Real Insights feature curated content from industry leaders during the program formation of the Real Estate Forums and Conferences. Each report features on the Top 10 Real Insights focused on major trends. For more details on the content of the RealCapital Conference, click the following Insights.

Strong labour markets and modest growth in consumer spending, along with better prospects in the energy sector, will help to propel Canada’s economy in 2020.

After increasing by 1.6% in 2019, the Canadian economy is expected to grow by 1.8% in 2020 as energy investment turns around and consumer spending picks up, the Business Development Bank predicts.

RBC forecasts that, for the second year in a row, provincial economies will grow in 2020—something that hasn’t happened since 2010-2011. Most provinces will see modest gains with Western Canada recording some of the stronger advances due toeasing pressure in the energy sector.

The Conference Board of Canada predicts that Alberta’s economy will rebound by 2.4% next year and 3.1% in 2021. The Conference Board credited the bump to the Trans Mountain pipeline expansion on which construction has commenced, money coming in to build LNG Canada and a forecasted turn around in energy investment.

However other experts consider this estimate ‘bullish’. Edmonton’s chief economist John Rose forecasts a more modest increase of around 1.5% in 2020 and then moving up to slightly above 2% in 2021. Quebec’s economy grew the fastest of all the provinces in 2019, but will slow next year as weaker population growth impacts household spending gains, the Conference Board predicts. It stated that “Ontario is in the midst of a period of modest economic growth as residential investment and consumer spending cools and slowing global growth is restraining its export prospects”. RBC estimates that Ontario will grow at 1.6% rate in 2020, 10 basis points lower than in 2019 while Quebec’s growth will slow to 2.0% from 2.5% last year.

RBC expects that Prince Edward Island and Nova Scotia will extend export gains made in 2019 when some of their food producers took advantage of the trade dispute between the US and China. Stronger population growth will continue to be a positive factor. At 2.0% for each of the following years, RBC’s growth forecast has PEI ranking second in the country in 2020 and third in 2021.

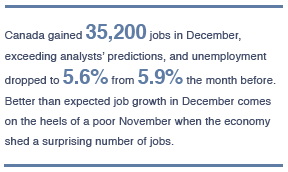

In November the economy shed 71,200 jobs which came as a surprise as economists on average had expected a gain of 10,000 jobs and the unemployment rate to hold steady at 5.5%, according to financial markets data firm Refinitiv.

All told, last year was one of Canada’s top years for job creation since the global recession. Roughly 320,000 jobs were created in 2019, the second-largest annual gain since 2007.

This has led to two important side effects—a boost in the labour force participation rate, and accelerating wage growth. In fact, in December, average hourly wages grew 3.6% from a year earlier, slowing from November’s 4.5% pace.

StatsCan said the consumer price index rose 2.2% compared with a year ago to end a three-month streak where the annual pace of inflation had held steady at 1.9%.

The increase in the pace of inflation compared with October came as energy prices in November posted their first year-over-year increase since April. Energy prices climbed 1.5% compared with ayear ago compared with a decline of 2.9% in October.

In early December, the Bank of Canada said that it “continues to expect inflation to track close to the 2% target over the next two years.”

The dollar began to rise after the recent inflation numbers and the loonie was one of the developed world’s powerhouse currencies in 2019, beating out the US dollar by 5%.

Interest rates are expected to hold steady in 2020 according to some experts who cite the following reasons: a strong job market, increased household spending, a rebound in the energy sector and increasing housing prices. With the Canadian inflation on target at the bank’s 2% level, the economy remains close to full capacity.

Despite lower investment volumes in 2019, investors still bullish on certain sectors and marketplaces.

Though final numbers are not yet available, the overall volume of investment activity decreased across Canada during 2019.

At the end of Q3, Altus reports that national investment volume year-to-date fell by 16% to $34.6 B compared to the same period last year.

According to Altus Group’s Investment Trends Survey in Q4 2019, Vancouver and Toronto remained the top preferred markets on the buy/sell momentum barometer, while all other markets displayed downward momentum.

