Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the performance of RealREIT, click the following Insights.

Despite global economic instability and three interest rate hikes, Canadian REITs delivered positive returns.

Canadian REITs delivered positive returns in 2018 despite escalating trade wars, Brexit, rate hikes, slowing economic growth in China and political instability, which were all drags on the market.

The S&P/TSX Capped REIT Index has returned 5.6% last year, while the total return of the broader S&P/TSX Composite Index was down approximately 10% over the same period. REITs also delivered the second-best return of any TSX subsector, surpassed only by technology stocks.

REITs managed to outperform the capital markets despite the BoC hiking rates three times in 2018.

“We believe that economic growth and supply-demand levels are

more important drivers of REIT performance than interest-rate

changes, so long as the interest-rate changes are gradual and not

unexpected,” wrote RBC Capital Markets analyst Michael Smith.

Even so, rates are unlikely to increase in 2019. According to a poll

of nearly 40 economists in early July, the BoC will hold interest

rates at 1.75% through to the end of next year.

“For the Bank of Canada, there is no rush to cut interest rates.

At the same time, with the Feds moving relatively aggressively to

cut interest rates, the BoC by next year will have to cut at least

once in order to prevent the Canadian dollar from appreciating too

strongly,” said Benjamin Tal, Deputy Chief Economist at CIBC.

“So, the question is, how long can you divorce yourself from the

Feds if you are the BoC, and I say not for too long,” Tal continued.

Canadian REIT activism has been on the rise in recent years,

according to figures from Activist Insight, even as activism in the

broader Canadian market has dropped after peaking in 2015.

REIT activists’ demands reflect the wider trend of institutional

investors reshaping the corporate governance landscape and

challenging how boards think about fundamental issues, such

as strategy, risk, capital allocation and board composition. REITs

are responding to investor demands by engaging more often and

directly with shareholders in an effort to improve transparency and

accountability, EY reports.

“Canada is the most shareholder activist-friendly jurisdiction in

the Western world,” said Walied Soliman, Chair of law firm Norton

Rose Fulbright Canada.

Canadian law allows shareholders with a 5% stake in a company

to call for a special meeting, compared with 10% in the United

States, giving activists the ability to launch campaigns without

locking in too much capital.

REIT M&A deals in 2018 collectively hit their highest monetary

mark since 2007. One dozen transactions were either completed or

announced last year. The value of these deals was approximately

US $76.3 B, NAREIT calculated.

M&A observers believe the volume in 2019 will match or even

exceed last year’s figure.

“While 2018 volume was significant due to many REITs being

traded at a significant discount to their net asset value, we

anticipate 2019 being similar. There are many investors and a

great deal of capital waiting for the right time with values, cap rates

and so forth,” says Greg Ross, National Managing Partner of the

Construction, Real estate, Hospitality and Restaurant Practice

at accounting and consulting firm Grant Thornton LLP. “The real

estate fundamentals are very strong, with low unemployment, low

interest rates and high consumer confidence.”

The mature nature of this real estate cycle means investors continue to display a degree of caution – EY

With late cycle uncertainty emerging as the market slows,

institutional investors are allocating more capital to REITs than

private equity funds, as REITs have historically outperformed broad

equities in late-cycle periods.

For example, California State Teachers’ Retirement System

recently announced a US $100 M commitment to REITs, its firstever entry into the sector.

While institutional investors tend to favour private equity funds

when the market is expanding, he says that REITs outperform

them by 2.5 to 3.0% over the long term, reports John Worth, EVP,

Research and Investor Outreach with NAREIT.

“…Global REITs, as an asset class, are set up well to outperform

most other sectors in 2019 and deliver an attractive 9% to 10%

total return balanced between yield and growth, not just growth,”

said Samuel Sahn, Timbercreek’s Portfolio Management &

Research Executive Director.

While REITs are where smart money goes to hedge any volatility

that may come with a maturing real estate cycle, investment

criteria differ from one shop to another. Emerging trends that are

starting to shape the industry become a harbinger of the direction

of capital flows.

Small Cap vs Large Cap

A good portion of small-cap REITs are newcomers that have

significant growth potential, even though they are generally

regarded as more volatile and riskier in the short term than largecap investments.

Small-cap dividend yields are typically larger than the major

players, which is likely due to capital being driven into large funds

that are pushing down yields. Large-cap REITs generally offer

greater access to capital and liquidity for investors than many

small caps do, however, as they often pay out in dividends or other

methods that aren’t available for immediate liquidation.

