Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the content of the Montreal real estate market, click the following Insights.

The Montréal has been the recipient of billions of dollars in investment to improve transportation infrastructure.

In December, Canada Infrastructure Bank announced that it is committing up to $300 M in financing to the Port of Montréal’s new container terminal in Contrecoeur.

Construction, which is scheduled to begin in 2021, could cost as much as $1 B and is expected to create as many as 5,000 jobs during the construction phase.

According to the port authority, the new terminal will add about 1,200 trucks a day to local traffic and two or three ships a week on the St. Lawrence River at the outset, and much more if the terminal reaches full capacity.

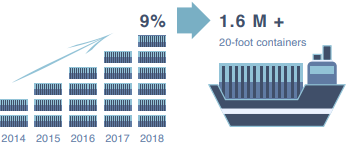

According to the port authority, freight traffic at Canada’s secondlargest port rose 9% in 2018 to the equivalent of more than 1.6 M 20-foot containers for the fifth straight year of record volumes, prompting concerns the docks will be overloaded by 2022. The Contrecoeur terminal would add capacity of 1.15 M containers.

Canadian Pacific has announced a new multi-modal transload terminal to be built at their Cote St. Luc railyard.

The new CP terminal will enable transportation and distribution services to East Coast urban centers not directly served by rail.

The terminal will be built by Canadian Pacific in multiple phases and operated by TYT, a Québec -based freight transportation service provider. The first phase is the construction, by CP, of a new 118,000 sq. ft. rail-served facility that is designed to assist in the receiving, unloading, carrying and delivery of rail traffic. Phase 1 is currently scheduled to be completed in June 2020.

John Brooks, CP Executive Vice-President and Chief Marketing Officer stated: “….this project enhances our footprint in the Montréal area by building capacity and expanding our ability to provide customers with value beyond rail, through trucking and transload services.”The Réseau Express Métropolitain (REM) is the 67-kilometre, $6.3 B light rail project is the single largest transit project in Montréal in half a century.

Conceived, planned and costed by the Province of Québec ’s institutional investor, the Caisse de dépot et placement du Québec (CDPQ), the REM is currently under construction. The first trains will begin running from the South Shore to Bonaventure station in 2021, and the entire network is scheduled for completion by 2023.

Once completed, it is supposed to provide high-frequency, intermediate-volume light-rail service on a regional level: connecting suburbs with the city centre along three axes and linking Montréal’s central business district with its international airport.

Last summer, the federal government made an investment of more than $1.3 B to extend the Montréal Metro’s Blue line. Slated for completion by 2026, the Blue line will include five new stops eastbound, covering an additional 6 km, with the final stop near the corner of Bélanger Street and Boulevard des Galeries d’Anjou.

The project will cost an estimated $4.5 B which will also include the construction of two bus terminals, a park-and-ride lot with 1,200 spots and a pedestrian tunnel that will connect to the future bus rapid transit system (BRT) on Pie-IX Boulevard.

In Q3 2019, the federal government made an investment of $50 M to improve air freight and logistics at the International Aerocity of Mirabel (YMX).

Work will include refurbishing and extending the main apron to a cargo apron, improving road access, increase aircraft parking capacity, and building 215,000 sq. ft. of warehouse space.

Absorption of over 3 M sq. ft. of office space the highest rate in almost 20 years.

Total office space absorption reached 3.1 M sq. ft. in 2019, JLL reported. This was the highest absorption rate since 2000 with nearly 3.5 times more leasing momentum than the ten-year historical average.

According to Altus Group, office vacancy in Greater Montréal has decreased from 11.5% in Q1 2019 down to 9.4% in Q1 2020, the lowest it has been since 2013. There were no completions in the first quarter, however 2019 had a total of almost 960,000 sq. ft. completed. For new supply coming to market, the first quarter had about 3.9 M sq. ft. under construction at an availability rate of 45.7% with almost 2.1 M sq. ft. preleased. The downtown market, alone had 1.5 M sq. ft. under construction with an availability rate of 30.3%.