The industrial asset class remained a top asset class in the first three quarters of 2019 at $6.6 B, following record-high annual transaction volume of $8.68 B in 2018, stated by Altus Group. The national availability rate hit an 11-year low of just 2.8% during the first half of 2019, according to Altus Group.

In 2020, sales activity is expected to remain strong. There is not enough industrial space in Canada’s big cities to meet demand.

Altus Data Solutions reports that industrial investment exceeded $1 B in the GTA in Q3 2019.

The office market, driven largely by Canada’s expanding tech industry, continued at a strong investment pace in 2019 while downtown rents continued to rise. There was a total of $6 B in office deals over the first three quarters of 2019, a slight decrease from the same period last year, according to Altus Group. The national office vacancy rate was at 9.6% at the end of 2019.

Vancouver and Toronto now have the two lowest downtown office vacancies in all of North America.

The largest office deal of 2019 was the acquisition of the Bentall Centre office complex by US buyers Hudson Pacific Properties with Blackstone Partners for $1.07 B. China’s Anbang Insurance Group had owned the four-building, 1.45 M sq. ft. complex since 2016.

According to Altus Group, total investment volume for the multifamily sector approached nearly $5.6 B at the end of Q3 2019, down from $7 B in the same period last year. Toronto and Montréal had the strongest investment volume activity from Q1-Q3 2019 in this sector, with total volume recorded at $3.8 B, followed by Montréal at $1.9 B. The $1.7 B apartment acquisition by Starlight which closed in December will put apartment investment number sover the top for 2019.

In fact, the largest investment transaction of 2019 was the Continuum REIT – Starlight Investments Ontario Apartment Portfolio, consisting of 44 properties in Ontario. The portfolio was purchased for approximately $1.732 B and contains a total of 6,271 residential units, representing an aggregate price per unit of $276,116, Altus reports.

Transwestern and Devencore teamed up to solicit insight from their commercial real estate advisory teams across 43 North American offices and produced their 2020 Commercial Real Estate Market Sentiment Survey. Roughly 70% of respondents expect Canadian office investment interest and pricing to rise in 2020, with half ofthe respondents expecting cap rates to remain flat. In the Industrial sector, half expect development levels to remain flat, given limited available developable land in prime areas and 86% of respondents expect higher investment interest in 2020, with pricing remaining steady to slightly increasing.

“Canadian commercial real estate markets also are expected to perform well in 2020, with mild concerns stemming from political and trade impacts as well as rising construction costs,” said Jean Laurin, President and CEO of Devencore. “Our economy is healthy and job growth is steady. With the exception of certain regions, major Canadian provinces like Ontario, British Columbia and Quebec all show robust conditions.”

From a global perspective, the top 50 global investors collectively added US $35.4 B of commercial real estate assets to their portfolios last year.

According to Real Capital Analytics, the pace of what the top 50 investors sold slowed from 2018. These investors were involved in dispositions totalling US $120.9 B in 2019 versus US $140.4 B in 2018.

Acquisitions fell from US $216.7 B in 2018 to US $156.4 B in 2019. On a net basis, this group of investors bought US $35.4 B more than they sold.

Stripping out the impact of Blackstone, however, net investment increased by only US $8.6 B for the year.

Blackstone had an outsized impact on the industrial markets in 2019. Its acquisition of a portfolio of industrial assets from GLP was the largest non-M&A type acquisition recorded for the sector. Even without the Blackstone activity, however, this group of investors was still hungry for industrial assets globally in 2019. Acquisitions of industrial properties by all groups but Blackstone exceeded the sale of assets by US $16.2 B.

For this group of top 50 global investors, the industrial sector was clearly a preferred sector in 2019, writes Jim Costello, senior vice president of RCA. Meanwhile, the appetite for investment in the office and retail sectors fell. The net investment was negative US $8.4 B for the office market globally and negative US $3.3 B for the retail market.