A look at the current FFO ratios for large and small-cap REITs

shows that small caps are trading at a substantial discount to large

caps: 12.6x compared to 17.3x as of March 31, 2019. The last time

the ratio was lower was in March of 2016.

Sector Based

The industrial sector continues to grow, driven by the rise

of e-commerce. National vacancy is at its lowest levels and

development is not keeping up with demand. Timbercreek, in their

2019 Global Real Estate Securities Market Outlook reports that

“favourable demand and supply dynamics will be supportive of

rental and capital value growth in 2019, positively influencing the

share prices of industrial REITs.”

The convergence of real estate and technology will create a strong

growth for data centers, representing one of the best investment

opportunities in 2019.

The imminent rollout of the 5G mobile communications network

and the significant increase in data that will need to be processed,

stored and distributed is likely to have a significant impact on the

data centre sector.

With the onset of 5G, a massive boom in edge computing is

expected to take place, transforming the way enterprises manage

their networks. According to experts, the edge data center market

is expected to exceed US $16 B by 2024, growing at a compound

annual growth rate of more than 20% in the next five years.

Demographics

According to Environics Analytics, millennial households account

for 19% of all households, approximately half the number of

households headed by baby boomers. However, over the next 10

years, as mortality shrinks the baby boom generation, the number

of households headed by millennials will start to exceed those

headed by baby boomers.

These two divergent generations are primary drivers of demand

in the apartment market. Millennials preferring the flexibility that

renting affords while boomers are downsizing and are choosing the

convenience of maintenance-free living.

An important factor in driving demand for facilities that cater to

seniors’ needs is the growth in the population aged 85 and older.

Canadians in this age group also show a strong tendency toward

collective dwellings, with 31% living in this type of housing in 2017,

according to the PwC Emerging Trends report.

Technology

Technology is accelerating the pace of change and contributing to

a more dynamic and fast-moving real estate market.

For those unable to keep pace, the risk of asset obsolescence

is very real, with negative implications for portfolio value and the

business generally. The accelerated pace of change seen in our

markets makes obsolescence more relevant than ever before.

Investors, lenders and rating agencies are considering these

factors as part of their process in determining how to underwrite

companies and their real estate assets, according to EY.

REITs have become some of the most active and innovative

developers across Canada.

JVs are increasingly being used by REITs, particularly for mixeduse developments to help mitigate risk.

Allied has partnered with Perimeter Development Corp. to build a

300,000 sq. ft. mid-rise office building that will make up Phase III of

The Breithaupt Block in Kitchener’s Innovation District. Allied has

announced that it has signed a tenant to the space for a 15-year

lease.

In addition to the office project, Allied and Perimeter have acquired

two nearby parcels of land totalling 94,090 sq. ft. They plan to

construct an ancillary five-storey parking structure on the site,

with approximately 700 parking spaces, for use by tenants of The

Breithaupt Block.

Allied has partnered with Westbank on a number of projects,

including KING Toronto, a mixed-use development on King Street

just west of Spadina, and has partnered with RioCan REIT on The

Well project on Front.

RioCan REIT is leveraging transit-oriented retail assets it

owns in Calgary and Toronto into mixed-use projects with a

substantial mix of residential. In Calgary, RioCan has joined with

residential developers in a $70 M mixed-use retail and residential

redevelopment at its Brentwood Village Shopping Centre, which is

served by Calgary’s light-rail transit.

Artis remains active in new construction with about $202 M

invested in projects under development. That includes a mixed-use

tower in Winnipeg and new industrial spaces in Houston, Phoenix

and Denver. The REIT also has several planning projects not yet

at the construction stage. “These projects are progressing well

through the development stages,” said Jim Green, the REIT’s

CFO.

Crombie has a pipeline of two dozen sites for either development

or redevelopment, Executive Vice President and COO Glenn

Hynes told RENX in a recent interview. It is currently spending over

$500 M on redevelopments at five existing properties in Oakville,

Montreal, Vancouver, St. John’s and Langford, BC.

The projects comprise about 1.4 M sq. ft. of new leasable space;

452,000 sq. ft. of commercial area and 976,000 sq. ft. of residential

rental space. The largest project is 520,000 sq. ft. at Oakville’s

Bronte Village Mall where Crombie has partnered 50-50 with

Montreal’s PrinceDev on a $275 M addition of two rental apartment

towers of 10 and 14 storeys, respectively.