Montréal has increasingly become an international tech hub with tech firms, especially gaming companies, increasing their presence in the city.

Montréal has more than 140 studios, making it the most significant video game production hub in Canada and one of the largest in the world.

At the end of 2019, Colliers reported that the technology industry occupied 7.9% of office space in the GMA.

In Q4 2019, Ubisoft renewed its lease for about 500,000 sq. ft. at 5505 Saint-Laurent Boulevard. Google expanded its space by over 42,938 sq. ft. at 425 Viger Avenue.

Take Two Interactive and Momentum Games have each leased entire floors at Kevric’s 1100 Atwater Avenue development in Westmount.

Chicago-based, cyber security firm OneSpan has plans to invest $9 M to expand its Montréal office which will make it its largest office and R&D centre.

CBRE’s Québec Managing Director Avi Krispine said, “Strong office demand is being driven by an evolving tech sector, which is pushing average downtown Class A net rents to an all-time high of $24.57 per sq. ft.”

Speaking in CBRE’s Canadian market outlook webinar on April 14, OMERS President & Chief Pension Officer Blake Hutcheson stated that he is bullish on office, though he sees change coming to the sector.

“Rough math, there is probably 20% less demand for office space on a go-forward basis, but there’s probably a 10% net demand for more additional elbow room because we over-served the market by jamming too many people in on a per-square-foot basis,” he observed.

Pandemic will likely thin out a crowded field of

flexible office suppliers.

In the last five years, the flexible office workspace sector has exploded across Canada, quadrupling its footprint to 6.1 M sq. ft. according to new research by CBRE.

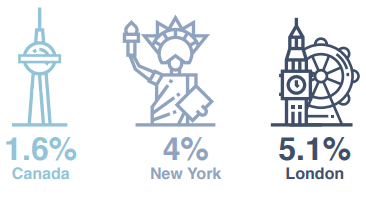

CBRE Canada Vice-Chairman Paul Morassutti said co-working, despite its major growth, still only accounts for 1.6% of Canada’s office inventory. This

under representation vis-à-vis other major centres (flexible office space accounts for 4% of office space in New York and 5.1% in London) is a positive thing as much of coworking space is sitting empty during this time.

In 2019, WeWork announced plans to expand its footprint in Montréal. Its first new location located at 1010 Rue Sainte-Catherine Ouest, will house approximately 2,000 desks across four floors. The second location, which WeWork has targeted to open during the second half of 2020, will be located at the Humaniti building. WeWork said the two new locations add over 3,000 members in Montréal, doubling its membership base in the city.

As of the beginning of 2020, WeWork’s expansion plans were still on track despite their failed IPO and the exit of the company’s co-founder and CEO Adam Neumann. However, in April, the Japanese tech firm SoftBank abandoned its US$3 B bailout of the company.

COVID-19 may also spell further trouble for WeWork. The company has at least US$47 B in lease liabilities worldwide. WeWork stopped paying rent in April on some of its United States locations to try to cut costs and hired JLL and Newmark Knight Frank to renegotiate its leases, the Wall Street Journal reported on April 8.

In a post virus environment, people will be less likely to share space the way they had been prior to the onset of COVID-19.

Bryan Murphy, CEO of flexible office space provider Breather, thinks that once work recommences, it will again favour flex office space.

“People might not want to share space as much after this like you do with traditional co-working spaces so we will likely see an uptick in demand for private offices,” Murphy said.

Flex space occupiers like Knotel, Industrious, Convene, and even WeWork have been growing their private office suite offerings for some time, so they have a hedge against the decrease in demand for traditional co-working spaces, Logan Nagel writes in Propmodo.

Alex Cohen, a real estate advisor with Compass in New York City, said that shared-office companies over-expanded in the largest markets in the last 24 months, particularly the fastest growing players. Even before the pandemic, there was a 50% vacancy rate at Knotel locations that opened in 2019, he said.