Many lenders looking to increase their allocation for real estate assets in 2020.

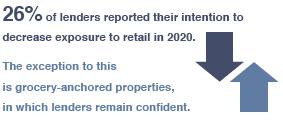

Though the break neck pace of loan book growth moderated in 2019, lenders directing additional capital to the real estate sector will direct 10-20% net new capital next year. For the few lenders looking to decrease their real estate exposures, it is mostly isolated to retail or land asset classes, where 26.1% and 15.2% of respondents respectively signalled an intention to decrease exposure. These are the findings of the recently released CBRE Canadian Real Estate Lenders’ Report.

Lenders expressed a strong desire to support transactions in gateway markets like Toronto, Ottawa, Vancouver and Montreal. Ottawa rose in the rankings to displace Vancouver as the second-most desirable market in the eyes of lenders, after Toronto. The report found that the biggest mover overall was Hamilton, which jumped four spots in the rankings to ninth place. There was also increased interest in London, ON, and Québec City, while lenders continue to express caution for assets in the Prairies.

Some key observations of the study follow:

Lenders are keen to facilitate rental apartment and industrial. Apartments saw the largest improvement in sentiment and almost no lenders reported concern with the asset class. The industrial sector is seen as a safe bet as occupancy is being bolstered by record demand stemming from the e-commerce boom. Almost one quarterof all respondents said that they were unable to meet their budget allocation for industrial products.

Lenders continue to be cautious regarding retail transactions:

Respondents continue to express interest on lending in Calgary or Edmonton. However, lender activity remains deal-dependent or relationship-specific.

While 57.9% of respondents met their 2019 budget allocations for real estate assets, the remainder were nearly evenly split between lenders not achieving plan and those that exceeded their planned budget.

Asset valuations caused some lenders difficulty in meeting their budgets in 2019, and it also ranked as the top microeconomic factor to shape lending decisions in 2020.

41.3% will increase their allocation for real estate assets in the coming year.

“For lenders looking for stable returns on investment, Canadian real estate stands out amid global uncertainty and persistently low bond yields,” said Carmin Di Fiore, Executive Vice President, Debt & Structured Finance, CBRE Canada. “Lenders remain confident about commercial real estate and are looking to deploy capital into the sector. However, lenders are also cognizant of global risks and some will be slightly more selective with their capital in 2020.”

In the US, 2019 was a record year of lending and commercial mortgage originators anticipate 2020 to be another strong year, according to the Mortgage Bankers Association’s (MBA) 2020 Commercial Real Estate Finance (CREF) Outlook Survey released in January.

The forecast revealed that commercial and multifamily mortgage bankers are expected to close a record US $683 B of loans backed by income-producing properties in 2020, a 9% increase from 2019’s anticipated record volume of US $628 B.

Nearly two-thirds of the top commercial/multifamily firms polled expect originations to increase in 2020, with 16% expecting an overall increase of 5% percent or more across the entire market. When forecasting just their own firm’s originations 42% expect to see an increase of 5% or more in lending in 2020.

“Buoyed by low interest rates, strong property markets and rising property values, commercial and multifamily mortgage banking firms expect a solid year in 2020,” said Jamie Woodwell, MBA’s Vice President Commercial Real Estate Research. “Most anticipate strong appetites from lenders and borrowers and expect overall levels of mortgage borrowing and lending to increase.”

Added Woodwell, “Overall, market leaders see an environment where there is more debt available than there are deals looking for debt, and expect 2020 should be slightly stronger than 2019.”

The proliferation of debt fund lenders, resurgence in CMBS activity and strong life insurance companies, and bank appetite has created an environment that is pushing loan structure, while at the same time reducing pricing. Full property valuations are driving the need for more structured financing vehicles as investors look to meet return hurdles. Senior/sub loan structures, which were popular during the prior boom, have gained market acceptance once again. All this competitive activity, combined with late-stage cycle concerns, are contributing to lower production levels for some capital providers, namely banks. The key takeaway is that it was a good year to be a capital user, Kathy Farrell, head of commercial real estate for Truist stated in January.