Crombie also recently acquired a $32.4 M, 20.25-acre industrial

site in Pointe-Claire, Quebec. The REIT will develop and own

a 285,000 sq. ft. customer fulfillment centre at the property for

Empire Company Ltd.’s online grocery home delivery service.

Empire is the parent company of Sobey’s, which maintains an

ownership stake in the REIT.

Acquisitions and merger activity have surged as REITs seek to

expand.

With a wide belief in the market that the current real estate cycle is

in its late stages, interest rates and cap rates are creeping up, and

debt is readily available. There’s also a large disconnect between

private and public real estate values, several analysts note. “The

backdrop is certainly conducive to M&A,” says Haendel St. Juste,

REIT Analyst at Mizuho Securities USA.

Since 2011, REITs have made gross acquisitions of over US $540

B; REITs also sold some $250 B of properties over this period,

resulting in net acquisitions of nearly $300 B according to NAREIT.

REIT M&A deals in 2018 collectively hit their highest monetary

mark since 2007. One dozen transactions were either completed or

announced last year. The value of these deals was approximately

US $76.3 B, NAREIT calculated. Included in this list of mergers

was:

- Prologis’ acquisition of DCT Industrial in a stock deal worth US

$8.4 B; - Blackstone to acquire all of Gramercy Property Trust’s

outstanding common shares for US $7.6 billion, cash; - General Growth Properties agreed to a buyout offer from

Brookfield Property Partners for US $9.25 B.

The merger of CREIT and Choice Properties last year created

Canada’s biggest real estate investment trust: 751 properties for a

total of 66.8 M sq. ft. of retail, industrial and office space.

At the time of the merger, Canadian REIT had plans to add 2.4

M sq. ft. of space through 15 projects that are currently under

development.

Nexus REIT was created through the combining of Nobel REIT

and Edgefront REIT in April 2017. Nexus REIT has a portfolio of

70 industrial, office and retail properties in Canada comprising

approximately 3.8 M sq. ft. of rentable area and valued at more

than $500 M.

Nexus completed a $3 M deal on April 2 to acquire four industrial

properties in Fort St. John, B.C., Estevan, Sask. and Blackfalds

and Medicine Hat in Alberta. The buildings are all occupied by

construction firm MasTec Canada and have leases ranging from

four to seven years.

Artis has a portfolio worth about $5.36 B with office, retail and

industrial properties in five Canadian provinces and six US states.

They are currently selling 27 properties over the next two to three

years and expects to sell more than $600 M in properties by the

end of 2019. Jim Green, the REIT’s CFO, said the divestment is

part of a strategy to increase both cash flow and to shore up share

prices. The REIT plans to increase its US presence and decrease

the number of office assets they own.

KingSett will acquire Dream Industrial REIT’s eastern Canadian

Properties for $271 M. The portfolio contains 38 assets and 2.8 M

sq. ft. of GLA. Brian Pauls, CEO of Dream Industrial REIT says,

“We plan to utilize the net proceeds from the sale to increase

scale in our target markets as we continue to transform, as well

as enhance the overall quality and performance of the Dream

Industrial portfolio.”

Dream Industrial also announced the purchase of two other

properties, one in Oakville, the other in Ottawa, for about $40 M.

“We remain focused on driving solid organic growth and improving

the quality of our portfolio,” said Lenis Quan, Dream’s CFO, in the

release.

US-based American Landmark/Electra America (ALEA) is in talks

to acquire Pure Multi-Family REIT. Pure Multi owns 22 properties

containing more than 7,000 residential units. The properties are

located in five general geographic areas, Dallas-Fort Worth,

Houston, Austin and San Antonio in Texas, and in Phoenix.

ALEA currently owns and manages approximately 28,000 units

valued at over US$4 B. The US firm has been extremely active in

mergers and acquisitions having completed, among others, the

acquisition of Apartment Trust of America, a US apartment REIT,

and the sale of approximately US $2 billion of apartment assets

to Starwood Capital Group and Milestone Apartments Real Estate

Investment Trust.