Some of the larger companies, including WeWork, were beginning to pivot their business model to rent to larger, established companies between six and 12 employees, rather than focusing on single entrepreneurs, Cohen said. However, even these leases were for 12 months or less.

Adam Henick, Co-Founder of Current Real Estate Advisors, states that, in order to survive, office-sharing companies will need to adjust the business model and continue their pivot toward attracting larger, more established businesses. If economic uncertainty affects hiring and growth plans, established companies might use shared office space to lower real estate costs.

Montréal has become the third tightest major industrial market after Toronto and Vancouver.

According to Altus Group, Montréal’s industrial market vacancy rate reached a 10-year low declining to to 1.8% in Q1 2020. In Q4 2019, the vacancy rate was at 2.2%, and 2.7% in Q1 2019.

There were two buildings that were completed in the first quarter representing a total of 433,560 sq. ft. In Point-Claire, a 295,610 sq. ft. CFC single tenant bulding was completed and fully leased by Sobey’s for its e-commerce brand Voilà, and will be an automated warehouse employing about 1500 workers upon completion. The warehouse and delivery network is expected to service the Quebec and the Ottawa area. In Terrebonne, a new 137,950 sq. ft. multi-tenant building was completed, with 100% availability. Four buildings under construction in Q1 2020 representing a total of almost 2.2 M sq. ft. and have already been fully leased.

The story for the industrial market has always revolved around the growth in e-commerce. This trend will continue, but at an accelerated pace, especially as it pertains to online grocery shopping, according to Altus Group. As a result of pandemic containment measures and the ensuing growth in demand for delivery services, grocery-related business has experienced a boom.

In Q4, 620,679 sq. ft. of industrial space was absorbed, bringing the total for the year to 4.2 M sq. ft. – the second highest absorption rate that the Montréal has had in one year, CBRE reports.

Near-zero industrial availability in Toronto and Vancouver markets has put pressure on the Montréal market. Much of the demand has been coming from technology, manufacturing, transportation, and logistics firms, reports CBRE Québec Managing Director Avi Krispine.

Robust demand to purchase industrial assets has led Montréal’s average asking sale price to climb for eight consecutive quarters, closing out the year at a record $111.24 per sq. ft. This represents a growth rate of 63.8% in two years.

Amazon has announced that it will open its first Québec fulfilment centre in Lachine. They plan to have it open in time for the 2020 holiday shopping season.

Montréal-based Metro Inc. has already been investing in automation since it announced a $400 million investment to modernize its Toronto distribution centres in 2017. Recently,Metro announced another $420 million investment in building and expanding its facilities in Quebec over five years. It plans to build a new 600,000 square foot fresh and frozen automated distributio centre, which will be located north of Montréal in Terrebonne, QC and expected to open by 2023. The investment also includes plans to expand an existing produce and dairy facility in Laval, QC to a 50,000 sq. ft. facility and expected to be completed by 2024.

Growing industrial demand is coming into conflict with municipalities that are focused on promoting mixed-use zoning in infill areas. In a fourth quarter 2019 report, JLL stated that despite the large supply pipeline at the moment, available land remains limited and this will continue to drive price appreciation in the medium term.

Investment volumes were up significantly in 2019 as institutional investors and REITs chased yield and solid market fundaments.

In 2019, Montréal investment transactions rose by 9% to 1,424 deals and total investment volume moved up by 35% to $8.8 B compared to the previous, Altus Group reports.

The office sector recorded the second highest transaction volume in 2019 reaching almost $2.1 B compared to about $800 M in 2018. Montréal’s office market also had third highest investment volume across the country, behind Toronto and Vancouver.

The top office transaction in Montréal was 1250 René-Lévesque Boulevard West. BentallGreenOak acquired the 47-storey, class-AAA office tower with 1,036,193 sq. ft. of space, from Oxford Properties Group and PSP Investments in May, for $605 M. It was the largest single-asset transaction BentallGreenOak has made in Canada to date.