Debt funds and unsecured debentures continue to take market share. More debt funds are entering the market, fueled by the funding gap and the search for yield in fixed income. Trending now are the partnerships between traditional lenders and debt fundsusing A/B structures, reports JLL in their Canadian National Capital Markets Insight for Q2 2019.

First National, for example, reports commercial segment originations of $2.6 B, 50% higher than a year ago, which reflects strong market demand. Commercial renewals of $664 M were about 2.2 times higher from a year ago on the same fundamentals, said Jeremy Wedgbury, Senior Vice President, Commercial Mortgages at First National Financial.

The abundance of capital for debt and equity is a feature of markets for now. But capital markets are notoriously fickle and real estate veterans are well aware of how quickly a “Niagara of capital” can be dammed up, PwC states in their 2020 Emerging Trends report.

The influx of tech-based tools has not only increased the amount of data CRE professionals have access to but is speeding up the underwriting process.

The fintech ecosystem is loaded with disruptive companies, this is especially evident in the lending sector. Employing artificial intelligence, big data and even blockchain, financial institutions are using technology to solve longstanding issues.

For commercial real estate lenders, the process of uncovering, organizing, and interpreting data on a property’s mortgage or debt history has always been a time-consuming and error-prone endeavour.

The industry has witnessed the emergence of commercial real estate technology capable of quickly surfacing and aggregating property data points, including debt history and lender information, from a variety of disparate sources.

As a result, the quality of data that CRE professionals have access to has improved and along with it, the level of transparency for all market participants.

Any player looking to analyze a property is able to access information more efficiently than ever before and enables them to underwrite the property more quickly.

Technology provides the ability to formalize institutional knowledge, remove inefficiencies, improve information flow, and increase access. It allows the ability to build powerful databases that ensure a deep understanding of the buyer’s capital needs, and the lender’s tolerances and preferences. Algorithms are able to deliver perfect matches. And once that match has been made, technology provides the means to track documents and work collaboratively, in real time, to successful completion, Adi Chugh, founder ofRemissary writes in Propmodo.

Remissary is a new platform that matches commercial real estate borrowers and lenders. Borrowers and lenders can put in the parameters of what they’re looking for into the online platform, which then matches them through an algorithm. But borrowers also get a Remissary broker to help them through the process and pay a fee if a deal closes.

Similar to Remissary, RealAtom is a web-based platform that connects prospective commercial borrowers with lenders looking to build their portfolios and close more loans.

Developers in the market for new commercial construction financing, for example, put their information on the platform to create a listing. Lenders have access to that loan request, and RealAtom using their algorithm then matches the requirement to our proprietary network of over 2,500 lenders.

CrediFi provides data and analytics to commercial real estate (CRE) lenders. The company’s big data platform tracks more than 10,000 US-based lenders and the US $13 T they’ve originated to map real estate lending industry trends. Additionally, CrediFi tracks the loans of more than six million property owners to ensure that lenders are making responsible, market-determined decisions.

Equity Investors are migrating into debt to chase better yield.

In 2019, global real estate fundraising exceeded US $150 B for the first time to reach US $151 B. Despite these record amounts, the number of vehicles reaching the final close declined to 295 in 2019, which means funds are getting larger. And the number of funds in market is now at an all-time high.

Deal-making did not match the records set in 2018, activity was still substantial and fund managers were able to successfully deploy capital, with dry powder decreasing to US $319 B as of December 2019, according to Preqin research.

“Real estate has benefited from a huge influx of capital in the past five years. But the steep decline in the number of funds closed shows how unevenly that capital is distributed—concentration among the largest fund managers is greater than ever,” stated Justin Hall, Head of Real Estate at Preqin.

Returns on core equity investments have shrunk as property values have increased. Value-add debt funds now offer more payoff which has led some equity investors to migrate into debt, reports Michael Lavipour, a managing director at Square Mile Capital Management LLC.