Crombie REIT announced in Q2 that it has entered into a second

agreement of purchase and sale to sell an 89% non-managing

interest in a 15-property portfolio for an aggregate purchase price

of approximately $193.3 M to an affiliate of private equity firm

Oak Street Real Estate Capital, LLC. Crombie will retain an 11%

ownership interest and will continue to manage and operate the

properties. The Transaction is scheduled to close in the fall of

2019. The first transaction Crombie did with Oak Street involved a

majority non-managing share of 26 properties for $161 M.

Minto Apartment REIT is breaking into the Montreal market and

increasing its Toronto portfolio with the purchase of 50% interests

in two multi-residential rental properties for $209 M. The REIT is

partnering with IG Investment Management to take a 50% stake in

Montreal’s Rockhill Property. Valued at $134 M, the deal will mark

Minto REIT’s first foray in the Montreal real estate market, bringing

a six-building, 1,004-suite property into its portfolio. In Toronto,

Minto REIT will also take a 50% stake in the 409-suite Leslie/York

Mills apartment complex partnering with existing owner HOOPP.

For both acquisitions, Minto REIT will act as the asset and property

manager, earning fees for those services.

“These acquisitions increase our suite count by 31%, while also

advancing our growth and geographic expansion strategies,” said

Michael Waters, the CEO of Minto Apartment REIT, in the release.

Melcor REIT announced this Spring that it had acquired a retail

property with warehouse space in Calgary, Alberta for $12.45 M.

Andrew Melton, President and CEO of Melcor REIT said, “this

acquisition fits well with our strategy to grow in markets we know

well and represents the continued redeployment of capital from our

asset recycling program. Being funded by the REIT’s line of credit,

this acquisition will be immediately accretive to AFFO.”

WPT Industrial REIT acquired 13 industrial properties in the US

for US $226 M this Spring. In addition to the 13 buildings which

total 2.2 M sq. ft. of leasable space, the portfolio includes three

parcels of land and is located in multiple American markets. The

acquisition adds properties to WPT’s current holdings in Chicago,

Milwaukee and Minneapolis and launches three new markets for

the REIT, including Los Angeles and Miami.

Supply is not keeping up with demand for rental apartments,

despite a significant increase in construction.

In 2018, growth in demand for purpose-built rental apartment units

outpaced the increase in supply across the country, causing the

vacancy rate to drop to 2.4%.

Matt Danison, CEO of Rentals.ca, said the new mortgage stress

test, higher interest rates and home prices have dramatically

increased the number of people looking for rental accommodation

this year.

“With near record-high immigration in Canada and record-low

unemployment, demand for housing is high, but flat or declining

resale house prices due to current and expected future credit

tightening has deterred many would-be first-time buyers from

entering the ownership market. That demand overflow is being

felt in the rental market, where very few Canadian markets are

offsetting demand with new rental supply,” added Danison.

Bob Dhillon, CEO of Mainstreet Equity, adds that rising interest

rates and the new federal mortgage stress test have made it more

difficult for prospective buyers to purchase homes, pushing them

into the rental market instead.

In 2018, average rents grew by 3.4% in Canada— higher than

the rate of inflation— to an average of $987, CMHC reported.

However, the average property on Rentals.ca was offered for rent

at $1,917 per month in May, an increase of 4% month-over-month.

The creation of affordable housing is a top priority across all levels

of government. As part of the National Housing Strategy (NHS),

the Rental Construction Financing Initiative provides low-cost loans

to encourage the construction of rental housing which is affordable

to middle-class Canadians across the country. The initiative has a

total of $3.75 B in loans available to encourage the construction of

more than 14,000 new rental housing units.

Details of Ontario’s new Housing Supply Action Plan were

announced in May and proposed to put in place the following key

measures:

- Preserve rent control for existing tenants;

- Encourage developers to build more rental housing by

exempting new rental units from rent control; - Cancel the Development Charges Rebate Program, which

it calls “expensive and ineffective,” estimating it will create a

savings of approximately $100 M over four years.

GTA rental completions have reached a 25 year high according

to a report from Urbanation. A total of 42,841 purpose-built rental

apartments were proposed for development but had not yet started

construction as of Q1 2019, and the number of purpose-built

rentals under construction was 10,694.

Solid employment growth, high costs of homeownership and a

preference to rent amongst millennials are underpinning strong

demand for apartments, while record immigration levels are

expected to drive demand even higher.

These factors, together with insufficient and constrained rental

supply, are expected to only intensify housing challenges,

especially in Canada’s gateway markets.