At the end of December, Place du Canada located at 1010 de la Gauchetière Street West was acquired by Crestpoint (97%) & Redbourne (3%) for $105.5 M representing a price per sq. ft. of $275.

The 22-storey class B office building was constructed in 1968. The building contains a total net leasable area of 384,000 sq. ft. and was 70% occupied at the time of sale. The seller was Crédit Suisse.

Allied Properties REIT closed its acquisition of 700 De La Gauchetiere West from Dream Office REIT during Q3 2019. The 28 storey class A office building was bought for $322.5 M. The building built in 1983, contains a gross leasable area of 935,966 sq. ft. and has a direct access to Square Victoria Metro.

In Q3 2019, Allied Properties REIT bought the Class I RCA Building at 1001 Lenoir Street for $80 M which included 107,000,sq. ft. of extra land.

With the purchase of 747 Du Square Victoria for $276 M in Q1 2020, Allied Properties REIT now has the largest office inventory of any company in the GMA. According to Colliers, Allied owns just under 2 M sq. ft. of office space in the Old Montréal Market representing 21% of market share.

The National Bank sold its headquarters at 600 de la Gauchetière Street West for $187 M to Kevric. The building was built as National Bank’s Headquarters in 1983 which the company will vacate the once its new headquarters is complete in 2022. Altus Group reports that Kevric has a $50 M redevelopment plan that will see the building repositioned.

1100 & 1150 René-Lévesque Boulevard West sold for $225 M in January 2020 to Groupe Petra and Groupe Mach.

The property is improved with one 26-storey, class A, office building constructed circa 1986. The building contains a total net rentable area of 565,170 sq. ft., with 7,903 sq. ft. of ground floor retail space and a typical floor plate of approximately 23,000 sq. ft.

The multifamily sector was the top performing sector in 2019 with transaction volume close to $2.7 B, an increase by nearly $500 M from 2018, Altus Group reports.

Globe Capital Management purchased Les Berges du Canal for $60 M in Q1 2020, a new 6-floor building project built out of concrete, just in front of Canal Lachine. This was Globe’s 11th purchase in Montréal since it first started buying concrete apartment high-rises in 2005. The 168-unit apartment was built in 2012.

Phases 3 and 4 of EQ8 on Newman Boulevard was bought by Manulife Investment Management for $105 M in January 2020. The newly constructed buildings contained a total of 300 units.

Minto Apartment REIT participated in the acquisition of over a half billion dollars in multifamily product in 2019.

In Q2 2019, Minto Apartment REIT and Investors Group acquired Le Rockhill from Ivanhoé Cambridge for $268 M. Constructed in 1967, Rockhill comprises six buildings on approximately 7.6 acres at 4850-4874 Côte-des-Neiges Road in Montréal. The 1,004 suites average approximately 777 sq. ft. per suite, with an average monthly rent of $1,352.

In Q4 2019, Minto Apartment REIT acquired two properties from QuadReal in for $281.8 M.

• Le 4300 is a 12-storey premium building originally built in two phases in 1957 and 1962, located on 3.1 acres at 4300 de Maisonneuve Blvd. W. in Westmount. It contains 318 large suites with an average size of approximately 1,260 sq. ft. and average monthly rent of $2,667 per suite.

• Constructed in 1928, Haddon Hall consists of 10 six- and sevenstorey buildings on 3.2 acres on Sherbrooke Street West. The buildings have an aggregate of 210 large units, with an average suite size of approximately 1,200 sq. ft. and average monthly rent of $1,882 per suite.

“When we launched Minto Apartment REIT last year, one of our objectives was to build a strong presence in the Montréal market. This acquisition, combined with our purchase of the Rockhill property in May, clearly achieves this goal,” said Michael Waters, Chief Executive Officer, in an October release.

CAPREIT acquired Rez Boisbriand 1065 Des Francs-Bourgeois Street from Réseau Sélection for

$33.3 M - a seven-storey apartment building containing 121 units.