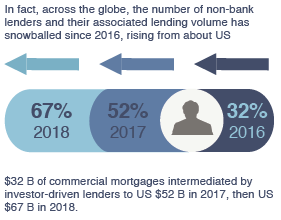

Investor-driven lenders have become a major source of commercial mortgage finance in recent years, states Jamie Woodwell of the Mortgage Bankers Association.

In the first half of 2019, it was 10% ahead of the pace seen a year before, according to the MBA data. The top investor-driven lenders have been Blackstone, Deutsche Bank, Capital One and Wells Fargo.

The growing number of lenders competing for the same opportunities has hampered some funds’ ability to put their capital to work, Preqin’s head of real estate, Tom Carr, said in an interview. Global real estate debt funds’ dry powder has piled up to US $61 B as of March 2019, from a low of US $12 B as of December 2012.

Canadian pension plans have been steadily growing their real estate allocation for at least a decade now. Real estate is one of the fastest-growing asset classes in the Canadian pension fund asset mix, with a 12% allocation as of 2018, double the level in 2006, Manulife reports.

As of the end of 2018, the top 10 Canadian pension funds had an average allocation to real estate in excess of 14% and that is likely to grow.

In November, RBC Global Asset Management Inc. (RBC GAMInc.) announced the first closing of the RBC Canadian Core Real Estate Fund which attracted more than $1.25 B in equity commitments from institutional and individual investors, exceeding subscription targets. The real estate fund is the result of a $7.5 billion collaboration with British Columbia Investment Management Corporation and QuadReal Property Group.

The bar will be raised and there will be more focus on the quality of ESG strategies.

Global Real Estate Sustainability Benchmark (GRESB) was established in 2009 by a group of large pension funds who wanted to have access to comparable and reliable data on the environmental, social and governance (ESG) performance of their investments.

Ten years later their ESG data covers US $4.5 T in real estate and infrastructure assets and is used by more than 100 institutional and financial investors to make decisions that are leading to a more sustainable real asset industry.

Canada is near the front of an increasingly competitive pack. Together, 26 real estate portfolios achieved an average score of 76.6, surpassing both the America’s average of 72.1 and the global average of 72, but off the pace of Australia/New Zealand’s 80.9 average score. Europe, home to the largest number of participating portfolios, trailed the field with an average score of 70.7, exceeding last year’s global average of 68.4.

GRESB investor members include Alberta Investment Management Corporation (AIMCo), HOOPP, Ivanhoé Cambridge, Ontario Teachers’ Pension Plan, Oxford Properties Group and Presima, while many more companies report and are benchmarked through the real estate assessment.

“The investor community is asking us for our GRESB scores now,” reported Regan Smith, director of sustainability with Manulife Investment Management. “Whereas, I don’t think they were asking at all about ESG ten years ago.”

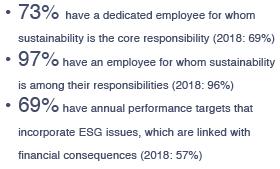

Over 90% of GRESB participants now have multiple ESG objectives that are fully integrated into their business strategy. The majority have established management structures to support execution on these ESG objectives:

90% of participants align their projects with green building rating standards. In addition, 45% of participants with development projects require a specific level of certification for more than 75% of their projects under development. Overall, 11% more participants have programs in place to address health and wellbeing of employees as compared to tenants/customers.

A 2019 survey from the Canadian Investor Relations Institute found that 87% of companies view ESG factors as important to their company’s long-term success, and 81% of respondents said their board or a committee oversees ESG issues. This should transmit into improved corporate disclosures.

CSA Group, the Canadian standards body, is convening a committee of market participants to develop a transition-focused framework that is more suitable for Canada and other resource driven economies.

As of January 1, publicly traded companies governed by the Canada Business Corporations Act are required to disclose their policies and practices related to diversity on their boards of directors and within senior management, including the proportions of women, Indigenous peoples, people with disabilities and members of visible minorities.