Due to the growing imbalance between housing demand and

supply, the multi-family sector is expected to continue to see

steadily increasing rents along with low vacancy rates for the

foreseeable future.

“When you look at the underlying fundamentals in Ontario, there

is, what we believe, a shortage of affordable housing options in

the province, and given that, we continue to see strong leasing

demand in the Ontario apartment sector that benefits from a lack

of affordable options plus population growth within the province,

particularly in the GTA,” Brad Sturges, the Real Estate and REITs

Analyst from Industrial Alliance Securities, told the Globe & Mail.

“We think there is still an imbalance between demand and supply

in the province, which should continue to be positive for market

rental rate growth.”

RioCan plans to borrow about $200 M of CMHC-backed financing

for their 36-story rental tower at Yonge and Eglinton called “

eCentral”.

“The cheapest debt in town is CMHC-guaranteed debt, which you

can put on rental residential buildings, so we’re quite hopeful that

our first CMHC transaction will take place before the end of the

summer,” Ed Sonshine said in an interview with BNN Bloomberg.

In the past 18 months, RioCan has been pivoting towards

apartment rentals. Its new strategy is retail and condo/apartment,

focused in Canada’s 6 major markets. It is well into its process of

selling off close to a hundred of its retail properties in secondary

and tertiary markets and switching its focus towards building new

apartment rentals.

RioCan in March 2018 also launched its residential brand: RioCan

Living. Through the brand it now has 8 projects in development

that will amount to 2,100 units, 13 additional projects are in early

planning stages, with a remaining 25.1 M sq. ft. of development

opportunity.

Diversification enables REITs to gain exposure to key markets and

dilute their exposure to sectors experiencing headwinds.

With its acquisition of CREIT, Choice Properties diversified away

from grocery-anchored retail and into office and residential

properties.

“I would say (the acquisitions) are quite strategic and one of the

important aspects of this transaction for Choice properties is the

increased diversification,” said Galen Weston.

He pointed to the industrial sector as an example. “Choice already

owns a number of industrial-type units, but they are Loblawoccupied. So now we are increasing our exposure to industrial,

which is something we were very anxious to do,” Weston said.

The acquisition gave Choice a portfolio comprised of 78% retail

(based on NOI), 14% industrial and 8% office. It had 9% industrial

and 2% office.

WPT’s purchase of 13 industrial buildings enabled them to

diversify into major US markets.

RioCan is in the middle of a transformation that will see the

company diversify its portfolio by adding a host of residential/retail

mixed-use properties, the first several of which are currently under

construction and set to open later this year.

RioCan is offloading non-core assets, raising approximately $2 B

towards the venture.

By shifting towards residential properties, RioCan is both offsetting

any potential slowdown in the retail sector while concurrently

offering what will be thousands of residential units in the major

metro areas across the country.

Boardwalk REIT has partnered with Redwood Properties in a JV to

build two residential towers totaling 365 rental units in downtown

Brampton, across the street from the GO Station.

Boardwalk CEO Sam Kolias said the addition of newly constructed

rental communities in a new target market is consistent with the

REIT’s long-term strategy of diversifying its portfolio. Kolias added

in an interview with RENX, that this new development provides “a

measured, high-quality entry” into the GTA.

While some REITs diversify by acquiring properties in sectors or

markets in which they are underexposed, others are focusing on fringe real estate asset classes.

NAREIT tracks 11 REITs in its “specialty” sub-sector. However,

research firm Green Street takes a broader view and it counts

more than 40 non-traditional REITs that also includes operators of

data centers, manufactured homes and self-storage among other

sub-sectors. Combined, those non-traditional REITs represent 37%

of the equity REIT market cap.

Easterly Government Properties is a US REIT that focuses on

investing in US government-leased buildings. The US government

is the largest employer in the world and the largest office tenant

in the US. The portfolio is 100% leased and has a weighted

average age of 11.5 years. Most of its buildings are office buildings

(67%) and the rest are either courthouse/office (6%), lab (9%),

VA Outpatient (11%) or others (7%). One of the REIT’s recent

acquisitions was an FBI facility in Salt Lake City.

Innovative Industrial Properties was founded in San Diego in 2016

to capitalize on the growing medical marijuana market in the US.

It has become the landlord to some of the country’s biggest pot

farmers. Typically, the company buys a property that a grower has

already established and then leases it back to the grower.