BentallGreenOak acquired Appartements-Boutique from developerLe groupe Prevel for $96.6 M. The newly completed complex includes 243 residential units across two buildings along with 10,714 sq. ft. of ground-level retail and 10,964 sq. ft. of office space. Amenities include conference rooms, fitness areas, rooftop patios and pools.

Interrent REIT picked up two GMA properties for $132 M. The portfolio contains a total of 544 residential units, La Tour LaFontaine (1023-1025 Sherbrooke Street East, 251 units), and La Nouveau Colisée (205 -235 Sherbrooke Street West, 297 units).

The retail sector was the second most active market after Toronto performing fairly well in 2019 reaching $1.3 B in transaction volume, up by 26% from the previous year.

Canada’s largest enclosed mall sale for the year was Ivanhoé Cambridge and CPPIB’s joint venture sale of Carrefour de l’Estrie in Sherbrooke to Groupe Mach for $236M at a 7.34% cap rate.

Firm Capital Property Trust acquired a 50% non-managing interest in six primarily grocery anchored shopping centres located in Ontario and Québec from First Capital REIT. The acquisition price for 100% of the portfolio was approximately $266 M.

Summit Industrial Income REIT sold a data centre in Ville-Marie for $106 M to AIMCO.

In September 2019, Pure Industrial Real Estate purchased an 11-property industrial portfolio in the Greater Montréal Area from Healthcare of Ontario Pension Plan (HOOPP) for $259 M. The portfolio contains a gross leasable area of 1,533,924 sq. ft., representing an aggregate price per square foot of $169.

The acquisition, which was one of the biggest industrial real estate transactions this year and the largest in Montréal’s history, includes warehouses, distribution centres and logistics buildings.

In February 2020, PIRET picked up 666 Saint-Martin Boulevard West, a multi-tenant industrial property in Laval, from Manulife for $28.1 M.

Vigorous demand for space across sectors has resulted in increased development across the city.

In Laval, ground broke last June on the $450 M Espace Montmorency – the largest ever mixed-use development in Laval. The project, which is a JV between Group Montoni, Groupe Sélection and the Fonds immobilier de solidarité FTQ will contain a total of 1.36 M sq. ft. and will be directly connected to the Montmorency metro station.

Espace Montmorency will include a 16-storey, 350,000 sq. ft. office building, a 180-room hotel and conference centre, 700 residential in two towers, 150,000 sq. ft. of commercial space, 1,400 underground parking spaces and 50,000 sq. ft. of public green spaces.

Broccolini is involved in more than $1.5 B worth of projects under construction in downtown Montréal including:

• National Bank’s new 40-storeys, 1 M sq. ft. headquarters located at 800 Saint-Jacques

• Victoria sur le Parc, a 58-storey, 400-unit luxury condominium. The project includes a mixed-use podium, known as the 700 St. Jacques, which will house commercial and office space. The nine-storey podium will offer 330,000 sq. ft. of leasable space.

• 628 Saint-Jacques, a 258 unit 35 storey luxury condominium

• Maison de Radio-Canada at 1500-1700 René Lévesque Blvd. E., will be delivered in 2020. Radio-Canada will be the major tenant of the fully leased, 418,000 sq. ft. building.

Carbonleo’s Royalmount development has undergone a significant revision. The new plan calls for a significantly reduced commercial component and adds 4,500 new residential units.

Gare Viger, at 530 Saint Hubert St., is slated to be complete in 2020. The eight-storey, 147,000 sq. ft., multi-tenant building is being developed by Jesta Group.

7240 Waverly is a six-storey, 118,259 sq. ft. building to be delivered next year as a purpose-built co-working space for Fabrik8.

Brivia launched 1 Square Phillips last September. The 61-storey, 789-unit residential building which will be the tallest residential tower in Montréal, is the first of three phases in this development.

Brivia plans to start construction in 2020 and anticipates first occupancies in 2024. Construction costs for the first tower are estimated at $400 M.