PwC identifies three emerging themes in its 2019 Private Equity Responsible Investment Survey:

Human Rights

Pressure is growing to understand and use the UN Guiding Principles on Business & Human Rights, to integrate human rights into their due diligence processes and to apply a human rights lens to the “Social” of ESG. New initiatives and laws around mandatory human rights due diligence for companies have taken shape. These include the Australia Modern Slavery Act and the Swiss Responsible Business Initiative adding to the UK Modern Slavery Act and France’s Duty of Vigilance Law.

Climate Change

Climate goals and risks are being redefined and business leaders are stepping in to set direction where policymakers are not, as evidenced by initiatives like the RE100 coalition, where over 150 large companies have committed to source 100% renewable energy, reports Libby Bernick, Managing Director¬ and Global Head of Trucost Corporate Business.

Sustainable Development Goals

The SDGs are a collection of 17 goals adopted by all United Nations member states in 2015 and provide a blueprint for “good growth” nationally and internationally.

Revenue and savings opportunities coming out of innovating around these goals are estimated at over US $12 T per year through 2030. The backlash against single-use plastic entering the ocean has catalyzed leading chemical companies and plastic manufacturers to invest in innovation and recycling infrastructure. For example, SC Johnson has committed to making 100% of its plastic packaging recyclable, reusable, or compostable by 2025, reports Bernick.

Corporate sustainability teams will need to be on the defence to identify and manage their ESG risks while having a strong eye on the offence to innovate on products and services that will capture opportunities being created in new markets.

Escalating land prices and labour costs are causing banks to become more wary of new construction financing, which has resulted in more developers becoming lenders themselves.

New construction as land prices and labour costs have all grown significantly, pushing budgets up at rates exceeding rent growth in many markets. In addition, with cap rates at record lows, property values continue to be very strong and could perhaps be priced at full value. Right now, there is a gap in the capital stack between banks’ comfort level and borrowers’ total financing needs. Mezz lenders and A/B structures are stepping in to fill that void, Kathy Farrell, head of commercial real estate for Truist said in January.

Debt funds now account for 22% of US construction lending Real Capital Analytics reports.

Large development companies have begun lending money to other developers, providing in-demand construction financing. These same companies borrow money from the big banks that their borrowers can’t do business with. They leverage their ability to source capital relatively cheaply to fill a gap in construction lending. Developer-to-developer lending is expected to keep growing because the economics benefit both sides of the transaction.

There are a number of NYC-based developers who recently haveset up lending divisions.

Silverstein Properties Inc. launched a joint venture last September to extend financing for office, industrial, residential and retail properties in growing urban markets across North America. Silverstein Capital Partners provides senior loans, bridge loans, subordinate loans and rescue capital for ground-up construction, value-add repositioning, lease-up and land projects, as well as inventory loans for condo projects. Loans start at US $25 M; there’s no cap on loan size.

Naftali Group recently set up its debt fund subsidiary, Naftali Credit Partners. The fund specializes in high-yield mezzanine construction loans.

In October, Naftali Credit Partners closed on a US $50 M loan for construction of 145 Central Park North, a 37-unit luxury condo project in Manhattan. Naftali Credit Partners sourced the senior loan and brought aboard Israel Discount Bank as its financing partner. Naftali Credit Partners closed on a $65 M loan for a10-story, 74-unit luxury condo project in Queens earlier in 2019. Naftali brought on CIT Bank as the senior mortgage lender.

The Moinian Group is another developer to set up a lending division. Its financing unit, Moinian Capital Partners, in April provided a US $119 M senior loan and US $23.5 M mezzanine loan for a 434-unit apartment high-rise in Miami. Moinian Capital Partners, founded in 2017, targets apartment properties in gateway cities, along with hospitality, office and retail assets.

Slate Property Group has launched a commercial lending arm to be called SPG Capital Partners. SPG intends to explore opportunities to provide construction, bridge, transitional, mezzanine and condo inventory loans worth up to 80% of a project’s total value, according to The Real Deal.