Americold Realty Trust is one of the newest additions to the

market. The company, which is one of the largest REIT focused

on the ownership, operation and development of temperaturecontrolled warehouses, went public in January 2018 and had a

market cap in excess of US $6.6 B.

Based in San Francisco, Digital Realty Trust is a data center REIT

with over 170 properties in 11 cities on four continents.

Founded in 1902 and headquartered in Baton Rouge, Louisiana,

the Lamar Advertising Company is a REIT that sells advertising

space on billboards, buses, shelters, benches and logo plates.

With more than 330,000 displays, it is one of the largest outdoor

advertising companies in the world.

ESG Initiatives grow across the capital markets as financial

viability is measured.

Responsible investing is widely understood as the integration

of environmental, social and governance (ESG) factors into

investment processes and decision-making. ESG factors cover a

wide spectrum of issues that traditionally are not part of financial

analysis, yet may have financial relevance.

The term was introduced in 2005 in a study written by Ivo Knoepfel

entitled “Who Cares Wins.” ESG investing is now estimated at

over US $20 T in AUM or around a quarter of all professionally

managed assets around the world, according to Forbes.

ESG breaks down into three components.

Environmental refers to an organization’s processes, policies,

practices, and impact related to the natural environment.

NAREIT reports that 79% of REITs owned green buildings in 2018

which were certified by at least one of the following bodies: LEED,

Energy Star, BREEAM, CASBEE, BOMA or HQE23.

The majority of REITs have reduced their energy consumption

every year for the past three years, which is reflected in a 2%

reduction in absolute energy consumption amongst REITs in the

past year, or the equivalent of energy usage from 31,223 homes,

according to the 2018 GRESB Portfolio Analysis Report.

Social refers to an organization’s processes, policies, practices,

and impact with regard to the people – both internal and external –

with whom it interacts.

Prologis launched its Community Workforce Initiative in 2019.

The program collaborates with local workforce development

organizations, nonprofits and schools to offer individuals interested

in careers in logistics, distribution and transportation the following

opportunities:

- Mentorships

- Skills training

- Internships

- Job placements

The company is also launching the Prologis Trade and Logistics

Lab in Miami, where more than 300 high school students will be

offered experiential learning opportunities and internships.

Governance refers to an organization’s processes, policies,

practices, and impact with regard to its organizational design,

transparency measures, policies, protocols and procedures, and

formalized governing bodies, roles and responsibilities.

Acquired by Brookfield Properties in December 2018, Forest City

Realty Trust set supplier diversity and hiring goals that adhered to

or surpass local requirements. For projects on existing properties,

it required at least one diverse vendor to be included in the bidding

process.

To evaluate and select locally based suppliers, Forest City utilized

a supplier-locator database tool that allowed it to sort diverse

suppliers by regions. The company also set internal goals to

support the growth and success of minority and women-owned

businesses.

In March 2019, Bentall Kennedy and REALPAC in conjunction

with the United Nations Environment Programme Finance Initiative

published the Global ESG Real Estate Investment Survey Results.

Respondents of the survey, which was conducted between

September 2018 and February 2019, collectively represent over

US $1 trillion of assets under management.

The survey found that 93% of respondents include ESG criteria

in investment decisions. Survey results indicated that 68% of

respondents have a real estate investment strategy in place that

considers GHG emissions of potential acquisitions – 100% of

respondents from the Asia-Pacific region, 72% from Europe and

47% from North America.

Across all regions, 95% stated that they contribute to or support

sustainability benchmarking at the portfolio and operational levels

and assess performance results.

The majority of respondents are highly motivated to use ESG

criteria in investments because of:

- Lowered risk

- Increased investor demand for sustainability disclosure

- Increased tenant demand for green buildings

“Every owner and investor should have an ESG strategy. There

are four reasons. First, the business case is incontrovertible.

Second, the expectations from stakeholders, including investors

and tenants, will only increase. Third, the pressure from regulators

and government will continue to rise. Lastly, it’s the right thing

for all corporations to do for their brand, their communities, and

their continuing social license,” said Michael Brooks, the CEO of

REALPAC.

More money is chasing real estate today than any other time

in history.

This has been an unprecedented period of fundraising that has

pushed dry powder to a new high of US $1.54 T as of the end

of June 2019, meaning that many investors have significant

commitments yet to be deployed, Prequin reports in their Private

Equity and Venture Capital Quarterly report.