Karen Groulx, Fraser Mackinnon Blair, and Dragana Bukejlovic, members of Dentons’ Construction group , write that the potential impacts of COVID-19 on the construction industry could be the delay of projects resulting from labour disruptions, critical supply chain disruptions, a delay or inability to obtain required permits and unforeseen events impacting the availability of financing.

As of the end of March, construction sites were closed in Québec, with the exception of sites that are expanding the capacity of the province’s healthcare system, or that are related to dispatch,

security and emergency services and rental equipment.

Home building was added to the list of essential services on April 13, specifically the work necessary to complete the delivery of residential units scheduled for July 31. The goal is for those affected to be able to move into their new homes as quickly as possible, while also easing pressure on the rental market.

Premier Francois Legault, who had extended the order for nonessential services to be shut down until May 4 suggested mid-April

that key sectors, including construction, could open sooner.

Disruption to the retail sector continues as the pandemic

sweeps across the globe.

Since the start of the pandemic consumers are moving to

e-commerce far more than ever before, said George Minakakis

CEO of the Inception Retail Group.

Almost 3 in 10 people are shopping for things online that they

normally would have bought in-store, according to a survey of

more than 30,000 Canadians by Chicago-based market research

firm Numerator.

The online shopping surge due to the ongoing COVID-19

pandemic is driving Amazon to hire on another 75,000 employees

less than a month after it announced it was hiring on 100,000

workers. They are so backed up that shipping times have

increased to a month for non-essential items.

Brands not already online have quickly tried to catch up.

Montréal-based etail21, an online B2B marketplace that connects

retailers, influencers, and brands to facilitate sales in the retail

industry, has launched a new initiative to help retailers have their

own fully-connected, free e-shop during the challenging times

presented by the COVID-19 pandemic, according to RealInsider.

BNN Bloomberg reports that Shopify stock prices have increased

to record levels as of mid-April after its Chief Technology Officer

Jean-Michel Lemieux said in a tweet that the Ottawa-based

company was handling “Black Friday level traffic every day” as it

brings “thousands” of businesses online.

Uber announced in mid-April that it is introducing two new types of

services - Uber Direct and Uber Connect. Uber Direct is a delivery

platform for retail items, while Uber Connect is a peer-to-peer

package delivery service, for sending goods to family and friends.

“This marks the most aggressive foray yet for Uber into courier

services, after it already introduced grocery items to its Uber Eats

platform as the coronavirus pandemic continues to suppress its

ride-hailing business,” Darrell Etherington writes in Tech Crunch.

The pandemic is likely to stoke other existing trends. Simeon

Siegel, Managing Director at BMO Capital Markets, told Retail Dive

in an interview, “It would seem that the coronavirus is acceleratingthe structural changes we’ve been seeing across retail and

society for the last decade — toward online interaction, toward

e-commerce and away from brick and mortar, toward direct-toconsumer away from department store.”

After the pandemic eases, Thomai Serdari, a professor of luxury

marketing and branding at New York University’s Stern School

of Business, states that there is likely to be pent-up demand, but

possibly tempered by a new appreciation for consuming less,

especially as a recession bears down.

Doug Stephens, Founder and CEO of Retail Prophet predicts that the luxury goods market – one that had been flourishing prepandemic – will take a hit. “Count on the luxury vehicle market suffering. Count on the jewelry industry suffering. The luxury goods category in general at least in the near term is going to suffer,” he said. “Not only because the average person on the street is feeling insecure about their job but even high net worth individuals right now are watching their stock holdings decreasing by upwards of 30 to 40 percent. That’s going to put a significant dent in discretionary spending.”

Many large retail landlords are working with tenants who need

support because of the financial challenges brought on by the

outbreak.

Choice Properties REIT said it would grant 60-day rent deferrals

on a case-by-case basis for “qualifying” small businesses and

independent tenants.