As well, banks have tightened their purse strings when it comes to spec development financing.

“Generally speaking, it is very difficult to get great financing for spec office from traditional senior lenders,” says Tommy Lee, a principal and head of capital markets at Trammell Crow Co. Trammell Crow is one of the most active spec developers in the US.

Those traditional senior lenders, primarily banks, have higher expectations in terms of recourse and pre-leasing requirements, while at the same time have lowered leverage on a loan-to-cost basis. Trammell Crow is now seeing spec leasing requirements from its bank lenders on office projects that range anywhere from 30% to 50%, with loan-to-cost amounts between 50% and 60%.

Even among non-bank lenders, financing for spec office projects is very market and location specific. “Really only top downtown locations and very select work-live-play suburban nodes are going to get financing today,” says Dan Levitt, senior vice president of capital markets at Ryan Cos. US Inc.

“Pre-leasing changes everything,” says Seth K. Grossman, a senior managing director at Meridian Capital Group. Metrics are still important. However, projects with pre-leasing above 30-50 percent open the doors to many more capital options, with lenders willing to do deals at different leverage levels.

According to Jeremy Wedgbury, Senior Vice President, Commercial Mortgages at First National Financial, lending to builders with experience is key especially those who have the ability to manage risk and respond quickly to changing circumstances.

Although higher construction costs are on lenders’ radar the strong supply and demand dynamics are pushing spreads down in the construction loan market, JLL reports. Overall, cheap and abundant capital is available for lending in Canada, with few clouds on the horizon.

The market share of non-bank lenders has been growing steadily as banks become more selective.

Alternative lenders are playing a growing role in Canada’s real estate market as the industry searches for new sources of financing, risk-averse banks become pickier, and investors look for yield.

Every year there are new entrants to the alternative lending space who are free to offer high loan-to-value ratios and loan-term flexibility. Among the nonbank sources entering the market are debt funds, mortgage REITs, online lending platforms.

In fact, there were 200 to 300 active alternative lenders in Canada last year holding $13 B to $14 B of outstanding Canadian mortgages. This number is steadily increasing from $11 B to $12 B the year prior and $8 B to $10 B in 2016.

An increasing number of homeowners turned to alternative lenders last year, while new mortgage growth reached its slowest pace in more than a quarter of a century amid government interventions aimed at cooling the housing market, according to a 2019 report by CMHC.

As a result, alternative lenders like Home Capital and Equitable Group Inc. have seen their stocks surge this year as the pace of mortgage growth picked up and home sales recovered in major cities including Toronto and Vancouver.

Significant share price appreciation of the alternative lenders is reflective of improving housing conditions specifically in the GTA as well as a benign credit environment and robust mortgage growth outlook, CIBC analyst Marco Giurleo said in a November 2019 note to clients.

We are also seeing more ‘truly’ private lenders stepping in, typically backed by groups of high-net-worth individuals. These lenders are providing a strong supply of high-leverage high-yield loan options for smaller and riskier transactions. Although relatively marginal, increased participation of investors with little or no capital to cushion losses could accelerate the impact of any deterioration in credit conditions in certain submarkets, JLL reported in their Q2 2019 Canadian Capital Markets Insight.

CBRE notes that alternative lenders have raised record amounts of capital for secondary financing and transitional property lending. CBRE says, this infusion of capital could exert upward pressure on loan proceeds and underwriting standards.

CMHC expects home prices are expected to increase in 2020 as a result of growth in household formation and disposable income.

There were just 4.2 months of inventory on a national basis at the end of November 2019 – the lowest level recorded since the summer of 2007 and well below its long-term average of 5.3 months. While still just within a balanced market territory, its current reading suggests that sales negotiations are becoming increasingly tilted in favour of sellers, according to the Canadian Real Estate Association.