Meyers Research Managing Director, Steve LaTerra, has seen

money targeting real estate more than double since 2012. The

amount of dry powder has been steadily increasing since 2014.

More money is chasing real estate opportunities today than at any

time in history.

REIT balance sheets are now so strong, according to NAREIT, that

in 2018, despite two corrections, REITs managed to raise equity

capital 110 times totalling US $41.84 B. All this capital was raised

during a year where there was a trade war escalation, four US rate

hikes and growing recession fears.

In NREI’s fourth annual research survey exploring the state of

publicly-traded REITs, respondents continue to have a stable

assessment of capital markets for REITs. Roughly two-fifths of

respondents said the availability of both equity (39%) and debt

(40%) is unchanged from a year ago. But three in 10 respondents

said equity (30%) and debt (31%) are more widely available. Those

figures rose about 10 percentage points from how respondents

answered in 2018. Only about one in 10 respondents (13% for

equity, 12% for debt) said capital was less available than a year ago.

Blackstone Group is tripling its fundraising goal for the real estate

investment trust it started last year.

The company said in its initial filing with the US SEC that it planned

to raise US $5 B for Blackstone Real Estate Income Trust but now

says it will raise an additional $10 B on top of this, according to the

Wall Street Journal.

Brookfield Asset Management closed one of its latest global private

real estate fund, Brookfield Strategic Real Estate Partners III

(BSREP III). With total equity commitments of US $15 B, BSREP

III is Brookfield’s largest private fund to date and will focus on

acquiring high-quality real estate assets on a value basis.

BSREP III significantly exceeded its original fundraising target of

$10 B, reflecting strong investor demand.

As part of Deloitte’s 2019 Commercial Real Estate Outlook, 500

global investors were surveyed, 97% of survey respondents

planned to increase their capital commitment to CRE over the next

18 months. Respondents from the United States plan to increase

their capital commitments by 13% in this time frame, while those in

Germany (13%) and Canada (12%) show similar levels of interest.

Figuring out how to deploy capital will be a major theme in 2019.

Several capital market experts said they expect the volume of capital

placements to be about the same as 2018 although there may be

changes in how or where funds are deployed, such as a move away

from big cities on the coasts and into secondary markets.

While some investors are exploring secondary markets in search

of yield, others remain in the major markets where there is more

stability and demographics work in their favour.

As commercial real estate values reach all-time highs in the

nation’s top-tier cities and cap rates get squeezed, secondary

markets with strong economic fundamentals are attracting investor

interest.

“Yield is king and yield is now being found in less-usual suspects,”

Spencer Levy, Americas Head of Research at CBRE, told the

Financial Post. “Some of the usual suspect central business district

markets are later in the cycle, and so some of the capital is now

flowing to other smaller markets to get this yield.”

The yield on assets in secondary markets can be anywhere from

75 basis points to as much as 100 basis points wider, depending

on the market and the product type, according to Chris Ludeman,

Global President of Capital Markets at CBRE. Good property

fundamentals, strong economies and smaller equity requirements

allow investors a broader field of play, Ludeman says.

In Canada, there has been a recent exit out of secondary markets

with RioCan divesting out of secondary markets with plans to sell

100 of its properties. Allied REIT also exited out of the Victoria,

Winnipeg & Quebec City markets to focus their operations in

Canada’s largest cities.

In Q1, BTB REIT acquired two office buildings in Laval, Quebec

for $25.3 M. The REIT is exiting secondary markets in order

to concentrate on the Greater Montreal, Quebec City and

Ottawa areas. BTB recently sold properties in Sherbrooke and

Drummondville, Quebec and it is planning to sell four more

properties in smaller markets.

However, Northview Apartment REIT has opted to expand into

secondary markets, such as in the north and Atlantic regions

of the country.

The secondary markets that Northview targets have significantly

lower upfront prices, particularly when compared to the current

rates on offer in the larger metro areas across the country. Lower

competition in those secondary markets translates into higher

occupancy rates for the company. Northview owns over 27,000

units that are scattered across eight provinces and two territories.