“We understand and acknowledge the extraordinary financial

pressures on parts of our tenant base, especially on independent

and smaller businesses,” said Choice chairman Galen Weston in

a statement.

As May rents become due, government support is on its way.

It plans to introduce the Canada Emergency Commercial Rent

Assistance (CECRA) for small businesses.

The program will provide loans, including forgivable loans, to

commercial property owners who in turn will lower or forgo the

rent of small businesses for the months of April (retroactive), May,

and June.

The apartment sector expected to continue to perform well in

the face of COVID-19.

The vacancy rate decreased from 1.9% in 2018 reaching 1.5% in

2019, a 15-year low. Vacancy rates have now reached 1.6% on the

Island of Montréal and 1.2% in the suburbs.

The estimated change in average rent in the Montréal CMA was

3.6%, a more pronounced increase than in recent years according

to CMHC, and averaged $841.

Supply recorded another significant increase, as around 8,500 new

units were added to the rental stock over the last year. This was

around 1,000 more units than last year and was well above the

annual average from 2011 to 2014 which was about 1,600 units.

The condominium rental vacancy rate remained relatively stable,

settling at 1.8% in 2019. On the supply side, the number of rental

condominiums rose by 1,150 units, for an increase of 3%, CMHC

stated.

The average rent for two-bedroom condominiums in the CMA, at

$1,275, was significantly higher than the average rent for purposebuilt rental apartments with the same number of bedrooms ($855).

Altus Group’s Director of Innovation and Growth Strategies,

Vincent Shirley, pointed out that there has been a 37% increase in

the number of foreign students to Québec in the last five years. In

2018, there were 45,086 foreign students in the province.

Students are one of the key demand drivers for multifamily

residential. They also provide a fairly quick turnover for landlords,

who tend to stay between three and four years, stated James

Palladino, Managing Director of RBC Capital Markets Real Estate

Group in Montréal.

Marc Hétu, Vice-President of CBRE Limited in Montréal, said

the growth of tech talent in Montréal is helping to fuel a steady

increase in rents in the city as tech job salaries are significantly

higher than in other fields.

During an April 7th webinar hosted by Informa, Benjamin Tal,

Deputy Chief Economist at CIBC, stated that approximately 75%

of apartment tenants paid their rent in full in April. Citing estimates

calculated from surveys among landlord companies, he said that

another 10% paid half their rent and 15% did not pay their rent at all.

These numbers were better than anticipated but concerns remain

for the following months.

Without some sort of change to policies, the number of people

who do not pay their rent will be higher in May. Tal suggested

that provinces take example from the BC government which is

providing renters with up to $500 per month for six months. The

subsidy is being paid directly to the landlord.

Tal said that 450,000 immigrants won’t be coming to Canada over

the next six months to a year because of COVID-19 movement

restrictions.

This will hurt economic activity and reduce demand in the rental

housing market. The Deputy Chief Economist anticipates purposebuilt rental construction dropping over the next six months, but

rebounding strongly in one to two years.

Momentum continued into 2020 – March represented 61st

consecutive month of sales growth.

A record-breaking 51,329 properties were sold in the GMA in 2019

representing a 10% increase from 2018, according to Québec

Professional Association of Real Estate Brokers (QPAREB).

This marked the fifth consecutive annual increase of more than

5%. The transactions had a combined value of $20.3 B - 15% more

than in 2018.

Last year, there was a 19% decrease in the number of listings from

the year before.

QPAREB cites full employment, rising disposable income, low

interest rates, positive migratory flows and government incentives

for home ownership as contributing factors to the growth in realestate demand.

The association states that non-residents now account for about

15% of all residential transactions in the downtown core.

5,907 residential sales transactions were concluded in March

2020, a 4% increase compared to March 2019. Despite the slowing

pace, this was the 61st consecutive month of sales growth. For the

first quarter of the year, 14,662 transactions were concluded in the

Montréal CMA, a 13% increase compared to Q1 2019.

Montréal’s housing starts have remained stable over the last three

years to hover around the 25,000 mark.

