flexible workspace, smart technology has a major role in helping landlords and companies understand and optimize the way spaces are being used. “In a flexible workplace, sensors make the office more accessible,” says Mizera. “The technology can deliver insights to better meet the needs of the people using it.

”The RBC Waterpark Place in Toronto uses sensors to facilitate many different aspects of the working day, from smart elevators getting employees to where they want to go in the shortest time, to keeping meeting rooms at optimal temperatures. Such small but critical adjustments to the office environment can have a huge impact on employee productivity.

CRE owners recognize the ability to realize significantly higher leasing fees with intelligent buildings. Accordingly, over 80% of new construction involves at least one facet of IoT and/or related Smart Building technologies.

In May, Cushman & Wakefield announced a new partnership with Stanford University’s Disruptive Technology and Digital Cities Program. The main aim of the collaboration is to identify, develop and launch transformative technologies within the commercial real estate space.

The shared focus will be to assess emerging technologies and societal trends, with the goal of leveraging these findings to develop practical applications in areas such as 3D visual modeling, property valuation, smart building operations and advanced data analytics.

BlueSky Properties recently completed a 9-storey building at 988 West Broadway and employed cost-saving smart technology. The AAA, 102,000 sq. ft. structure was the first office building in Canada fully equipped with View Dynamic Glass technology.

“The smart window system controls the amount of light entering the building by automatically tinting to block glare using nanotechnology. It can also be manually controlled down to the level of individual windowpanes via a tablet or other electronic device. The system can reduce incoming visible sunlight by up to 99.5%, representing a 20% savings on the operation of the building,” the company said.

988 Broadway is the first building in Vancouver and the first office tower in Canada to use the system for all its windows. The glass is also utilized on the Humber River Hospital in Toronto.

The company has completed roughly 22 projects in Canada, with another 30 locations underway. Smart glass market is expected to reach US $8.35 B by 2023 from US $3.32 B by 2017, at a CAGR of 16.61% between 2017 and 2023.

Buildings that have traditionally been mere brick and mortar enclosures are now capable of responding to real-time needs, Naveen Joshi writes in Forbes. “The fusion of sensors, cameras, actuators, and other IoT devices have made buildings smart. But, AI is what makes smart buildings ‘smart’ in the truest sense of the word. In addition to reduced operational costs, enhanced tenant experience, and improved asset utilization, smart buildings promote energy conservation as well.”

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.