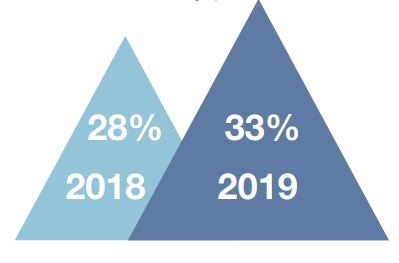

According to CBRE’s 2019 Investor Sentiments Survey,

investor’s appetite for ‘good secondary market’ showed

an increase to 33% from 28% the year before. The share of

sovereign wealth funds, insurance companies and pension funds

that now want to invest in secondary markets has risen from 25%

to 52%.

Colliers International noted in its 2018 property outlook that sales

and leasing volumes have been shifting (and will continue to

shift) to secondary locations due to decreasing availability and

progressively pricier rents in the primary markets.

Another reason for the increased interest in secondary markets is

the cost of housing in primary markets. According to PwC’s 2018

Emerging Trends report, there is pressure for tenants to hire talent

in a tight labour market. Millennials make up one-third of this talent

and are starting to settle down and start families. The proximity

to affordable housing is becoming more important and is in short

supply in the primary markets.

JLL’s Lauro Ferroni, Director of Research reported that there was

an increase of investment activity back into primary markets in

2018 following three consecutive years of decline.

Investors, he says, are looking for the security of an income

stream coupled with high-quality assets that will be best-positioned

to go through different economic cycles. The performance of the

commercial real estate sector over the next several quarters will

dictate whether this will turn into a trend, he notes.

New trends, new brands, the expansion of established brands

and untapped development potential all providing opportunities for

REITs.

Major Canadian retail REITs will be increasingly focusing on

redevelopment activities to maintain growth in the future, according

to research by Ryerson University’s Dr. Maurice Yeates and Dr.

Tony Hernandez.

The same applies to the US. For several high-productivity retail

REITs, particularly Simon, Regency and Taubman, redevelopment

remains a substantial source of untapped long-term value. Toptier retail assets are ideal for the “live-work-play” mixed-use

residential expansion, and there are a handful of highly successful

redevelopments from these three higher-productivity REITs.

High-productivity mall REITs continue to find accretive yields in

redeveloping vacated department store space into higher-value

mixed uses, including multifamily and experience-based retailers.

In Canada, while e-commerce is certainly impacting the retail

sector, its negative ramifications are less pronounced than in the

US.

The 2019 Summer Shopping Habits Survey and 2019 Summer

Dining Habits Survey, developed by Lightspeed, found that

physical retail is still the most prevalent form of shopping for

Canadians at 47% and Americans at 36%.

There are a number of retailers expanding into the Canadian

market: UK brand Cath Kidston, Korean beauty brand Innisfree,

Dutch discounter Hema and France’s ba&sh. As well, there are

Canadian brands that are expanding: Bad Boy, Giant Tiger and

SPINCO.

Digitally native brands are making their mark on the brick-andmortar landscape. Collectively they are set to open 850 stores in

the next five years, according to an Online Retailers Report by JLL.

Research firm Coresight projects up to 12,000 closings by yearend, primarily concentrated in the mall segment.

As of June, US retailers have announced 6,986 store closures and

2,985 store openings. This compares to 5,864 closures and 3,251

openings for the full year 2018.

The bifurcation between top-tier and lower-tier retail REITs

continues to widen as retailers focus investments into the highest

productivity locations. Downsizing retailers have focused their

investment into higher-performing stores and have continued

to close weaker-performing stores in lower-tier malls and retail

centers. 2017 saw an unusual surge in the rate of store closings,

but total closings dropped 20% in 2018 before reaccelerating yet

again in the early part of 2019. Lower-productivity mall REITs are

in a continual fight for survival and funding concerns are expected

to be lingering issues for the foreseeable future, Daily Forex Times

reports.

Retail keeps evolving despite these headwinds.

In keeping with the Space-as-a-Service trend, PropTech

startups Fourpost and BrandBox are transforming the traditional

retail model by adapting the SPaaS model to retail through

“brandboxing.”

Brandboxing is a full-service approach that enables smaller online

brands to open and operate stores in malls. Prefabricated spaces

available for shorter lease terms and lower rents make it easier

for online merchants to scale and test the success of the brick and

mortar stores without having to obtain a permanent location.

Fourpost has already launched studio shops in the Mall of America

and West Edmonton Mall. Macerich announced the launch of

Brandbox in Tysons Corner Center in Virginia this last November.

To start, Tysons Corner housed six brands with space ranges

from 550 to 2,500 sq. ft. at the property with six to 12-month lease

agreements.

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.