The aggregate price of a home in Canada climbed 4.4% year-overyear in Q1 2020. In December 2019, Royal LePage had forecasted

an increase of 3.2% by the end of 2020, but expected growth rates

have had to be revised due to the COVID-19 pandemic.

According to Royal LePage, Greater Montréal aggregate home prices in the first quarter of 2020 were $441,979 (up 7.2% yearover-year). Condo prices climbed 5% to reach $344,962.

The real estate services firm modelled two different scenarios:

If business resumes by the end of June, the aggregate home price

is expected to reach $434,500 (down 0.5% year-over-year) by the

end of 2020.

If business activity resumes in late summer 2020, the aggregate

home price is expected to reach $421,400 (down 3.5% year-overyear) by the end of 2020.

This forecast factors in that Québec is the only province where real estate brokerage is currently not included in the list of essential services, Royal Lepage noted.

New REM stations are resulting in millions of dollars worth of

new commercial and residential construction underway in the

West Island submarket.

By the time the new REM is complete in 2023, six stations will

serve the West Island: Des Sources, Fairview-Pointe-Claire,

Kirkland, L’Anse-à-l’Orme, Sunnybrooke and Pierrefonds-Roxboro.

The construction of the new stations has precipitated a number of

new large-scale developments.

In Pointe-Claire, Cadillac Fairview has partnered with Ivanhoé

Cambridge for the development of the 50 acres of vacant

land Cadillac Fairview purchased in 2013, which is next to CF

Fairview Pointe-Claire. The mixed-use development is planned

for the site which will include residential, office, commercial and

entertainment uses.

A REM light-rail station will be located along Fairview Avenue and

with a bus terminal already in place at the mall, the project will

become a good example of a transit-oriented development.

CF Fairview Pointe-Claire is undergoing a $30 M renovation. As

well, a new Simons store will take over two floors of what was once

a three-storey, 180,000 sq. ft. Sears store. The remaining floor will

become a new food hall that will include signature restaurants.

Also in Pointe-Claire, Capcium, a manufacturer of softgel products

has partnered with Aurora Cannabis and will be constructing a new

state-of-the-art facility at 7300 TransCanada Highway.

As mentioned, construction is underway on a $95 M, 285,000 sq.

ft. Sobey’s Customer Fulfillment Centre in Pointe-Claire, that, once

complete, will employ upwards of 1,500 people.

In Lachine, Dollarama is expanding its distribution operations with

a new 270,000 sq. ft. facility that will include 27 loading docks.

Amazon has announced that they will open their first Québec fulfilment centre in also in Lachine, and they plan to have it open in time for the 2020 holiday shopping season.

Development company Les Développement Lachine Est is

transforming former industrial lands in Lachine into a $1B housing

development. The VillaNova project will contain 4,000 housing

units, ranging from townhouses and duplexes to multi-storey condo

towers and will be developed over the next 10 years. It will be built

on the sites of the former Jenkins Valves Factory and Dominion

Bridge Factory along the Lachine Canal. The 52-acre site required

significant soil decontamination.

In Dorval, the North American Development Group recently

bought the Dorval Gardens shopping centre and the adjoining

property. The company has plans to transform the space into a

new residential development that includes the construction of

approximately 950 residential units in six apartment and condo

towers ranging in between 12 and 16 storeys. Sylvain Forté, VicePresident of Québec Development for NADG, said the project will

be a mix of rental apartments and condos.

The $350 M project also includes about 38,000 sq. ft. of

commercial space and a hotel will be built on Dorval Avenue.

The City of Kirkland has several projects in the work for the

coming year, with one of the biggest being the eventual residential

development on the Merck Frosst property.

Kirkland, the Montréal Gazette reports, hosted a roundtable in

November that almost 90 residents attended. The purpose of the

session was to put together a potential vision for the future of the

former Merck campus, which is currently zoned industrial. In 2016,

plans for an 800-unit residential development failed.

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.