“Home prices look set to continue rising in housing markets where sales are recovering amid an ongoing shortage of supply,” said Gregory Klump, CREA’s Chief Economist. “By the same token, home prices will likely continue trending lower in places where there’s a significant overhang of supply, perpetuated in part by the B-20 mortgage stress-test that continues to sideline homebuyers there.”

CMHC forecasts that existing home sales will stay near their 2018 level in 2019, below the historical peak observed in 2016 which was 533,000 sales.

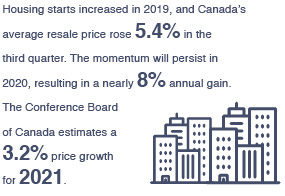

The average MLS® price is expected to decline for a second consecutive year in 2019 from the recent high registered in 2017 which was $511,830. However, CMHC expects that positive price growth will resume in 2020 and 2021, driving the average price above its 2017 level. This is expected to reflect household disposable income growth and rates of household formation that will remain supportive of price growth.

In its outlook for 2020, Re/Max said buyers are becoming more enthusiastic, and “increased consumer confidence could be a key factor affecting the housing market in 2020.” The report predicted a 3.7% increase in house prices nationwide, with Toronto prices rising 6% next year, roughly doubling this year’s pace. “As more Canadians have adjusted to the mortgage stress test and older millennials move into their peak earning years, it is anticipated that they will drive the market in 2020,” says Re/Max. “A recent Leger survey conducted by Re/Max found that 51% of Canadians are considering buying a property in the next five years, especially those under the age of 45.”

Central 1 Credit Union stated that “BC’s housing market is recovering much quicker than anticipated due to improved affordability and increased housing demand, driven by lower mortgage rates, first-time buyer incentives and population growth boosted by international migration.”

After falling nearly 7% in 2019, Central 1 expects house prices to rise in the Vancouver area by 3.6% this year, and 6.3% in 2021.

Royal LePage forecasts that the aggregate price of a home in the Greater Montreal Area will increase 5.5% year-over-year by year-end 2020 to $457,900, which is similar to 2019’s rate of appreciation. At this pace, the GMA real estate market will enter its fourth consecutive year of price appreciation above the 4% mark.

In 2020, the aggregate price of a home in Calgary is forecast to increase by 1.5% year-over-year to $477,000. “There are signs that the Calgary real estate market has touched its price floor and we are beginning a gradual return to balance,” said Corinne Lyall, broker and owner at Royal LePage Benchmark. “There’s positive news with the Trans Mountain Expansion, increased net migration and new jobs. Calgary’s housing market will see some buoyancy but it’s not going to be immediate.”

Across much of Canada, strong rental demand has pushed vacancy rates to historic lows. In Vancouver, Toronto and Montreal rates are hovering around the 1.0% mark.

As of November 2019, the national average rental rates declined for the second consecutive month, but are still up 9.4% annually.S econdary markets such as London, Hamilton, Kanata, Burlington, and Kitchener are all experiencing double-digit rent growth when considering all property types, reports Rentals.ca and Bullpen Research & Consulting Inc.

In their 2020 forecast, they call for national rent growth of 3% next year.

The impact of the changes to the mortgage stress test has started to fade as developers and investors look to increase rental supply to offset the increase in rental demand brought on by the decrease in mortgage credit and the spike in population over the past two years, according to Bullpen Consulting.

At the end of the third quarter, CMHC reported almost 72,000 rental units under construction in Canada, the highest rate in over 30 years. As this new supply hits the market, expect moderate rent growth in 2020 compared to 2019.

Real Insights is powered by Altus Group’s Investment Transactions research. For more information, please visit altusgroup.com.

20 Eglinton Ave West, Suite 1200

Toronto, ON, M4R 1K8

Canada Post – PO Box 2055

English: 416-512-3807

Français: 416-945-0310

Subscribe to the Real

Estate Forums Newsletter. Gain excess to expert opinions, breaking news, market

data and reports.

Become a Real Estate

Forums Club Member to access over 20 industry benefits.